How to Calculate APR on a Credit Card Per Month

Introduction

Understanding how to calculate APR on a credit card per month is a critical skill for anyone carrying a balance. Most people see the Annual Percentage Rate, or APR, on their monthly statement but are unsure how that percentage translates into a specific dollar amount. While the APR represents the cost of borrowing over a full year, interest is typically calculated on a daily or monthly basis.

MoneyAtlas tracks these rates and provides side-by-side credit card comparisons to help consumers see how different interest levels impact their total debt over time. This guide breaks down the math behind interest charges, the importance of your average daily balance, and how to verify the numbers on your statement. Knowing these mechanics allows for better decision-making when comparing credit products or planning a debt payoff strategy.

What is APR and How Does it Differ from Interest?

Annual Percentage Rate (APR) represents the yearly cost of borrowing money on a credit card. It includes the interest rate and any specific fees the lender might include, though for most credit cards, the APR and the interest rate are essentially the same number. However, even though the rate is stated as an annual figure, banks do not wait until the end of the year to charge you.

The interest rate is the percentage charged on the principal amount borrowed. On a credit card, this is a revolving cost. If you want a deeper explanation of the term itself, our guide on what APR is on a credit card is a helpful companion piece. If you pay your statement in full every month, you typically benefit from a grace period where no interest is charged. If a balance remains after the due date, the APR is applied to that debt.

Monthly periodic rates are the intervals at which interest is actually assessed. Most credit card issuers use a daily periodic rate rather than a monthly one to account for the fact that your balance changes as you make purchases or payments throughout the month. For a broader look at how this math works in practice, see how APR works on a credit card. This distinction is important because it affects how the final finance charge is calculated on your statement.

The Mathematical Formula for Monthly Interest

Calculating your interest charge requires three specific pieces of information from your statement. You need your current APR, your average daily balance, and the number of days in your current billing cycle. Most billing cycles run between 28 and 31 days.

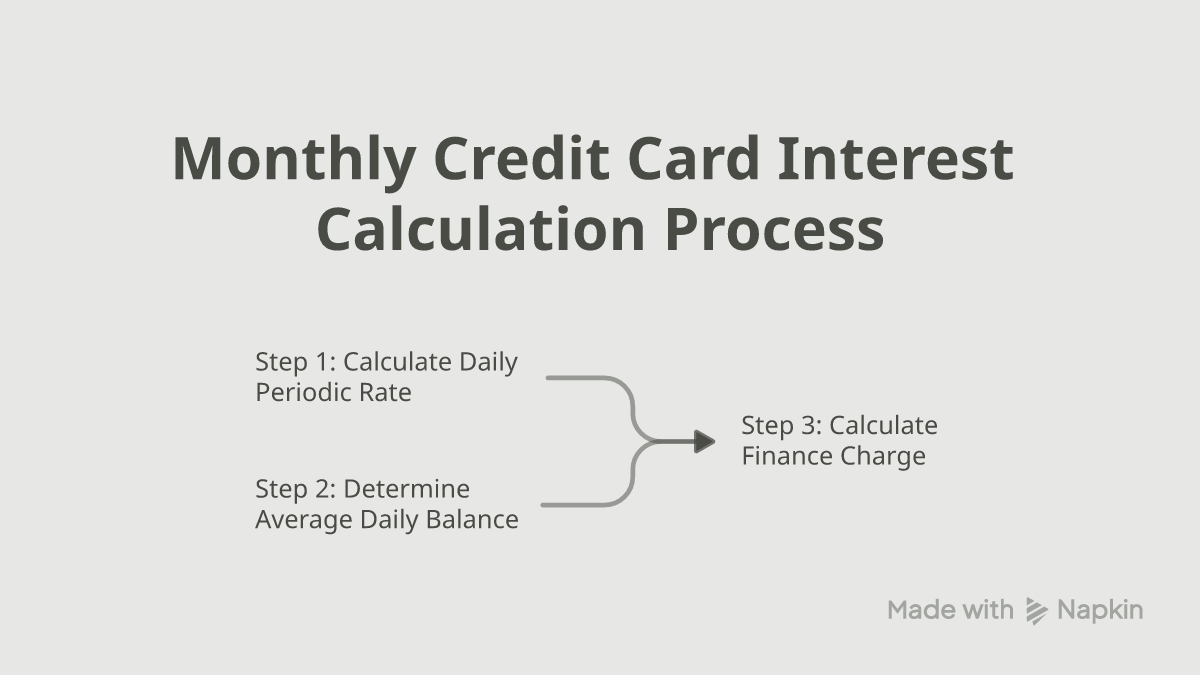

Step 1: Calculate the Daily Periodic Rate

Because interest usually compounds daily, you must first convert your annual rate into a daily one. To do this, divide your APR by 365. For example, if a card has a 24% APR, the calculation is 0.24 divided by 365. This results in a daily periodic rate of approximately 0.000657, or 0.0657%.

Step 2: Determine the Average Daily Balance

The bank does not simply look at your balance on the last day of the month. Instead, they calculate how much you owed on each individual day of the cycle. They add these daily totals together and divide by the number of days in the cycle. This means making a large payment early in the month reduces your interest more than making that same payment on the last day.

Step 3: Calculate the Finance Charge

Once you have the daily rate and the average daily balance, multiply them together. Then, multiply that total by the number of days in your billing cycle. The final number is the interest charge that will appear on your statement.

Why the Average Daily Balance is the Most Important Factor

The average daily balance method is the standard way issuers determine how much you owe. This method is more complex than simply looking at your ending balance, but it is more accurate for a revolving line of credit. Every time you buy a coffee or pay a bill, your balance changes, and the daily interest follows suit.

A credit card billing cycle is the period between your last statement and your current one. If you start the month with a $500 balance and pay it down to $0 on day 15, your average daily balance for a 30-day month would be $250. This is because you owed $500 for half the month and $0 for the other half. If you waited until day 29 to pay, your average daily balance would be much closer to $500.

Transactions take time to post to your account. Generally, the date a transaction occurs is different from the date it "posts" or is officially added to your balance. Interest begins accruing on the posting date. Understanding this delay is helpful when trying to calculate your daily balance exactly.

How Daily Compounding Accelerates Interest

Most credit card companies use daily compounding for interest charges. Compounding means that the interest you earned yesterday is added to your principal balance today. Consequently, tomorrow's interest is calculated on a slightly higher amount than today's interest.

The difference between simple interest and compounding interest is small over one month but large over a year. Over the course of 30 days, the "interest on interest" might only amount to a few cents. However, if a balance is carried for 12 months, daily compounding causes the effective rate you pay to be higher than the stated APR.

This effective rate is sometimes referred to as the Annual Percentage Yield (APY). While APY is more common in savings accounts, the same logic applies to debt. A 24% APR compounded daily actually feels like a higher percentage to the borrower over a long period. This is why credit card debt can feel like it is growing faster than expected even if no new purchases are made.

Different APRs for Different Transactions

One statement can contain multiple different APRs. It is a common misconception that a single rate applies to everything you do with a credit card. Most issuers break down your activity into three main categories: purchases, balance transfers, and cash advances.

Purchase APR is the standard rate applied to things you buy at a store or online. This is usually the lowest of the non-promotional rates. If you have a good credit score, this rate will likely be lower than if your score is in the fair or poor range.

Cash Advance APR is typically much higher than the purchase APR. A cash advance occurs when you use your credit card to get physical cash from an ATM or a bank teller. These transactions usually do not have a grace period. Interest starts accruing the moment the cash is in your hand.

Balance Transfer APR applies to debt moved from one card to another. Many cards offer a promotional 0% APR on balance transfers for a set period, such as 12 to 18 months. For a closer look at that strategy, read how credit card balance transfers work. After that period ends, the remaining balance is subject to a standard balance transfer APR, which may differ from your purchase rate.

The Power of the Grace Period

A grace period is the time between the end of a billing cycle and the date your payment is due. According to federal law, if an issuer offers a grace period, they must mail or deliver your bill at least 21 days before the due date. Most cards offer a grace period of 21 to 25 days.

To maintain your grace period, you must pay the entire statement balance by the due date. If you do this, the issuer will not charge any interest on the purchases made during that cycle. This effectively makes the credit card a free short-term loan.

If you carry even a small balance into the next month, you lose the grace period. This is known as "trailing interest" or "residual interest." Even if you pay your next statement in full, you might still see an interest charge on the following bill. This is because interest was accruing on the balance during the days between the statement closing and the date the bank received your payment.

How Your Credit Score Influences Your APR

Lenders use your credit score to determine how much of a risk you are. A higher credit score typically leads to a lower APR offer. Credit scores are calculated based on your payment history, the amount of debt you owe, the length of your credit history, and other factors.

Variable APRs are tied to the Prime Rate. Most credit cards have variable rates, meaning they can change when the Federal Reserve adjusts interest rates. When the Federal Reserve raises rates, the Prime Rate usually goes up, and your credit card APR will follow. This happens regardless of your individual credit behavior.

Penalty APRs can be triggered by late payments. If you are more than 60 days late on a payment, an issuer might raise your APR to a much higher "penalty rate," which can sometimes exceed 29%. This rate can apply to both your existing balance and future purchases. Maintaining an on-time payment history is the best way to avoid these extreme costs.

Evaluating Promotional 0% APR Offers

Many credit cards offer a 0% introductory APR for a limited time. These offers are popular for people looking to finance a large purchase or pay down existing debt without interest getting in the way. MoneyAtlas allows users to compare these promotional offers side by side to see which one provides the longest window.

Deferred interest is different from a 0% APR offer. You will often see deferred interest at furniture stores or electronics retailers. If the balance is not paid in full by the end of the promotional period, the issuer may charge you all the interest that would have accumulated from the very first day of the purchase. This can result in a massive, unexpected charge.

Standard 0% APR offers do not charge retroactive interest. If you have a remaining balance when the 0% period on a standard credit card ends, you will only be charged interest on the remaining amount going forward. It is still vital to read the fine print to confirm which type of offer you are accepting.

Steps to Verify the Interest on Your Statement

If you suspect your interest charge is incorrect, you can manually verify it. While banks use automated systems that are rarely wrong about the math, errors can occur in how transactions are categorized or how payments are applied.

How to Verify the Interest on Your Statement

- 1

Check your billing cycle length

Look for the "Statement Period" on your bill. Count the number of days between the start and end dates.

- 2

Locate your daily periodic rate

This is often listed in a section called "Interest Charge Calculation" or "Information About Your Account." If it isn't listed, divide your stated APR by 365.

- 3

Audit your daily balances

This is the most tedious step. Start with your previous balance, then add or subtract each transaction based on the date it posted. This will give you the balance for each day.

- 4

Perform the final math

Add all daily balances, divide by the number of days, multiply by the daily rate, and then multiply by the total days in the cycle. If your result is within a few cents of the statement charge, the calculation is correct.

How to Lower the Amount of Interest You Pay

The most effective way to lower interest is to pay more than the minimum. Even adding $20 or $50 to your monthly payment can significantly reduce the amount of principal that is subject to interest the following month.

Changing your payment date can also help. If you get paid on the 1st of the month but your credit card bill isn't due until the 20th, paying as soon as you get your paycheck will lower your average daily balance for those 20 days. This results in a lower interest charge even if you don't increase the total amount you pay.

Consider a balance transfer to a lower-rate card. For those carrying significant debt at a high APR, moving that balance to a card with a 0% introductory rate can save hundreds or thousands of dollars. If you are comparing that option, start with balance transfer cards and then review the fine print on the cards that fit your credit profile.

Making a Smart Decision on Your Next Card

Not all APRs are created equal. When looking for a new credit card, the "headline" APR you see in an advertisement is often a range. The rate you actually receive depends on your creditworthiness at the time of application.

Compare the total cost of ownership. A card with a lower APR might have an annual fee, while a card with a higher APR might have no fee but better rewards. If you never carry a balance, the APR is irrelevant and you should focus on rewards. If you do carry a balance, the APR is the most important factor. If you are trying to avoid yearly fees altogether, compare no annual fee credit cards alongside the rest of your options.

Use comparison tools to see the fine print. MoneyAtlas reviews over 1,500 financial products, making it easier to see the daily periodic rates, penalty APRs, and grace period terms of various cards side by side. Taking the time to compare ensures you aren't surprised by how your monthly interest is calculated once you start using the card. For a broader browse page, you can also start at all credit card reviews before narrowing down the products that fit your needs.

Summary Checklist for Calculating Monthly APR

To stay on top of your credit card costs, keep this checklist in mind when your statement arrives:

- Confirm the APR: Check if your rate has changed due to a variable rate adjustment or the end of a promotional period.

- Identify the Cycle: Note if your billing cycle was 28, 30, or 31 days.

- Calculate Daily Rate: Divide your APR by 365 to understand the daily cost.

- Review Daily Activity: See if large purchases were made early in the month, which increases the average daily balance.

- Check Transaction Types: Ensure cash advances or transfers aren't being charged a higher rate than you expected.

- Verify the Grace Period: Ensure you haven't lost your interest-free window by carrying a balance from the previous month.

Understanding the mechanics of interest calculation turns a mysterious finance charge into a manageable variable. By knowing exactly how the bank arrives at that number, you can take practical steps to reduce your costs and pay off your debt faster.

FAQ

Conclusion

Mastering the calculation of credit card interest takes the guesswork out of your monthly finances. By understanding that your APR is actually a daily cost applied to an average of your daily balances, you can see exactly how your spending and payment habits impact your bottom line. Whether you are looking to avoid interest entirely through a grace period or are trying to minimize the cost of a revolving balance, the math remains the same.

To find a card that better suits your financial needs, use the comparison tools on MoneyAtlas to evaluate current APRs, promotional offers, and fee structures. Comparing your options side by side is the most effective way to ensure you are not paying more for credit than necessary.

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

How to Evaluate Credit Card Annual Fees Interest Rates Rewards

Learn how to evaluate credit card annual fees interest rates rewards to maximize value. Master the math behind APR and perks to pick your perfect card.

How to Calculate the Interest Rate on a Credit Card

Learn how to calculate the interest rate on a credit card using your APR and average daily balance. Follow our simple guide to master your debt today!

How to Lower Interest Rates on Credit Card Accounts

Learn how to lower interest rates on credit card accounts through negotiation, 0% balance transfers, or consolidation to save money and pay off debt faster.