Blue Cash Everyday® Card from American Express

3% on groceries, gas, and online — no annual fee

Updated July 27, 2026 · By the MoneyAtlas Editorial Team

on BankRate.com's secure site

A $0-fee cash back card that wins on everyday U.S. spending

The 3% back at U.S. supermarkets, gas stations, and online retail with no annual fee makes this a domestic everyday-spend standout, but the $6,000 category caps and 2.7% foreign transaction fee rule it out for heavy spenders and frequent travelers.

3% at U.S. supermarkets, gas stations, and online retail covers the categories most households spend in, but the $6,000 annual cap per category and a flat 1% on everything else hold it back from the top tier.

A $0 annual fee paired with 3% everyday categories and a welcome offer means there is almost no spending level at which the card costs you money.

Amex Offers, purchase and return protection, and Plan It installments are useful, but there are no travel credits or lounge access, and the 2.7% foreign transaction fee is a real drawback abroad.

Cash back posts automatically as Reward Dollars you redeem for statement credit, with no rotating categories to activate, though the per-category caps take a little tracking.

The Blue Cash Everyday® Card from American Express earns cash back on three of the most common spending categories — groceries, gas, and online retail — with no annual fee. The headline rate is 3% in each, capped at $6,000 per year per category, then 1%. There are no rotating quarterly bonuses to track and no points to convert. For most U.S. households that already spend in those buckets, the card pays for itself the first time you fill the cart.

Overview

The Blue Cash Everyday® Card sits in Amex's no-fee Cash Back lineup. It earns flat percentages on category spend, with no rotating calendars, no enrollment, and no points-to-cash conversion. Most of its appeal is in the absence of friction: pay the bill, watch Reward Dollars accumulate.

Features

The core features:

- No annual fee: $0 to carry the card.

- Cash Back rewards: paid as Reward Dollars, redeemable as a statement credit or at Amazon.com checkout.

- Introductory APR: , then .

- Purchase protections: fraud monitoring and return protection on eligible items.

- Entertainment access: Amex presale tickets to select concerts and events.

Annual fee and cost comparison with other cards

The annual fee is $0. That matters most for casual spenders. A $95 fee on the Blue Cash Preferred, for example, requires roughly $3,200 in extra grocery spend a year (at the 3% rate gap) just to break even. Blue Cash Everyday clears that hurdle on day one because the hurdle doesn't exist.

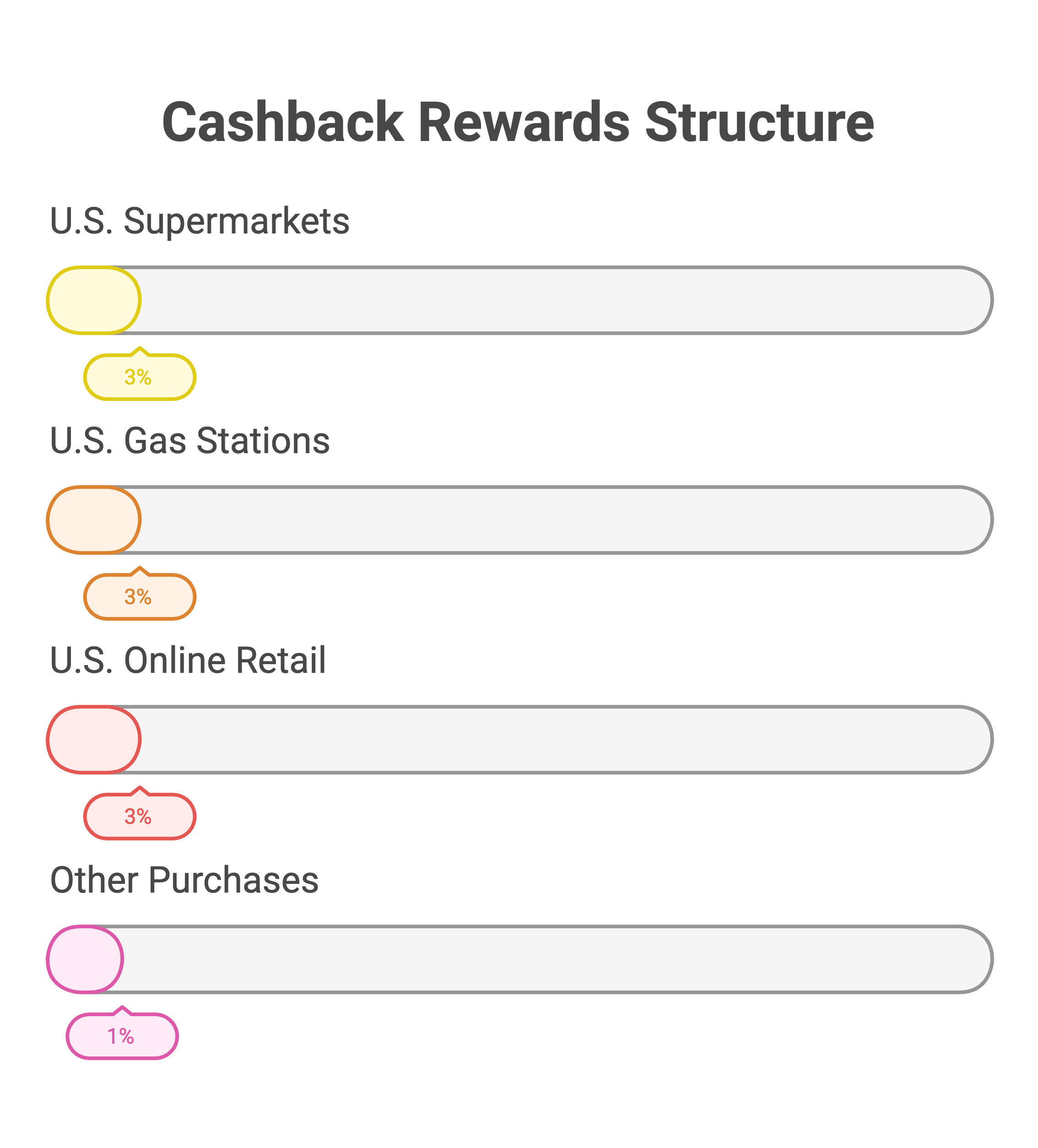

Cash back rewards structure

The structure is flat:

- 3% Cash Back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%).

- 3% Cash Back at U.S. gas stations on up to $6,000 per year (then 1%).

- 3% Cash Back on U.S. online retail purchases on up to $6,000 per year (then 1%).

- 1% Cash Back on other purchases.

If your monthly spending lines up with these three categories, the math is straightforward. If most of your spend is in restaurants, transit, or travel, you'll earn 1% on the bulk of it, and a different card may suit you better.

Benefits

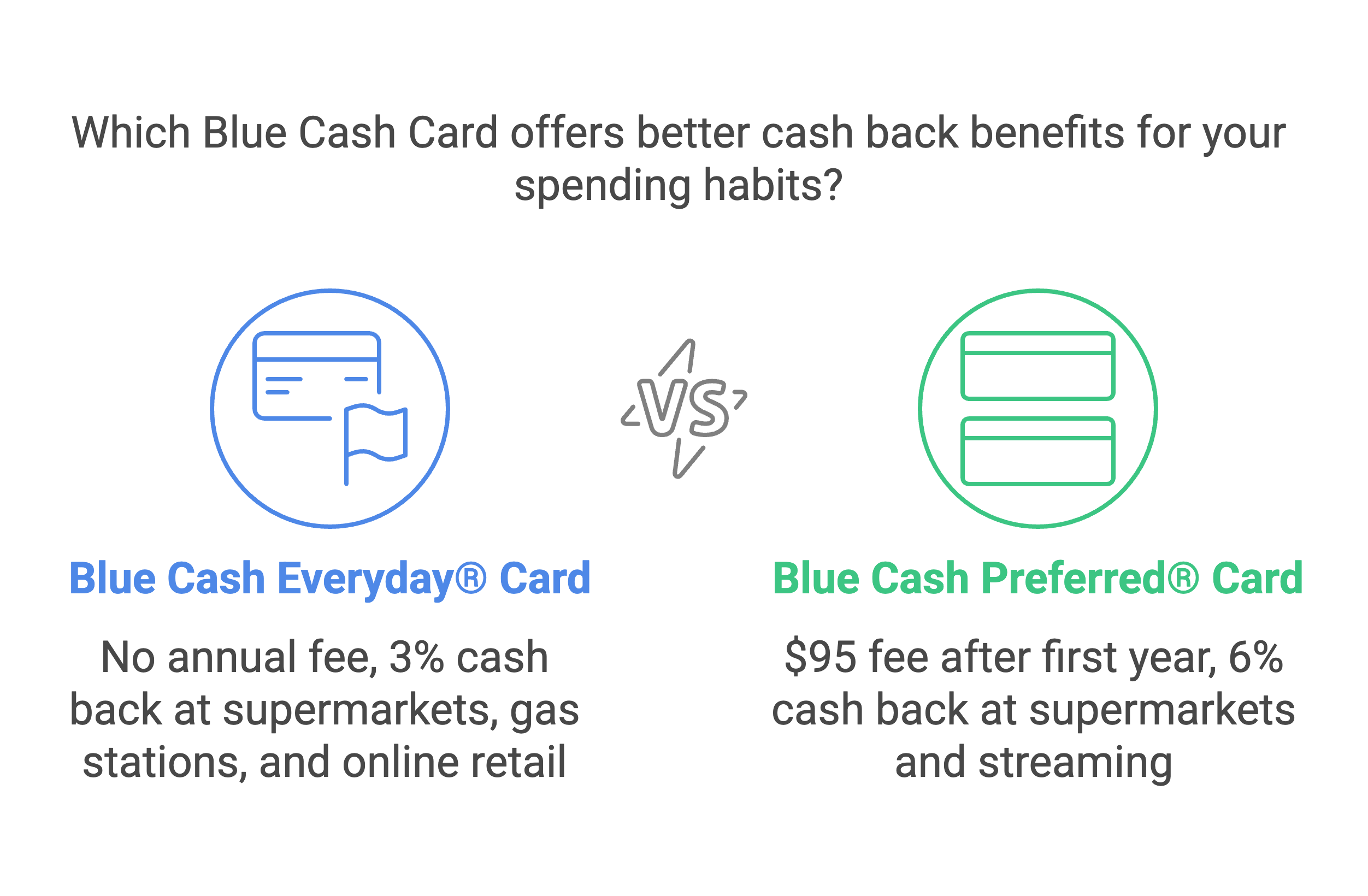

Comparison with the Blue Cash Preferred Card

The Blue Cash Preferred Card is the same family with higher rates and a $95 annual fee. It pays:

- 6% Cash Back at U.S. supermarkets on up to $6,000 per year (then 1%).

- 3% Cash Back at U.S. gas stations and on transit.

The break-even is roughly $3,200 of additional grocery spend per year. That's where the extra 3% on Preferred ($95 fee divided by the 3% rate gap) starts paying you back. Above that, Preferred wins. Below it, Everyday wins.

General rewards and benefits for cardholders

Other cardholder benefits:

- Online account management: review transactions and redeem Reward Dollars in the Amex app or web portal.

- Fraud protection: real-time alerts on suspicious activity, plus Amex's standard chargeback support.

- Amex Offers: rotating statement-credit deals from partner merchants. Available in your account; you opt in per offer.

Considerations for applying

Before you apply, a few things to check.

Credit score requirements

Amex typically approves the Blue Cash Everyday for applicants with a good to excellent credit score (FICO 670+). The score is one input among several. Amex also weighs income, debt levels, and any existing relationship with the issuer. A 700+ score with low utilization is a comfortable margin; below 670 is rarely approved on this card.

Approval difficulty compared to other cash back cards

Amex is selective but not extreme. The Blue Cash Everyday sits closer to the entry tier of the Amex lineup. Easier to get than the Gold or Platinum, harder than most subprime issuers' starter cards. The biggest gates are thin credit files (under two years), recent delinquencies, and high revolving utilization. None of those are automatic deal-breakers, but stack two of them and approval gets uncertain.

Cash advance limits with Amex

Cash advances on the Blue Cash Everyday come with a 29.49% variable APR, a fee of $10 or 5% of the advance (whichever is greater), and no grace period, so interest accrues from day one. The cash advance limit is a sub-limit of your credit line, usually a few hundred to a couple thousand dollars. If you need cash, almost any other route is cheaper.

Compare

Conclusion

Best fit: a household with under $6,000 a year in any single category — groceries, gas, or online retail — that wants a flat 3% without an annual fee. Skip it if you spend heavily abroad (the 2.7% foreign transaction fee adds up) or if your grocery spend tops $6,000 (the Blue Cash Preferred's 6% wins from there).

FAQ

Pros

No annual fee: Nothing to break even on. Every Reward Dollar is profit.

3% on three everyday categories: U.S. supermarkets, U.S. gas stations, and U.S. online retail. Three places most households already spend the bulk of their card budget.

$200 welcome bonus: $200 statement credit after $2,000 in purchases in the first 6 months. Achievable for most households without changing spending habits.

Cons

$6,000 annual cap per category: The 3% rate drops to 1% once you cross $6,000 in any category. Heavy grocery or gas spenders will outgrow it.

2.7% foreign transaction fee: Don't pack this one for international trips (see rates and fees).

Cash Back is paid as Reward Dollars: You redeem them as a statement credit or at Amazon.com checkout. An extra step versus cards that credit cash back automatically.