American Express Approval Requirements: 2026 Credit Score, Income & Eligibility Guide

Most American Express cards require a FICO credit score of 670 or higher for approval, though premium cards like the Amex Platinum and Gold typically require scores of 700 or above. There is no official published minimum, and Amex also considers your income, existing debt, and credit history length when evaluating applications. Below, we break down the specific requirements for each Amex card tier, income thresholds, and the application rules you need to know.

American Express is known for premium credit cards, but great perks often come with stricter qualification standards. If you’re wondering whether you will meet American Express approval requirements, this guide will help you better understand approval odds and credit card applications for the world-class American Express card.

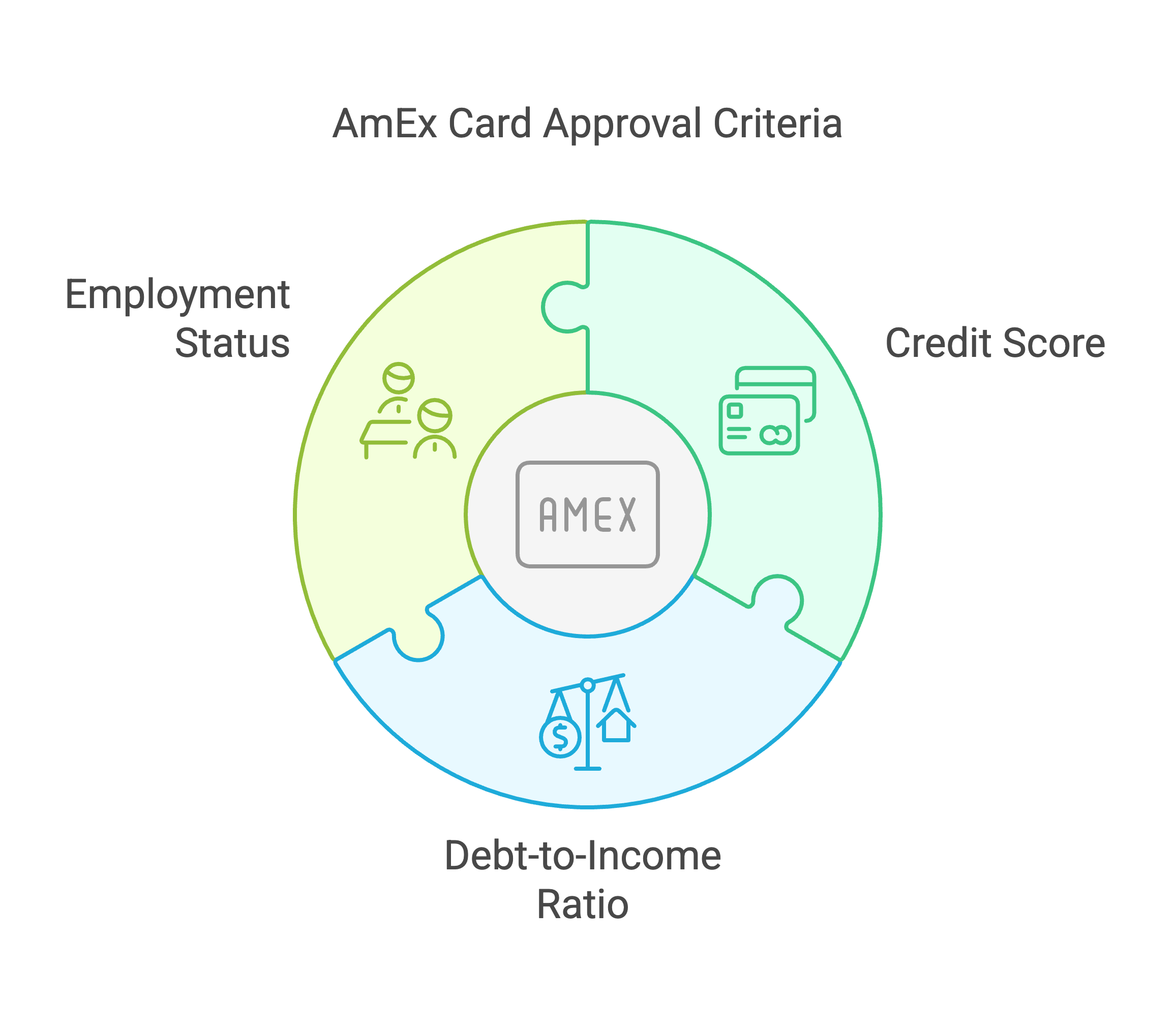

Key Factors Influencing Approval

American Express credit card approval requirements vary based on the card. The key factors influencing approval, however, mirror many other major credit cards, starting with your credit score. These three factors are critical to becoming an authorized user:

- Credit Score Requirements: Unlike some other credit cards, AmEx does not offer a subprime card, which means you need good credit to get approved. Typically, applicants are required to have a credit score of 670 or higher.

- Debt-to-Income Ratio: Your debt-to-income ratio measures the percentage of your monthly income that goes towards paying debts, such as rent or mortgage, car payments, credit cards, child support, and more. To determine your ratio, divide your total monthly debts by your total monthly income. AmEx prefers a debt-to-income ratio in the low 30s or below.

- Employment Status and History: Like many financial institutions, American Express considers your employment status and history as part of your credit card application. Naturally, if you have a stable employment industry with a solid salary, that is an indication that you will be able to make monthly credit card payments.

Understanding Credit Scoring Systems

In a nutshell, a credit scoring system reviews your credit history — including history of repayment, debt, total accounts, and more — to calculate a credit score that predicts the likelihood that you will miss a payment by at least 90 days in the next two years.

FICO Score Explained

FICO scores range from 300 to 850, and most lenders use them to determine your creditworthiness. FICO, which stands for Fair Isaac Corporation, creates ratings based on the following scale:

- Excellent: 800–850

- Very Good: 740–799

- Good: 670–739

- Fair: 580–669

- Poor: 300–579

VantageScore Overview

The three major credit rating agencies developed an alternative to FICO scores: the VantageScore. It also ranges from 300 to 850 and uses machine learning for its analytics, but its ranges are slightly different from FICO’s:

- Excellent: 750–850

- Good: 700–749

- Poor: 550–649

- Very Poor: 300–549

While FICO scores are still the most common form of credit scoring, VantageScore is growing rapidly. Both can provide a picture of your current credit status and future ability to make payments.

Tips for Improving Your Credit Score

If your credit score isn't already in the "excellent" range, you can take several steps to improve it.

Strategies to Boost Your Score

One of the best things you can do to boost your credit score is to make on-time payments for your other credit cards, rent or mortgage, and other monthly bills. Late and missed payments are reported to the national credit bureaus and can drag your score down, but timely payments will always work in your favor. If you struggle with remembering to make monthly payments, consider autopay options through your bank.

Other smart strategies include paying down balances, avoiding new credit applications, maintaining your oldest accounts for the sake of your credit history, and having a family member add you as an authorized user on their card, as long as they have a good payment history.

Monitoring Your Credit Report

Equifax, Experian, and TransUnion — the three national credit reporting bureaus — are required by law to provide a free annual credit report. If you haven't checked yours out lately, go for it! You might be surprised at errors or inaccuracies, which, when fixed, can help to boost your credit score.

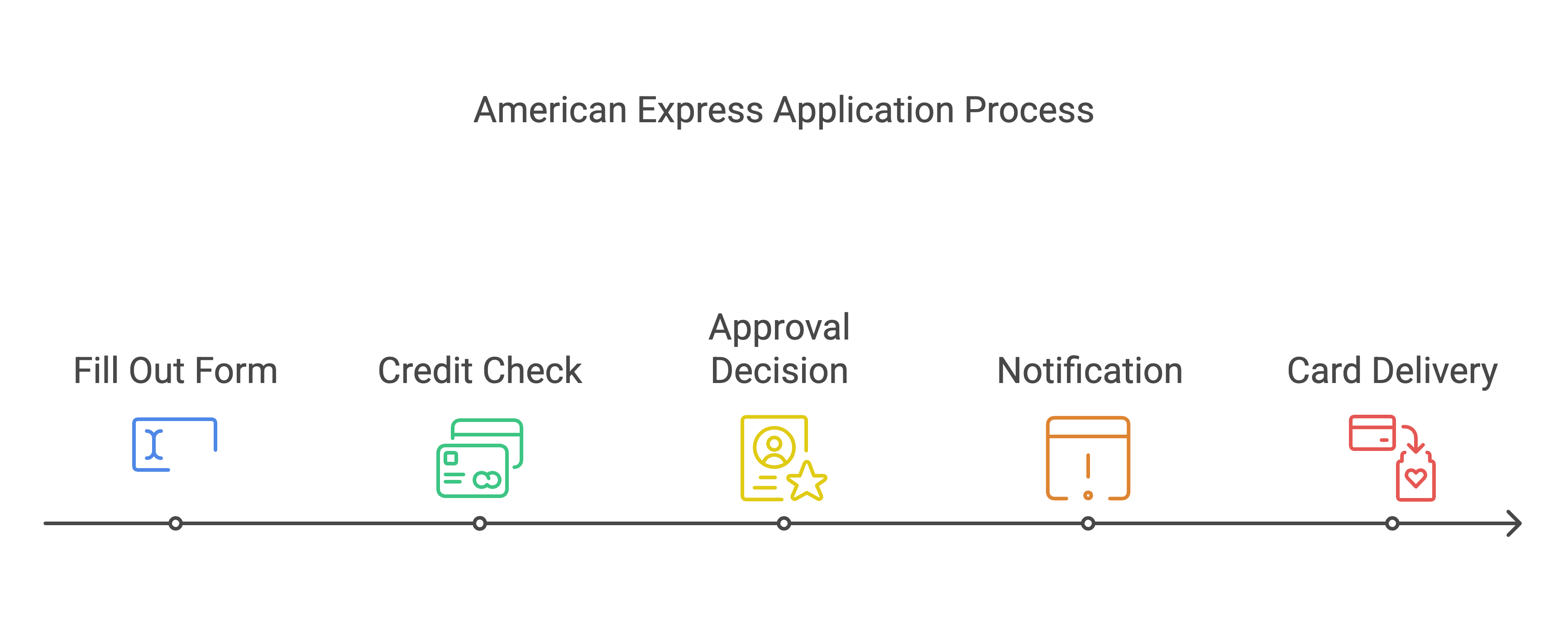

How the American Express Approval Process Works

You can apply for an American Express online in about 10 minutes after reading the Terms and Conditions, although requirements can vary per card. American Express Platinum approval requirements may vary slightly from card approval requirements, for instance.

Application Process Overview

The typical process is as follows.

- You fill out a form with your personal and financial information.

- American Express checks your credit history and credit score.

- You may receive an automatic approval, or American Express may use a manual review to check tax and employment information.

- You are notified of AmEx's decision.

If your application is approved, you should receive your new card within three to five business days.

Pre-qualification: What It Is and How It Works

Much like it sounds, pre-qualification is a pre-screening that will give you a better idea of your likelihood of approval. American Express can perform a "soft" credit check that doesn't affect your credit score as a pre-qualification.

You can "apply with confidence" online for three different cards to determine your pre-qualification status.

American Express Application Rules

Not surprisingly, AmEx has several rules when it comes to applying for its coveted credit cards.

Number of Applications and Impact on Approval

You can only be approved for an AmEx card once every five days, and for two cards within 90 days. You will max out at five personal and business cards total.

Multiple Applications

If you do the math, that means you must wait at least six days between card applications if you are applying for multiple American Express cards. After that, you must wait another 90 days for any additional applications. Note that charge cards do not count toward the five-card limit, only personal credit cards do. Amex also enforces a once-per-lifetime welcome bonus rule, meaning you cannot earn the sign-up bonus on a card you have held before, even if the account was closed years ago. Some applicants also encounter "Pop-Up Jail," an informal term for a message shown during application indicating you may not be eligible for the welcome bonus based on your prior history with American Express.

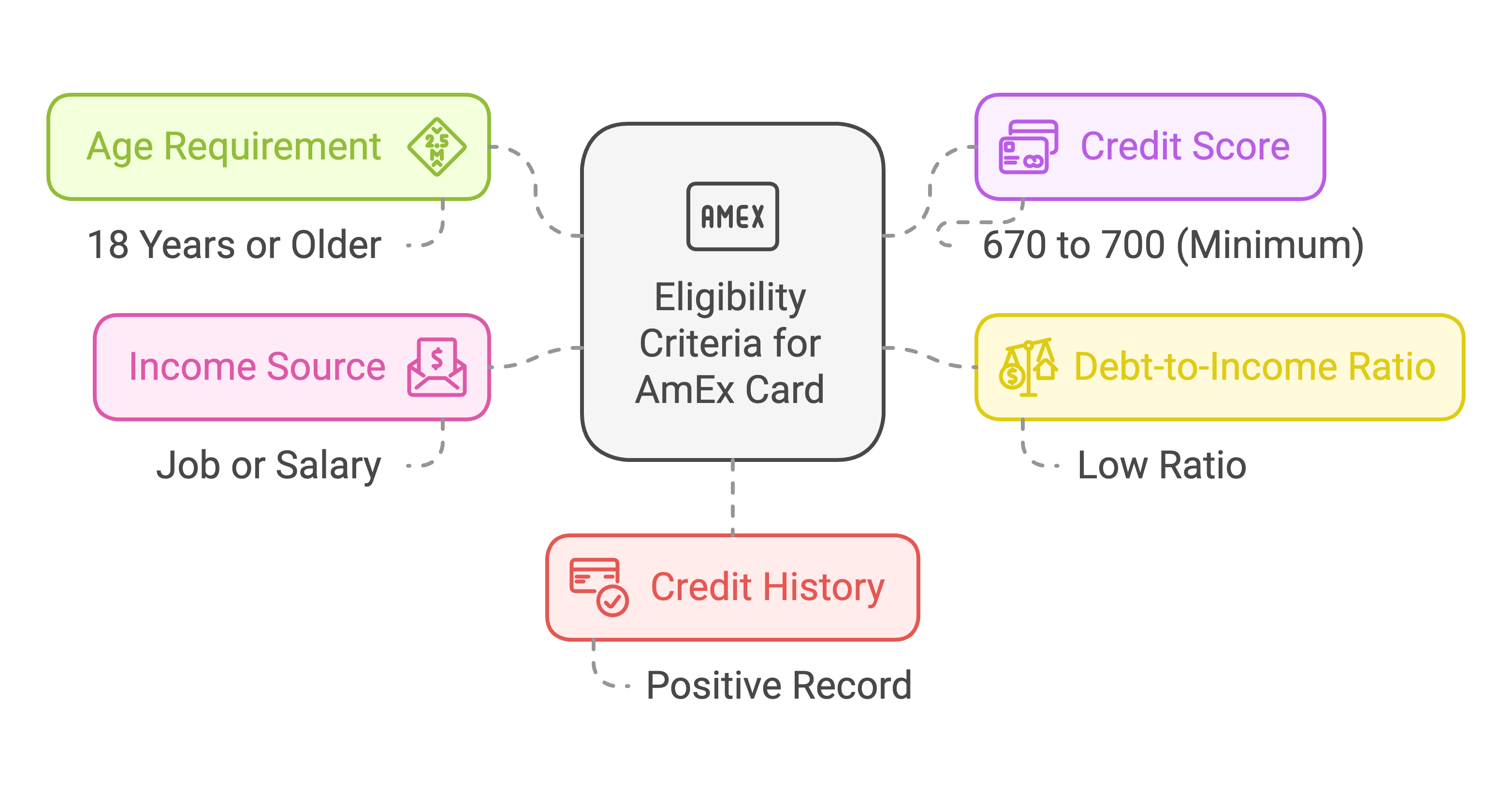

Essential Qualifications for AmEx Card Applications

Eligibility criteria can vary based on the specific card.

General Eligibility Criteria

In general, to be eligible for an AmEx card, you will need to meet these requirements:

- Be at least 18 years old

- Have a minimum credit score of 670 to 700

- Have a low debt-to-income ratio

- Have a reliable source of income

- Have a solid credit history

Specific Requirements for Select Cards

Every AmEx card requires a good to excellent credit score. Beyond that, here are some specific requirements for select cards:

- American Express Centurion (Black) Card: You must receive an invitation to apply for this exclusive card.

- The American Express Gold Card requires a good credit score while the Platinum Business American Express Card, which is harder to earn and has a higher annual fee as well as better rewards, requires an excellent score. The Platinum is great for luxury travel benefits, while the Gold is a great option for earning everyday spending.

AmEx also offers a guide to "leveling up" when it comes to cards, their colors, and their associated perks.

Card-by-Card Requirements

Each American Express card has different approval thresholds. Entry-level cards like the Blue Cash Everyday and Amex EveryDay are accessible with good credit scores starting around 670, modest income, and limited credit history. Mid-tier cards like the Amex Gold and Blue Cash Preferred typically require scores of 690 or higher with a demonstrated history of on-time payments and moderate income. Premium cards like the Amex Platinum, Delta SkyMiles Reserve, and the Centurion (Black) Card demand excellent credit scores of 720 or above, higher income levels, and a strong relationship with American Express. Business cards like the Blue Business Plus and Business Gold generally require a personal score of 670 or higher plus demonstrated business income or revenue.

Income Requirements for American Express

American Express does not publish a specific minimum income for most cards, but your reported income is a significant factor in approval decisions and directly affects your credit limit. When filling out an application, you can include your personal salary, household income (if you are 21 or older), regular contributions from others, and investment income. Amex may request income verification through tax returns or pay stubs, especially for premium cards or high credit limit requests. For entry-level cards, applicants reporting annual income as low as $25,000 to $35,000 are commonly approved, while premium cards like the Platinum generally favor applicants reporting $75,000 or more.

What to Do If You're Denied an American Express Card

Roughly one in five Amex applicants is declined on the first review, but a denial is not the end of the road. The reason on your adverse-action letter — sent within 30 days under the Fair Credit Reporting Act — tells you exactly what tripped the algorithm and gives you a starting point to fix it.

Common denial reasons

- Credit score below the card's threshold (most common — pulls from Experian for personal cards, Equifax or TransUnion for business).

- Too many recent inquiries (six or more hard pulls in 12 months is a red flag).

- High revolving credit utilization (above 30% across all cards).

- Limited or thin credit file (under two years of history).

- Income reported is too low for the card requested, or doesn't match what's on file with credit bureaus.

- Recent late payments, charge-offs, bankruptcies, or other derogatory marks within the last 7 years.

- You've previously had an Amex account closed by the issuer (a near-permanent disqualifier).

Calling the Amex reconsideration line

American Express runs a reconsideration line at 1-800-567-1083 (personal cards) and 1-866-314-0237 (business cards). A live underwriter can re-evaluate your application without pulling a second hard inquiry. Call within seven days of the denial decision while the file is still active, have the application reference number from your letter ready, and be prepared to explain (a) why you applied, (b) how you plan to use the card, and (c) any one-time event that suppressed your score (medical bill, divorce, recent move). About a third of denials are overturned on the recon call when the applicant is calm, prepared, and has the cleanest possible explanation.

When to reapply

If the recon call doesn't work, wait at least 90 days before reapplying for the same card. During that window, focus on the specific issue from the adverse-action letter: pay down balances to under 10% utilization, dispute any inaccurate items on your credit report with Equifax, Experian, and TransUnion, and avoid any new hard inquiries. Reapplying inside 90 days with the same underlying credit profile almost always produces the same denial.

How to Improve Your Approval Odds Before Applying

Amex's underwriting model rewards applicants who look low-risk on the day of application. Five concrete steps in the 30 to 60 days before you apply move the needle the most:

Pre-application checklist

- Pay revolving balances down to 10% or less of your credit limits before your statement closes — this is the credit-utilization ratio that posts to the bureaus and is one of the heaviest weighted FICO inputs.

- Pull your credit reports from each of the three bureaus and dispute any inaccurate negative items (incorrect late payments, accounts that aren't yours, debts past the 7-year reporting window).

- Avoid any new hard inquiries for at least 90 days before applying — that includes auto loans, mortgage pre-approvals, and other credit card applications.

- Use Amex's CardMatch tool, which performs a soft pull and tells you which cards you are pre-qualified for without affecting your credit score. Pre-qualified offers convert to approval at roughly 80%.

- Make sure your address, employer, and reported income on the application match what's already on file with the bureaus and prior creditors. Mismatches can trigger a manual review and slow down or sink the approval.

- Consider freezing your reports at Experian (the bureau Amex pulls personal cards from) only on the day of application — not before. A frozen report at the time of pull will cause an automatic decline.

Compare

Best Amex Cards by Credit Tier

The right Amex card depends on where your credit score actually sits today. The list below maps each major Amex personal card to the typical credit-tier range of approved applicants, drawn from publicly aggregated apply outcomes and the Federal Reserve's Survey of Consumer Finances income data. Use it as a starting point — Amex's underwriting also weighs income, utilization, and existing relationship.

Fair credit (580–669): Limited Amex options at this range. Strong applicants with low utilization can sometimes qualify for the no-annual-fee Delta SkyMiles Blue or for Amex's secured Optima card (invitation-only after a closed account). Most personal Amex cards target 670+, so it's usually worth spending 3 to 6 months building score first.

Good credit (670–739): This is the heart of Amex's approval band. Top picks include the Amex Blue Cash Everyday (no annual fee, cash back on groceries and gas), the Hilton Honors American Express Card for travelers, and — for applicants in the upper end of this tier — the American Express Gold Card or Blue Cash Preferred.

Excellent credit (740+): Premium Amex products are squarely in reach. The flagship Platinum Card from American Express carries the heaviest fee-and-credits package in the lineup. The Delta SkyMiles Reserve is the top pick for frequent Delta flyers. Approval at this tier is largely about income reported and existing Amex relationship rather than the score itself.

For a broader cross-issuer comparison covering Amex alongside Chase, Capital One, and Citi cards, see our guide to the best credit cards updated for 2026.

Frequently Asked Questions

Personal Finance and Freelance Writer

Education

- Bachelor’s Degree in Journalism, Northwestern University

- Master’s Degree in English, University of South Dakota

Expertise

- Budgeting and personal finance

- Family finance

- Small business

Related Articles

Why Do Credit Cards Charge Interest on Purchases?

Why do credit cards charge interest on purchases? Learn how revolving loans, risk, and the grace period affect your balance and how to avoid extra costs.

Why Do Banks Charge Interest on Credit Cards?

Ever wonder why do banks charge interest on credit cards? Learn how banks manage risk, calculate daily interest, and how you can avoid fees entirely.

Why Is My Credit Card Not Charging Interest?

Wondering why is my credit card not charging interest? Learn about grace periods, 0% APR offers, and refunds to manage your balance effectively.