How 0% APR Credit Cards Work: Terms, Fees, and Timelines

Introduction

A 0% APR credit card is a financial tool designed to provide a temporary window where interest charges are suspended on specific types of transactions. Most people look for these cards when they need to finance a large purchase or move existing high-interest debt to a more manageable account. Understanding how 0% APR credit cards work is the first step toward using them effectively. MoneyAtlas helps readers compare these offers side by side in our best credit cards comparison to see which terms fit their specific goals. These cards operate on a strict timeline, and the promotional period eventually gives way to a standard interest rate. This article explains the mechanics of zero-interest periods, the importance of the fine print, and how to evaluate different offers before applying.

The Definition of 0% APR

Annual Percentage Rate, or APR, represents the yearly cost of borrowing money on a credit card. It includes the interest rate and certain other costs, expressed as a percentage. If you want a deeper refresher on rates, see our guide to APR on a credit card. While most credit cards charge an interest rate that fluctuates based on the market and your creditworthiness, a 0% APR card sets that rate to zero for a limited time.

This 0% rate is almost always an introductory offer. It is intended to attract new customers by giving them a "grace period" that lasts much longer than the standard 21 to 25 days found on most monthly statements. During this time, the cost of carrying a balance is eliminated, provided you follow the rules of the card agreement.

It is helpful to view the 0% APR as a bridge. It allows you to move from a high-interest situation or a large upcoming expense to a zero-balance state without the friction of compounding interest. However, this bridge has a clear end point.

How the Introductory Period Functions

When you open a 0% APR card, the clock starts immediately. The introductory period is the specific number of months that the 0% rate remains in effect. The length of this window varies significantly between different products.

Most competitive offers on the market today range from 12 to 18 months, though some cards extend this to 21 months or more. MoneyAtlas tracks these durations across hundreds of cards to help users identify which ones offer the longest windows.

The Impact of the Start Date

The promotional period usually begins on the date the account is opened, not the date you receive the card in the mail or the date of your first purchase. This distinction is important for anyone planning a major project, like a home renovation or a wedding. If you apply for the card too early, you may lose several weeks of the interest-free window before you even begin spending.

Requirements for Minimum Payments

A 0% APR is not a "payment holiday." You are still required to make at least the minimum monthly payment by the due date every single month. If you fail to make a payment, the consequences are often swift. Many card issuers include a clause that allows them to terminate the 0% offer immediately if a payment is missed. In some cases, a late payment could even trigger a penalty APR, which is significantly higher than the standard rate.

Types of 0% APR Offers

Not every 0% offer applies to every transaction. Credit cards generally have different interest rates for different ways of using the card. You must verify which category the 0% offer covers. If you are comparing payoff-focused cards, start with our balance transfer card comparison.

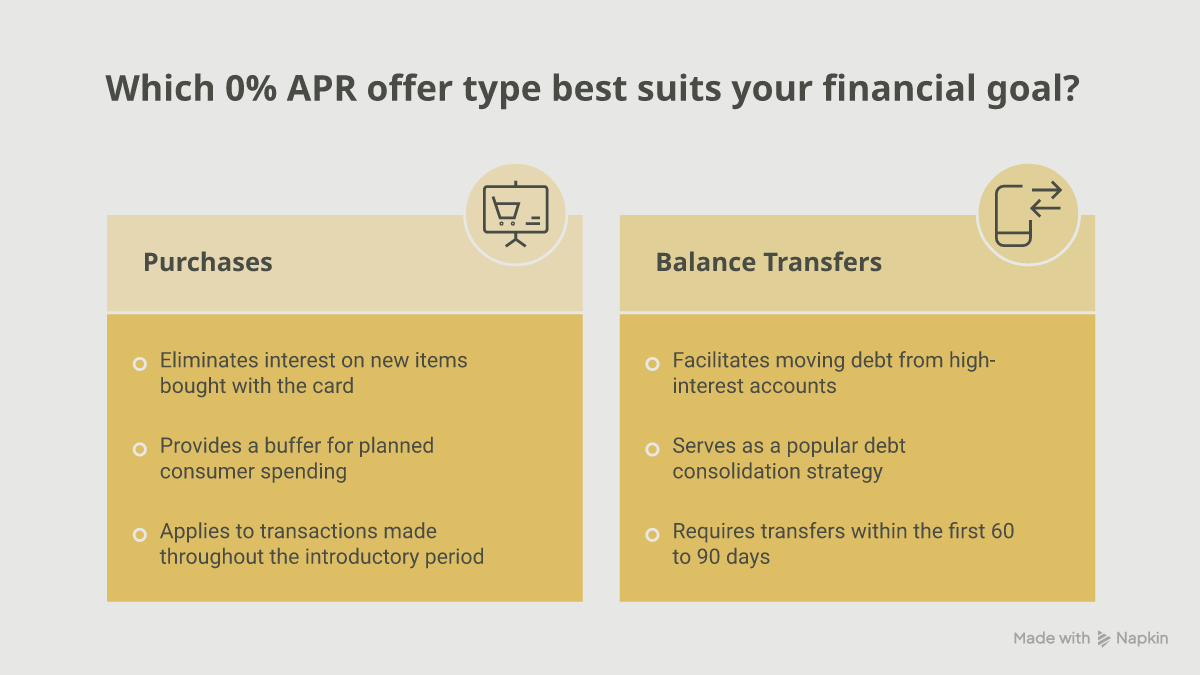

0% Intro APR on Purchases

This offer applies to new items or services you buy with the card. If you use the card to buy a $2,000 refrigerator, that $2,000 balance will not accrue interest during the intro period. This is a common choice for people who have a specific, large expense coming up and want to pay it off over a year or more without extra costs.

0% Intro APR on Balance Transfers

A balance transfer is when you move debt from one credit card to another. This is a popular strategy for debt consolidation. If you have a $5,000 balance on a card charging 24% interest, moving it to a 0% APR card allows every dollar of your payment to go toward the principal balance rather than interest.

Combined Offers

Some cards offer 0% on both purchases and balance transfers. However, the length of the periods may differ. For example, a card might offer 15 months of 0% interest on purchases but only 12 months on balance transfers. It is also common for the 0% balance transfer offer to only apply to transfers made within the first 60 or 90 days of account opening.

The Role of the Schumer Box

Every credit card offer in the United States includes a standardized table known as a Schumer Box. This table is required by law and provides a clear breakdown of the rates and fees. When comparing 0% APR cards, the Schumer Box is the most reliable place to find the actual terms. For a broader product overview, you can also browse our credit card reviews index.

In this table, you should look for the following:

- Introductory APR: The 0% rate and exactly which transactions it covers.

- Duration: How many months or billing cycles the rate lasts.

- Ongoing APR: The interest rate that will apply after the 0% period ends. This is often a range, such as 18.24% to 29.24%, based on your credit score.

- Balance Transfer Fee: The cost to move debt to the card.

- Annual Fee: Whether the card charges a yearly fee just for having the account.

Using these facts allows for an apples-to-apples comparison. MoneyAtlas makes it easier to compare these specific data points side by side so you can see which card actually costs the least over time.

Understanding Balance Transfer Fees

While the interest rate may be 0%, moving a balance is rarely free. Most issuers charge a balance transfer fee, which is typically a percentage of the total amount you move.

Common fees are 3% or 5% of the transferred amount. For example, if you transfer $10,000 to a new card with a 5% fee, the issuer will add $500 to your balance immediately. Your starting balance on the new card would be $10,500. If you want to compare a specific no-fee option, check the Capital One Quicksilver Cash Rewards Credit Card review.

Even with this fee, a 0% APR card usually saves the borrower money. If you are paying 25% interest on $10,000, you are accruing roughly $200 in interest every month. In that scenario, paying a one-time $500 fee to stop the $200 monthly interest charge pays for itself in less than three months.

What Happens When the 0% Period Ends?

The transition from a 0% rate to a standard rate can be a significant financial shock if you are not prepared. Once the introductory window closes, any remaining balance on the card is subject to the ongoing APR.

Credit card interest is compounded, usually on a daily basis. If you have $3,000 left on the card when the 0% period expires and your new APR is 24%, you will start seeing significant interest charges on your next statement. The issuer is not required to send you a warning that your promotional rate is about to end. It is your responsibility to track the calendar. If you want to understand what happens to credit when accounts change, see whether closing a credit card hurts your score.

Planning for the "Cliff"

A successful strategy involves dividing your total balance by the number of months in the intro period. If you have a $6,000 balance and a 12-month window, paying $500 per month ensures you hit a zero balance before the interest kicks in.

0% APR vs. Deferred Interest

It is vital to distinguish between a true 0% APR credit card and a "deferred interest" offer. Deferred interest is most common with store-branded credit cards or medical financing.

With a true 0% APR card, if you have a balance left when the period ends, you only pay interest on that remaining amount going forward. With deferred interest, the rules are different. If you fail to pay off the entire balance by the deadline, the issuer will charge you interest on the full original purchase amount, retroactively, from the day you bought it.

For example, if you buy a $2,000 couch on a 12-month deferred interest plan and still owe $50 at the end of month 12, the store will add 12 months of interest on the full $2,000 to your bill. True 0% APR cards from major lenders do not typically use this retroactive model. Always check the terms for the words "no interest if paid in full" to identify deferred interest traps.

How 0% APR Cards Affect Credit Scores

Opening and using a 0% APR card impacts your credit profile in several ways. While these cards can be part of a healthy financial strategy, you should be aware of how they interact with credit reporting.

Hard Inquiries

Applying for any new credit card results in a hard inquiry on your credit report. This usually causes a small, temporary dip in your credit score. If you apply for multiple cards in a short period, the impact can be more significant.

Credit Utilization

Your credit utilization ratio is the amount of credit you are using compared to your total credit limits. It is a major factor in your credit score. If you use a 0% APR card to finance a $5,000 purchase and your credit limit is $6,000, your utilization on that card is 83%. This high utilization can lower your credit score even if you are not paying interest. For a closer look at this factor, read how credit utilization affects your score.

Conversely, if you use a 0% APR card to pay off debt and close out other high-interest balances, your score might eventually improve as your total debt decreases.

Average Age of Accounts

A new card lowers the average age of your credit accounts. This is a smaller factor in your score, but it is something to consider if you have a relatively short credit history.

Qualifying for a 0% APR Card

Introductory 0% offers are generally reserved for borrowers with good to excellent credit. This typically means a FICO score of 670 or higher, though the most competitive offers with the longest periods often require scores above 740.

Lenders also look at your income and existing debt levels to determine your credit limit. You might apply for a card hoping to transfer $10,000 in debt, but the lender may only approve you for a $5,000 limit. In this case, you would only be able to move a portion of your debt. MoneyAtlas provides reviews that often list the typical credit ranges needed for specific cards to help you gauge your chances of approval.

Steps to Take Before Applying

Steps to Take Before Applying for a 0% APR Card

- 1

Check your score

Knowing where you stand helps you target cards you are likely to qualify for.

- 2

Total your debt

If you are doing a balance transfer, know the exact amount and the current interest rates.

- 3

Read the Schumer Box

Confirm whether the 0% applies to purchases, transfers, or both.

- 4

Calculate the fee

Factor in the 3% or 5% transfer fee to ensure the move is cost-effective.

How to Compare Different 0% Offers

When you are ready to choose a card, you should evaluate the offers based on your specific goal.

For Debt Consolidation

Focus on the length of the 0% balance transfer window and the cost of the transfer fee. A card with a 21-month window and a 5% fee might be better than a card with a 12-month window and a 3% fee if you need the extra time to pay off a large balance. Use our cash back credit cards comparison to see which cards currently offer the lowest fees.

For New Purchases

Focus on the 0% purchase APR duration and whether the card offers any rewards. If you are spending $5,000 on a new deck, you might as well earn 1.5% or 2% cash back on that purchase while also getting the 0% interest period.

For Long-Term Use

Consider the ongoing APR and the annual fee. If you plan to keep the card for years after the 0% period ends, a card with no annual fee and a lower standard APR is more valuable than a card with a long intro period but a high yearly cost. For a fee-free option, review our no annual fee credit cards comparison.

Managing Your Card Responsibly

Once you have the card, the goal is to maximize the interest-free period without creating new financial problems.

- Set up autopay: Ensure you never miss the minimum payment, which protects your 0% rate and your credit score.

- Avoid new debt: If you are using the card for a balance transfer, try to avoid making new purchases on it. This keeps the balance clear and easier to track.

- Mark the expiration date: Put the date the 0% period ends on your calendar. Aim to have the balance paid off one month early to avoid any surprise interest charges.

- Monitor your statements: Even with 0% interest, fees or other charges can appear. Check your statement monthly for accuracy.

If you want more background on rate mechanics, the article what a balance transfer does and why it matters is a helpful next read.

Conclusion

How 0% APR credit cards work is straightforward: they offer a temporary break from interest to help you manage costs. However, the details in the Schumer Box determine the real value of the offer. By paying attention to balance transfer fees, the length of the introductory window, and the ongoing APR, you can choose a card that aligns with your financial needs. The most effective way to use these cards is to have a clear payoff plan and a firm understanding of when the promotional rate ends. We invite you to use the MoneyAtlas comparison tools to browse current 0% APR offers and find the card that fits your timeline and credit profile. If you want to compare individual cards next, start with our product reviews index.

- Determine your goal: Decide if you need to finance a purchase or consolidate debt.

- Calculate your monthly payment: Divide your total balance by the intro months to find your target payment.

- Compare fees: Look for cards with low or no balance transfer fees.

- Watch the clock: Ensure the balance is gone before the standard APR kicks in.

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

Will Capital One Lower Interest Rate On Credit Card?

Wondering if will Capital One lower interest rate on credit card? Learn how to negotiate a lower APR, use Eno, or qualify for hardship programs to save money.

Will Credit Cards Lower Your Interest Rate if You Ask?

Will credit cards lower your interest rate if you ask? Yes! Learn the exact steps to negotiate a lower APR, save on interest, and cut your debt faster.

Will Credit Card Interest Rates Ever Go Down?

Will credit card interest rates ever go down? Explore 2026 APR forecasts and learn proactive strategies to lower your interest rates today.