Amex Blue Cash Everyday Credit Limit: What to Expect

The American Express Blue Cash Everyday card is a cash-back rewards credit card that offers a range of benefits to cardholders. While any cardholder can earn rewards, individuals may have different credit limits based on their creditworthiness and income. Like most credit cards, the Amex Blue Cash Everyday credit limit is revolving, meaning that once you've made payments on the balance, you'll have access to that credit again.

Here's what to know about the Amex Blue Cash Everyday card.

Pros and Cons of the Amex Blue Cash Everyday Card

Like any credit card, there are pros and cons to the Amex Blue Cash Everyday card.

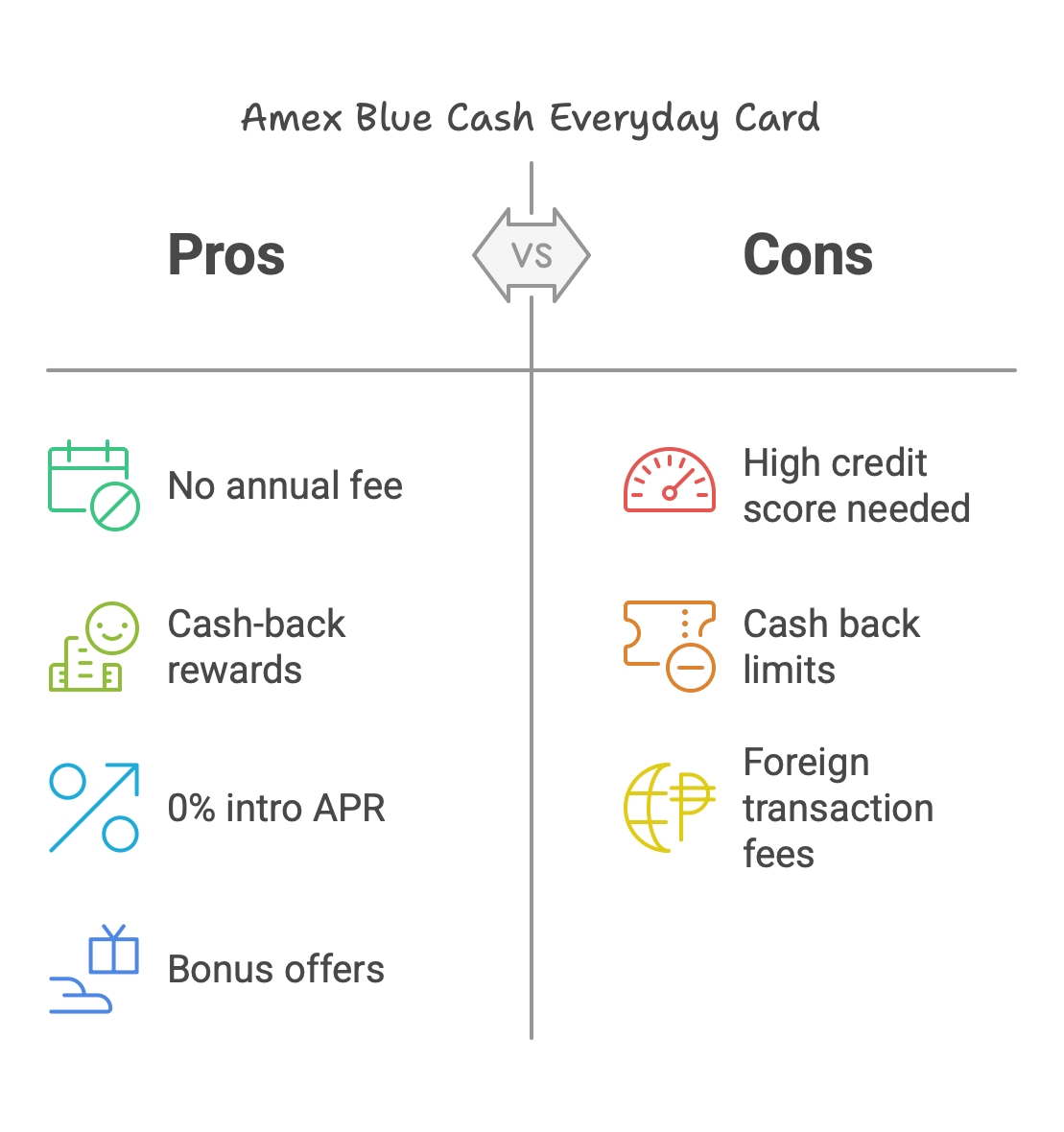

Advantages

- No annual fee

- Cash-back rewards

- 0% intro APR for the first 15 months

- Bonus offers

The key advantages of the Amex Blue Cash Everyday card are the high cash-back value and the lack of an annual fee. For a card with no fee, the Blue Cash Everyday card offers surprisingly strong rewards, with 3% cash-back atU.S. supermarkets, U.S. gas stations, and U.S. online retail purchases up to the first $6,000 of annual spending in each category. (After that, the cash-back percentage drops to 1%.) It also offers 1% cash-back on all other purchases.

The Amex Blue Cash Everyday card has several introductory benefits, including a 0% intro APR on purchases and balance transfers for 15 months, and a $200 statement credit after spending $2,000 on your card within the first six months. Some other bonuses you'll get with the card include an $84 Disney Bundle Credit and a $180 Home Chef credit.

Since the card has no preset spending limit, it's a good choice for applicants with a high credit score and income who want to earn rewards without paying an annual fee.

Disadvantages

- Requires a high credit score to qualify

- Cash back limits

- Foreign transaction fees

Despite the advantages, there are a few drawbacks to the Amex Blue Cash Everyday card. One we already mentioned: cash-back rewards drop after a certain amount of annual spending. While $6,000 is a sizable number for each category, it's not unreasonable to think you may spend more than $6,000 on groceries in a year, thereby earning reduced rewards by the end of the year.

Additionally, American Express charges a 2.7% fee on international purchases on this card, making it a poor option as a travel card.

Finally, it's recommended that you have a good to excellent FICO score (670 to 850) to apply for the Amex Blue Cash Everyday card. Although you typically need a good credit score to get the best credit cards, this is a particularly high score for a card with no annual fee.

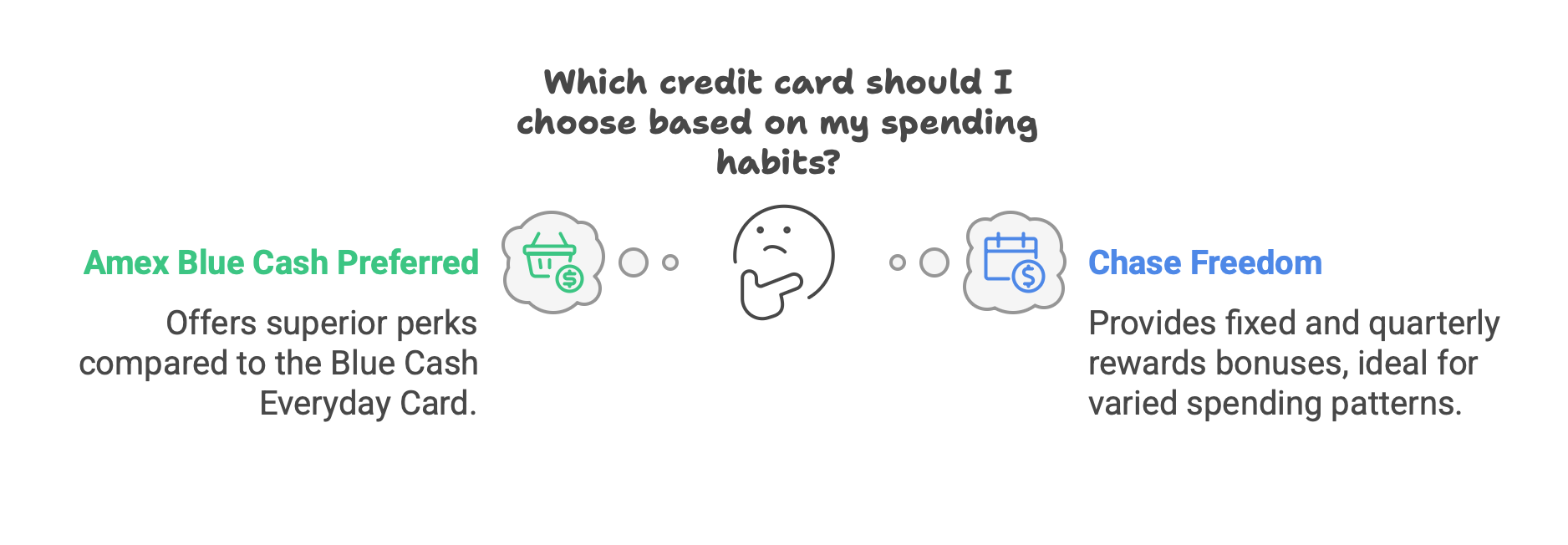

Comparing the Amex Blue Cash Everyday with Similar Cards

The Amex Blue Cash Everyday card is most commonly compared to two other cards: the Amex Blue Cash Preferred card and the Chase Freedom card.

Amex Blue Cash Preferred

Another American Express card, the Blue Cash Preferred card offers no annual fee for the first year and is then $95 per year after. While the annual fee might be a turnoff for some applicants, the Preferred card offers significantly better perks than the Blue Cash Everyday card, including:

- 6% cash-back at U.S. supermarkets (up to $6,000)

- 6% cash-back on U.S. streaming subscriptions

- 3% cash-back at U.S. gas stations (with no spending limit)

- 3% cash-back on transit

The Preferred card also offers a $250 statement credit after spending $3,000 in the first six months, and an intro offer of 0% APR for the first 12 months.

Chase Freedom

Like the Blue Cash Everyday card, the Chase Freedom card has no annual fee and offers cash back on a variety of purchases. It also offers an intro 0% APR for the first 15 months but has a $200 bonus after just $500 of spending within the first three months.

A key difference between how Chase and Amex do rewards, however, is that Chase offers both fixed and quarterly rewards bonuses that incentivize you to spend in different ways. For instance, Chase Freedom offers the following fixed rewards:

- 5% cash back on travel booked through Chase

- 3% cash back on dining

- 3% cash back on drugstore purchases

- 1% on all other purchases

In addition, you can also earn 5% cash back in quarterly bonus categories on up to $1,500 of spending. Bonus categories change every quarter, and you have to activate them to receive the additional rewards. While this is a nice perk, it makes it much more complicated to maximize the Chase Freedom card's value.

Understanding Credit Limits

Your Amex Blue Cash Everyday credit limit is the maximum amount you may spend on the card before making payments on the balance. The credit limit range depends on a number of factors, and you can typically request a credit limit increase if you've experienced an increase in credit score or income. American Express regularly reviews your financial information and may offer a new credit limit during your membership too.

The average credit limit for Amex Blue Cash Everyday cards is $7,479, but the most common limit is $1,000.

Factors Influencing Credit Limits

Your credit limit is primarily informed by your creditworthiness and your income. Most Blue Cash Everyday cardholders have a credit score in the range of 670 to 850, and those with higher scores are more likely to have higher credit limits. If you only barely meet the minimum credit score for approval, you will need to have a significant verified income to get a high credit limit.

Your credit score is calculated using a number of factors, including payment history, credit utilization, length of credit history, and more. Missed payments, using too much of your available credit without being able to pay it back promptly, and opening many new credit cards can all lower your credit score or credit limit.

What credit score do you need for an Amex Blue Cash Everyday?

American Express typically approves Blue Cash Everyday applicants with good to excellent credit (a FICO score of 670 or higher), and approval odds improve meaningfully at 700+. Amex weighs your full credit profile, not just the score: income, debt-to-income ratio, and any prior Amex relationship all factor in.

That doesn't mean a 670 score will get denied. Applicants in the 670 to 699 band often receive starting limits at the floor (around $1,000 to $2,500), while applicants with scores of 720 or higher more frequently see starting limits in the $3,000 to $10,000 range. If your score is below 670, consider building a few months of on-time payment history before applying.

For the full underwriting picture across Amex's lineup, see our Amex approval requirements overview. The CFPB's Consumer Credit Card Market report confirms that issuers like Amex weigh FICO scores heavily for prime, no-annual-fee cards like the Blue Cash Everyday.

How to request a credit limit increase on your Blue Cash Everyday

Once you've held the card for at least 60 days, you can request a credit line increase (CLI) through your Amex online account or the mobile app. The process is straightforward:

- Log in to americanexpress.com and navigate to Account Services, then Card Management, then Increase Credit Limit.

- Enter your updated income and the desired new credit limit. Don't ask for more than a 3x multiple of your current limit — Amex often denies requests that look out of step with the relationship.

- Submit and wait. Most decisions arrive instantly, but some go to manual review (24 to 72 hours).

Amex CLI requests are typically processed as a soft pull, meaning your credit score won't take a hit just from asking. That's a meaningful advantage versus issuers like Capital One or Chase, which often use hard pulls on increase requests. The FTC's guidance for consumers denied credit explains your rights if Amex denies the request — you're entitled to the specific reason in writing.

Amex also runs automatic CLI cadences roughly every 6 months for cardholders in good standing. If you've made on-time payments and your utilization stays under 30%, you may see an unprompted increase without ever asking.

Why is my Amex Blue Cash Everyday limit so low?

If your starting credit limit came in at $1,000 or $1,500 and you expected more, the most common causes are:

- Thin credit file. Newer credit profiles (under 3 years of history) get conservative starting limits regardless of score.

- High existing Amex exposure. Amex looks at total credit lines across all your Amex cards. If you already have a Gold or Platinum charge card or another Blue Cash variant, your Blue Cash Everyday limit may be capped to keep your overall Amex exposure in check.

- Modest reported income. Lower-income applicants get lower starting limits — typical for any prime issuer.

- High utilization on other cards. If your total revolving utilization across all issuers is above 30%, Amex assumes additional credit-line risk.

The fix is patient: keep utilization under 30%, make every payment on time, and request a CLI after 60 days. Most cardholders see their first automatic or requested increase within 6 months. The Federal Reserve G.19 consumer credit data shows revolving credit lines have been climbing nationally over the past 24 months, so issuers like Amex are generally extending more credit than they were two years ago — your timing is decent.

Blue Cash Everyday vs Blue Cash Preferred credit limit

Searchers comparing the Blue Cash Everyday to the Blue Cash Preferred often assume the Preferred carries a higher starting credit limit because of its annual fee. The data doesn't support that assumption. Both cards draw from the same Amex underwriting model — starting limits cluster in the same $1,000 to $10,000 band, and credit profile drives the outcome, not the card tier.

What does differ between the two cards:

The Preferred makes sense if your annual spend at U.S. supermarkets is high enough that the higher cash-back rate beats the annual fee. It does not give you a meaningfully higher starting credit limit, so don't pay the fee for that reason alone.

Choose the Right Card for You with MoneyAtlas

The American Express Blue Cash Everyday card will allow you to earn cash back while shopping for gas, groceries, and more. It has a range of perks, including a $0 annual fee, but it's not without its drawbacks. To compare cards and find the best options for you, check out MoneyAtlas, a platform for expert comparisons of banking, loans, credit cards, and investments.

FAQ

Nick has worked with some of the world's biggest brands and organizations as a copywriter, editor, content manager, and marketing consultant. He's managed editorial e-commerce initiatives with The Walt Disney Company and Hello! Magazine, and developed the brand voice and go-to-market messaging for Fanatics' live commerce platform, Fanatics Live. His written work has appeared on CNN Underscored, PC Mag, TechCrunch, Forbes, Inc., Entrepreneur, and more.

Related Articles

When Does Your Credit Card Charge Interest and How to Avoid It

Wondering when does your credit card charge interest? Learn how grace periods work, how interest is calculated daily, and tips to avoid costly fees.

When Do You Get Interest Charged on Credit Cards

Wondering when do you get interest charged on credit cards? Learn how grace periods, daily compounding, and balance transfers affect your bill today.

When Is Interest Charged on My Credit Card? Understanding the Timing

Wondering when is interest charged on my credit card? Learn how billing cycles, grace periods, and transaction types affect your costs. Avoid fees today!