SoFi vs Discover: Banking, HYSA, and Personal Loan Comparison

More and more people are turning to digital financial services rather than traditional in-person banking. But with so many options popping up, finding the right financial institution for your needs and preferences can get overwhelming.

SoFi and Discover are two popular digital financial institutions. Whether you’re looking for a checking account, personal loan, or other financial services, this SoFi vs. Discover comparison will help you make the right choice.

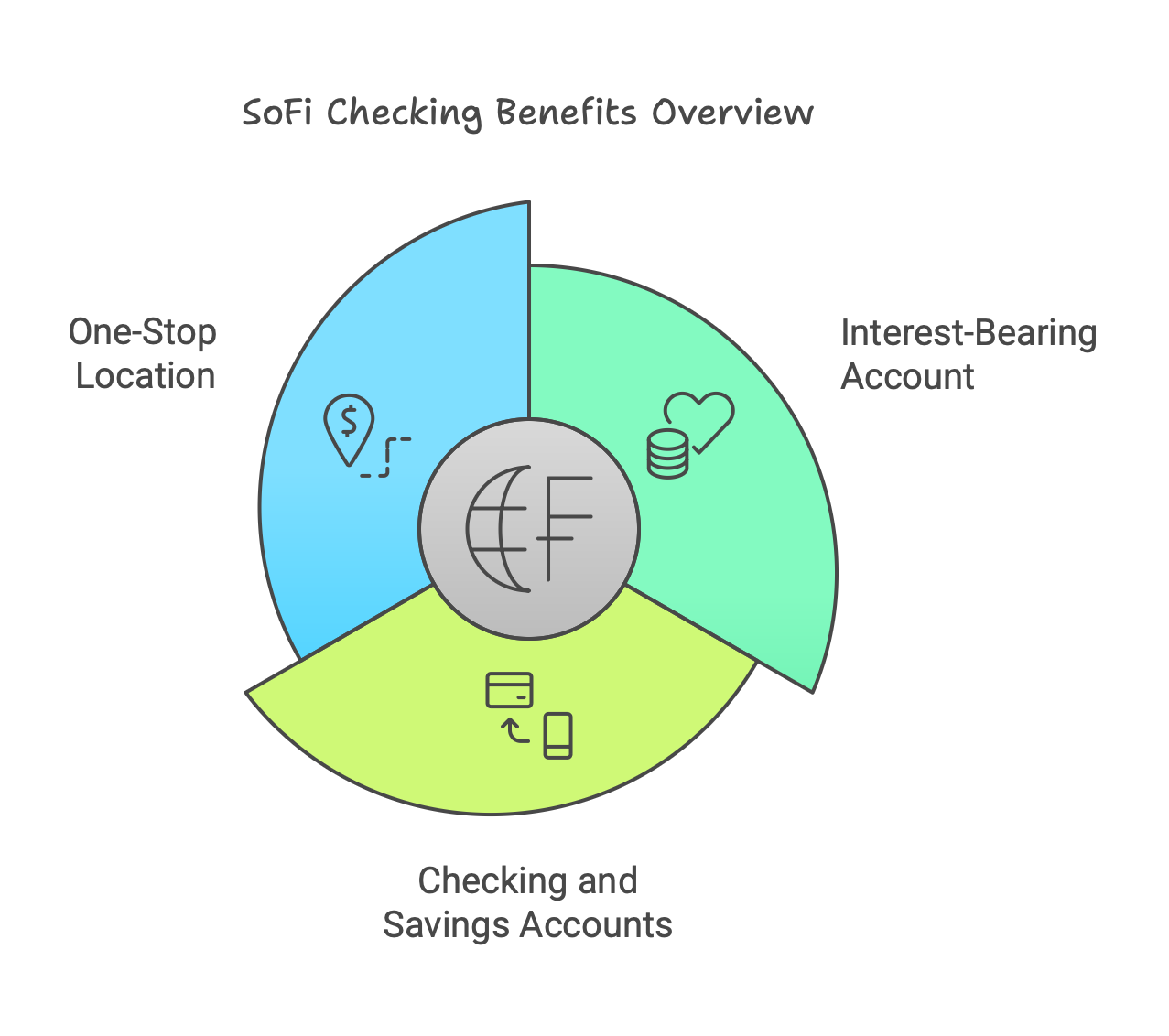

Why Choose SoFi Checking

SoFi offers an online checking account that’s suitable for many modern financial customers. Here are a few of the factors that set it apart.

Interest-Bearing Account

SoFi’s online checking account is an interest-bearing account, meaning you can earn interest on the money you deposit. Checking accounts typically earn little to no interest, so the interest you earn on your SoFi checking account balance is a nice bonus over many other options.

Checking and Savings Accounts

When you open a SoFi checking account, SoFi will also automatically open a high-yield savings account for you as part of one easy sign-up process. That way, you can access higher interest rates on your savings account balance to help you save for the future.

Discover also offers a high-yield savings account with a similar interest rate, so it’s hard to say which account comes out ahead in the SoFi vs Discover high yield savings account comparison.

One-Stop Location for Managing Your Money

The SoFi app allows you to send money, deposit checks, and pay your bills — all from one place. It’s a very convenient way to stay on top of your finances without having to deal with tons of apps, websites, or accounts. SoFi checking and savings accounts also don’t have any minimum balance, monthly service, or ATM fees, which can save you money compared to many other banking options.

Something that sets SoFi apart in the SoFi vs Discover savings account comparison is that your SoFi accounts are automatically linked. And, if you enable Roundups, SoFi will automatically round up all your debit card purchases to the next whole dollar and deposit the change in your savings account. That way, you can grow your savings with your everyday purchases.

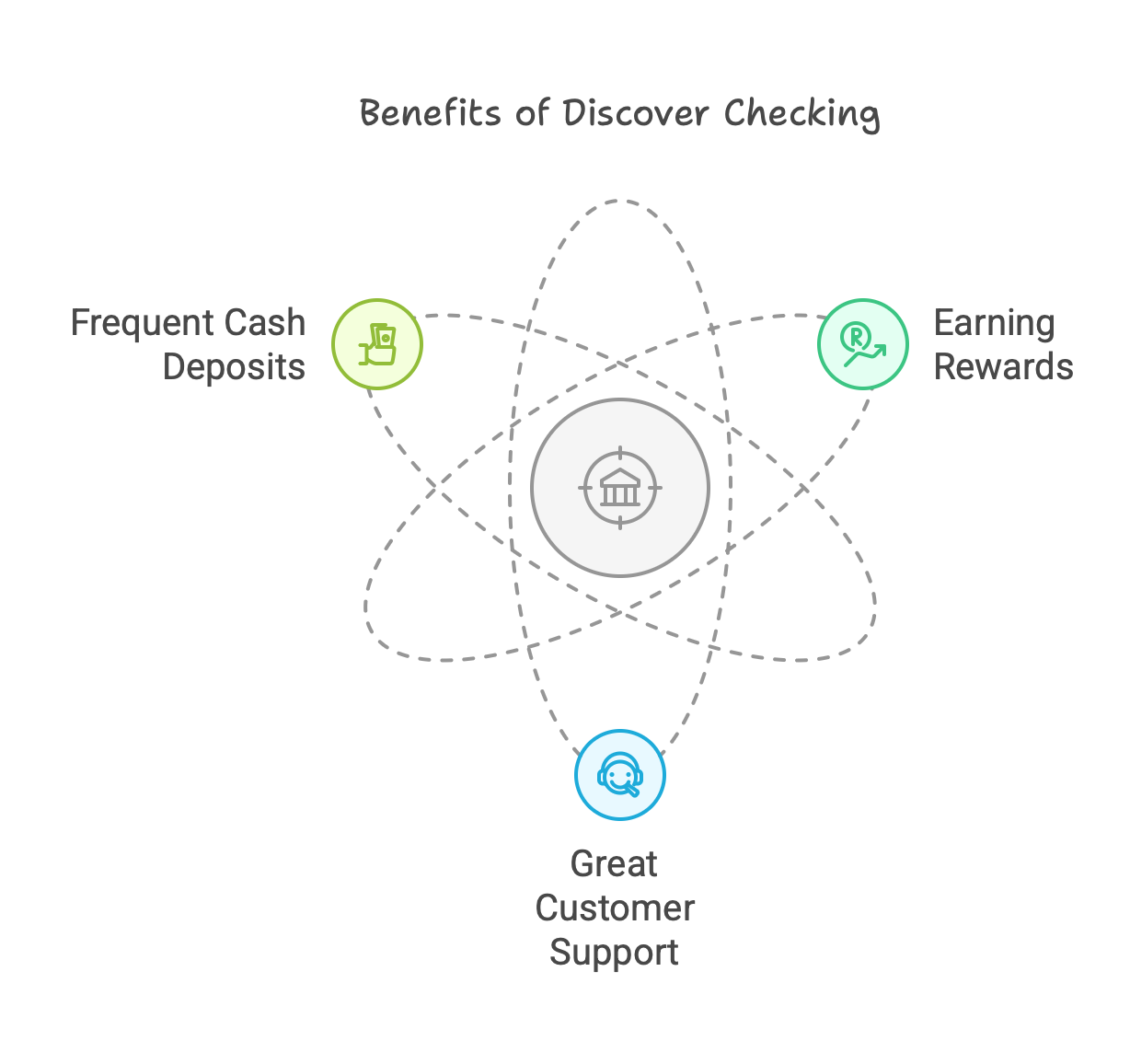

Why Choose Discover Checking

Discover’s checking account is called the Discover Cashback Debit account, and it rivals the best bank options for checking accounts.

Earning Rewards

As the name suggests, the account lets you earn cashback on the debit card purchases you make each month up to a set limit. Earning these rewards can be a nice bonus, putting a little extra money in your account for purchases you would already make.

Also, like SoFi, Discover does not charge monthly service or minimum balance fees on checking accounts. You can also use over 60,000 ATMs in the U.S. with no ATM fees. You don’t have to worry about fees chipping away at your account or the rewards you earn.

Great Customer Support

Discover is known for its strong customer support. If you have any issues with your checking account or online services, you can contact Discover’s 24/7 live, 100% U.S.-based customer support team for help. Knowing that you have access to high-quality support from live representatives in the United States can be a significant comfort.

This great customer support is part of the reason why the Discover checking account tied for first place in customer satisfaction in a 2022 J.D. Power study. Discover customers are largely happy with their checking accounts and the support they receive.

Frequent Cash Deposits

One of the drawbacks of digital banking is that it can be inconvenient or even impossible to deposit cash into your account. That’s not the case with the Discover checking account.

As a Discover checking account holder, you can add cash to your account at any Walmart in the U.S. Since there are over 4,500 Walmart stores throughout the country, you probably have one nearby where you could deposit cash into your Discover checking account.

And the best part is that these deposits are completely free. You don’t have to pay any fees — just use your contactless debit card.

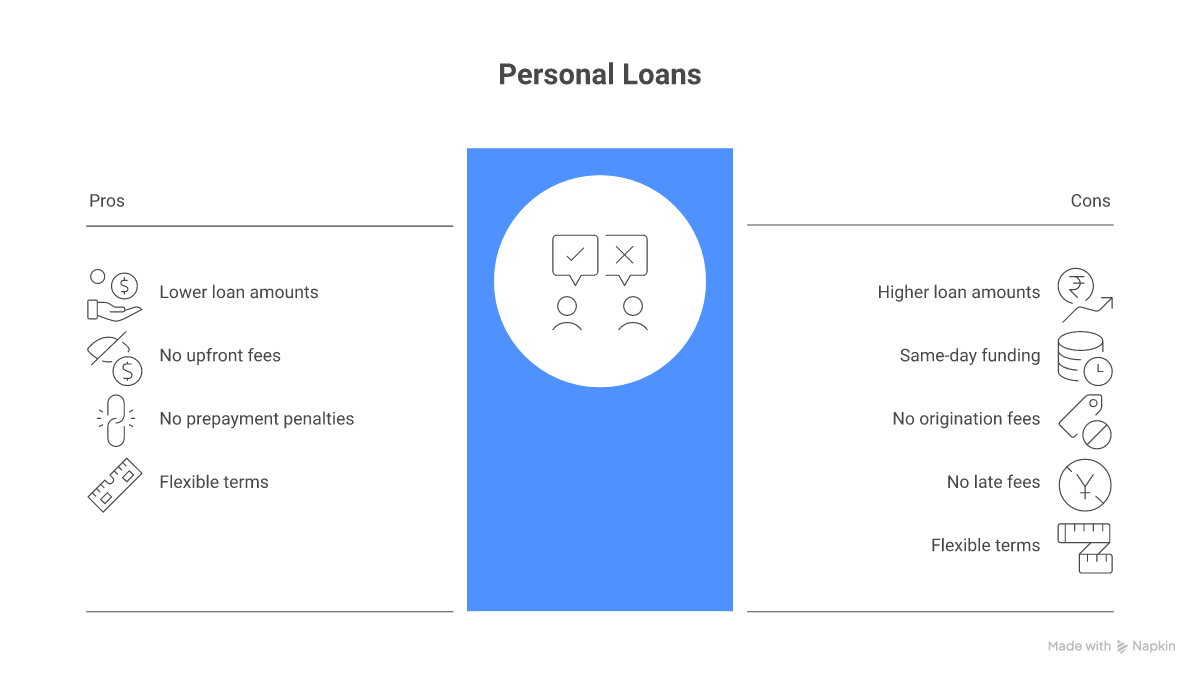

Discover Personal Loans vs. SoFi Personal Loans

If you need to borrow money, both Discover and SoFi offer personal loans. Consider these key factors when comparing SoFi vs Discover personal loans.

Discover

- Lower loan amounts ($2,500 to $40,000)

- No up-front fees or prepayment penalties

- Flexible loan terms of 36 to 84 months

SoFi

- Higher loan amounts ($5,000 to $100,000)

- Get your funds as soon as the same day

- No origination fees, late fees, or prepayment penalties

- Flexible loan terms of 24 to 84 months

You may find it helpful to check your personal loan interest rate offer from both Discover and SoFi to help you select the right loan. That way, you can see your estimated monthly payment with both institutions and make a more informed choice.

SoFi vs Discover: High-Yield Savings

SoFi's checking account automatically opens a paired high-yield savings account, with a tiered structure that requires qualifying direct deposit to unlock the top APY. Discover Online Savings is a standalone HYSA with no minimum balance and no monthly fees. Both products are FDIC-insured up to $250,000 per depositor per institution and account ownership category.

The practical difference shows up in how the two banks bundle the savings product. SoFi packages checking and savings as one linked account family, so transfers between the two clear instantly and the Roundups feature drops debit-card change straight into savings. Discover keeps Cashback Debit checking and Online Savings as separate accounts you link manually.

If you already qualify for SoFi's direct-deposit tier, the SoFi APY is competitive with Discover's. If you don't, Discover's flat rate pays the same on every dollar with no qualifying activity, which is the simpler path for savers who can't reroute payroll.

Compare

Side-by-side snapshot of SoFi, Discover, and Synchrony Bank, three online-only banks most consumers consider when shopping a high-yield savings rate alongside a checking account.

SoFi vs Discover: Pros and Cons

SoFi

Pros

All-in-one money hub: checking, savings, investing, and lending live behind one login, and transfers between accounts settle instantly.

Roundups boost savings: every debit-card purchase rounds up to the next dollar and the change drops into your linked savings account.

Fast personal-loan funding: approved SoFi personal loans can fund as soon as the same business day, with no origination fees, late fees, or prepayment penalties.

Cons

Top APY is conditional: the headline savings rate requires a qualifying direct deposit; users without one earn a lower base rate.

Cash deposits cost money: loading cash into a SoFi account runs through a retail partner network that charges a fee per deposit.

No branch network: every interaction is online or in-app, so there is no in-person service if a problem needs a face-to-face fix.

Discover

Pros

Cashback on debit purchases: Discover Cashback Debit earns 1% cash back on up to $3,000 of qualifying debit purchases each month.

U.S.-based 24/7 support: customer service representatives are based in the United States and pick up around the clock, every day of the year.

Free cash deposits at Walmart: you can load cash to your Discover checking account at any participating Walmart MoneyServices counter at no charge.

Cons

No investing or auto lending: Discover stops at deposit accounts, credit cards, and personal loans; brokerage and auto loans are not in the app.

Lower personal-loan ceiling: Discover caps personal loans at $40,000, well below SoFi's $100,000 ceiling for larger borrowing needs.

Flat HYSA rate: Discover Online Savings pays a single APY on every balance tier, so high balances do not unlock a higher rate.

Choose Between Discover and SoFi with Money Atlas

SoFi and Discover are both strong options for banking services like checking accounts and personal loans. Consider which features are most important to you and choose the financial institution or product that ticks the most boxes off your list.

Finding the right financial institutions and services for your needs doesn’t have to be a hassle. Money Atlas, a platform for expert comparisons of banking, loans, credit cards, and investments, is here to help you figure out which option is right for you.

Take control of your money and explore more financial product comparisons on Money Atlas today.

FAQ

Education

- Bachelor’s Degree in Economics, Ramapo College of New Jersey

Expertise

- Debt and Credit Management

- Budgeting and Money-Saving Strategies

- Financial Digital Security and Fraud Protection

Related Articles

High-Yield Savings Accounts with No Minimum Balance

Looking for a high-yield savings account with no minimum balance? Explore top options offering great interest with no deposit requirements.

What Do I Need to Open a Business Bank Account? Full Checklist

Wondering what do you need to open a business bank account? Here's a complete checklist, including IDs, licenses, and business formation documents.

Checking vs Savings Account: Which One Do You Really Need?

Checking accounts are ideal for daily spending, while savings accounts earn more interest. Learn the pros, cons, and when to use each account type.