What Do I Need to Open a Business Bank Account? Full Checklist

A business bank account separates your business and personal finances, which simplifies tax preparation and limits your personal liability if the business runs into trouble. It also lets you build business credit independently of your personal credit.

What you actually need varies by entity type, but the core checklist is short. Below is the full document list, plus how to pick the right account type for your business.

Benefits of Having a Business Bank Account

Business accounts simplify bookkeeping, tax preparation, and payroll because all business cash flow runs through one channel. Vendors and investors generally take a business more seriously when invoices and payments come from a business name rather than a personal account.

If you own certain business enterprises, you may gain limited liability protection, which means collectors can’t target your personal assets to pay off the business’s debt.

Business accounts often include buyer-protection features for card and mobile-wallet purchases, which reduces dispute risk on both sides of a transaction.

Types of Business Bank Accounts

Requirements vary by entity type — a sole prop with no DBA needs less paperwork than an LLC or corporation.

Before you start, you need to decide which type of business account(s) you need. Sole proprietorships may only need checking accounts, but small to medium-sized businesses may need more than one type of account.

Do you need to handle payroll, accept customer payments, earn interest, or improve your credit? Depending on your needs, you may want to open a checking, savings, or merchant account — or more than one of these.

Checking Accounts

A business checking account is typically the first account you’ll open when starting a business. You can use it to make deposits and withdrawals, pay bills, and manage payroll. You also get access to business debit cards and checks.

Check out our U.S. Bank Business Checking Review and see how it compares to other options.

Savings Accounts

If you’re starting to gain traction and have extra money sitting around, saving accounts for businesses are ideal for storing money and earning some interest. You can use these accounts for emergency funds, large purchases, future investments, or tax purposes.

A high-yield savings account can be useful for businesses as well as individuals because it will earn you significantly more interest than a typical savings or checking account.

Merchant Accounts

If you accept card or mobile payments — in person or online — you'll need a merchant services account. Retailers, restaurants, food trucks, and online stores all need one; service businesses with card-paying clients usually do too.

Look for merchant accounts that integrate with point-of-sale (POS) systems, have robust security protocols, and incorporate tools like invoicing and payment portals.

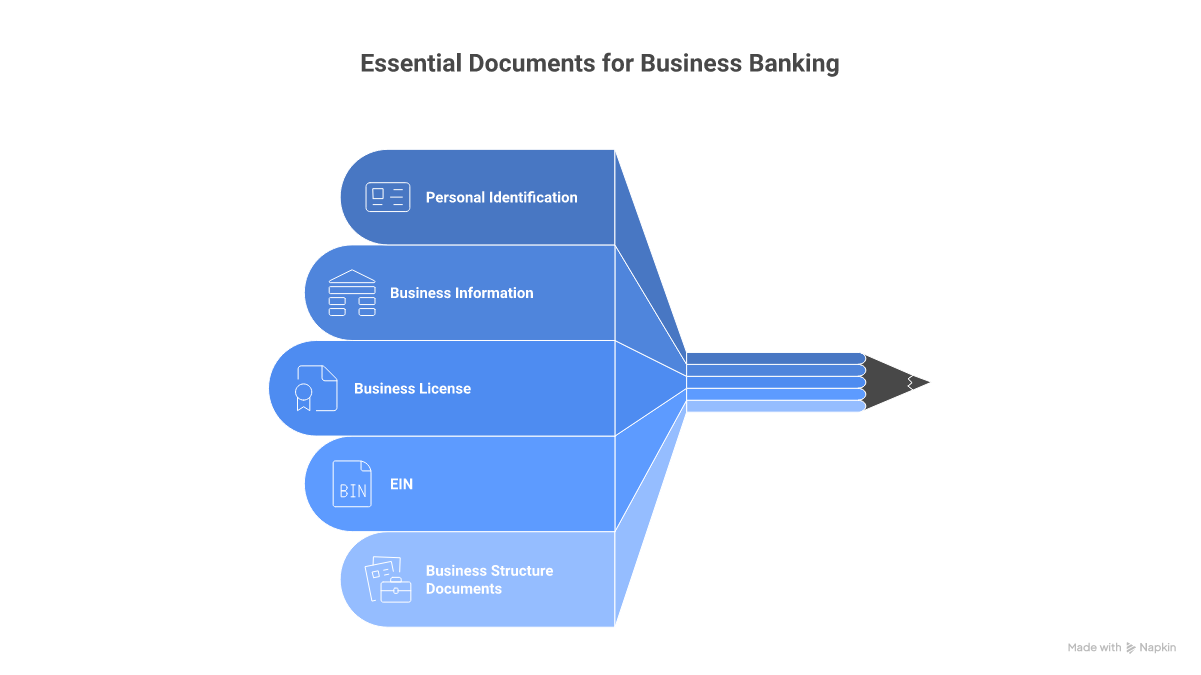

Required Documentation

Once you've picked the account type, here's what to bring.

In general, you’ll need to provide your preferred financial institution with the following documentation to open a bank account for your business:

- Personal identification: driver’s license, SSN number

- Business information: name, address, and structure

- Business license: document allowing you to operate within a jurisdiction

- Employer identification number (EIN): acts as a federal tax identification number

Requirements Based on Business Structure

In addition to showing your business license, you may need to provide documents proving business formation for your particular business structure:

- Corporation: Articles of Incorporation

- Limited liability company (LLC): Articles of Organization

- Businesses with a trade name: Doing Business As (DBA) certificate

- Partnerships: Partnership Agreement

How to Prepare to Open a Business Bank Account

- 1

Form your entity and get an EIN

Register your business with your state, then apply for a free Employer Identification Number from the IRS. An EIN works as your business's federal tax ID and keeps company records separate from your personal ones. The Small Business Administration guidance covers registration for each entity type.

- 2

Gather your formation documents

Pull the paperwork that proves your business exists: Articles of Incorporation for a corporation, Articles of Organization for an LLC, a partnership agreement, or a DBA certificate if you operate under a trade name. A sole proprietor with no trade name usually skips this step.

- 3

Gather personal and business ID

Bring a government photo ID and your Social Security number, plus the business name, address, and any required business license. Banks verify both you and the entity, so have the legal business name exactly as it appears on your formation papers.

- 4

Prepare ownership and beneficial-owner information

If anyone owns 25% or more of the business, banks collect their details to meet beneficial ownership reporting requirements. Have each owner's name, address, date of birth, and ID number ready before you apply.

- 5

Compare accounts and apply

Decide whether you need checking, savings, or merchant services, then weigh fees, minimum deposits, and transaction caps before you commit. Many banks let you finish the application online; others want you in a branch. Compare business checking accounts and apply with your documents in hand.

Choosing the Right Financial Institution

Traditional banks aren't your only option. Credit unions often charge lower fees and offer smaller minimum payments for business credit cards and loans. Local branches tend to handle relationship questions in person, which can matter if your business needs flexibility on overdrafts or wire fees.

Bank vs. credit union, the document checklist is the same. The differences are in fees, processing speed, and online availability.

Many smaller credit unions have fewer requirements to open an account compared to national banks, and they may offer sign-up bonuses. But setting up your account can be slower, and you may not be able to do it online. The process may also be more complicated if you need to close a business account.

If your business operates in multiple states or you need to accept international payments, you’re likely better off with a traditional bank.

Tips for a Smooth Account Opening Process

Opening the account itself is straightforward, especially online. Most major banks and online-only banks let you complete the application without going to a branch.

Though some traditional banks require in-person application and document review due to regulatory standards, many online banks offer fully online applications. If you have to go in person, call ahead to clarify which documents you’ll need and make an appointment.

Most business accounts have a minimum opening deposit, monthly maintenance fees, and transaction caps. Read the fee schedule before applying — wire fees, cash deposit fees, and excess-transaction fees vary widely between banks.

Common Challenges and How To Avoid Them

Common pitfalls when opening a business bank account include incomplete or inaccurate documentation, lack of credit history, or excessive minimum deposits or online fees.

Most issues come down to documentation. Confirm the bank's exact requirements (some require an in-person visit; some require notarized formation documents) before starting the application. Check for state-specific rules — a few states have specific requirements for the business name attached to bank accounts.

If you need to build credit, look for banks offering business credit cards for bad credit. A business credit card is one of the simplest ways to build a track record. Use it for routine expenses, pay it off monthly, and after 6–12 months you'll have a credit profile lenders can underwrite against.

FAQ

Learn More About Business Banking With MoneyAtlas

Beyond the bank account, there are decisions on credit cards, payroll, accounting software, and tax handling. MoneyAtlas covers each of these with comparisons and how-to guides.

MoneyAtlas reviews financial products and writes how-to guides for small business owners, individuals, and nonprofits. Recent business-focused content includes a Found business banking review and side-by-side comparisons of business savings accounts.

Compare the best business checking accounts for your business.

Emily Pitkin

Education

- Bachelor of Science Degree in Economics, Portland State University

- Master of Arts in Professional Writing, New England College

Expertise

- Long-term Investing and Retirement Planning

- Budgeting and Saving

- Debt Management Strategies

- Small Business Development

Related Articles

SoFi vs Discover: Banking, HYSA, and Personal Loan Comparison

Side-by-side comparison of SoFi and Discover for checking, savings, and personal loans: APYs, fees, rates, and who each bank is best for.

High-Yield Savings Accounts with No Minimum Balance

Looking for a high-yield savings account with no minimum balance? Explore top options offering great interest with no deposit requirements.

Checking vs Savings Account: Which One Do You Really Need?

Checking accounts are ideal for daily spending, while savings accounts earn more interest. Learn the pros, cons, and when to use each account type.