Brokerage Account vs Mutual Fund: Pros, Cons & Best Uses

Deciding between a brokerage account vs. mutual fund? Both can be valuable tools in securing your financial future. But they’re not mutually exclusive. In fact, you can invest in mutual funds through a brokerage account. Here's what you need to know.

Brokerage Account vs. Mutual Fund: Side-by-Side Comparison

Pros of Brokerage Accounts

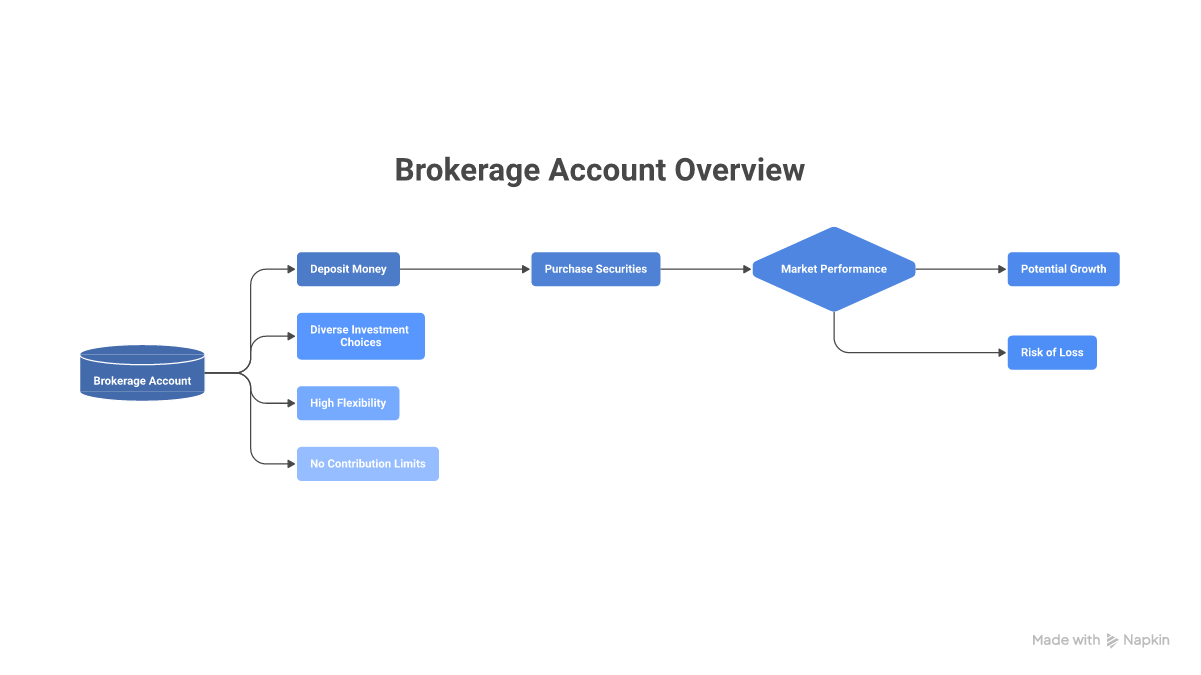

What is a brokerage account? It's a type of account you can open through a brokerage firm. The money you deposit can be used to purchase individual securities, like stocks and bonds, or funds. This means your money can gain or lose value based on market performance. The growth potential of a brokerage account is generally higher than that of a traditional savings account, but this ultimately depends on the investments you select.

Advantages of a brokerage account include:

- Diverse investment choices: You can hold a variety of investment vehicles inside a standard brokerage account, including stocks, bonds, exchange-traded funds (ETFs), and mutual funds.

- High flexibility: You can choose how to invest based on your unique needs, risk tolerance, and financial goals.

- No contribution limits: Unlike individual retirement accounts (IRAs), there are no contribution limits or penalties for early withdrawals.

Cons of Brokerage Accounts

There are some drawbacks to brokerage accounts, but that doesn’t mean you shouldn’t use them. What’s important is that you weigh your options carefully and have a robust understanding of how they work.

Here are some potential downsides:

- Market volatility: When choosing between a brokerage account or a high-yield savings account, consider the impact of market volatility. Unlike bank deposits, the value of funds invested in a brokerage can rise or fall depending on business and economic conditions.

- Tax and fee considerations: Unlike IRA contributions, brokerage account contributions aren't tax-advantaged. You'll pay taxes annually based on interest, dividends, and capital gains received. You may also have to pay commissions for trades, though many discount brokers offer trading at a reduced cost.

- Opportunity costs: While cash in your brokerage account is highly liquid, invested money isn’t readily available until you sell.

Pros of Mutual Funds

Are mutual funds brokerage accounts? No, a mutual fund is a professionally managed fund that takes your and other investors' money and invests it in different securities. You can invest in mutual funds through a general brokerage or advisory account, a retirement account, or directly through a mutual fund company. If you choose the former, you should understand the difference between advisory and brokerage accounts. With the latter, make sure you do your research to ensure the investment firm you choose is trustworthy and reputable.

Regardless of how you invest in them, mutual funds can be excellent additions to your investment portfolio. Here are some of the key benefits:

- Investment diversification: A mutual fund highlight is diversification. Each fund holds a mix of stocks, bonds, and other assets.

- Professional management: Many mutual funds are actively managed by financial experts who monitor business and market performance and make changes to the fund's makeup over time. Contrast this with different types of brokerage accounts, many of which are self-directed, meaning you make investment decisions on your own.

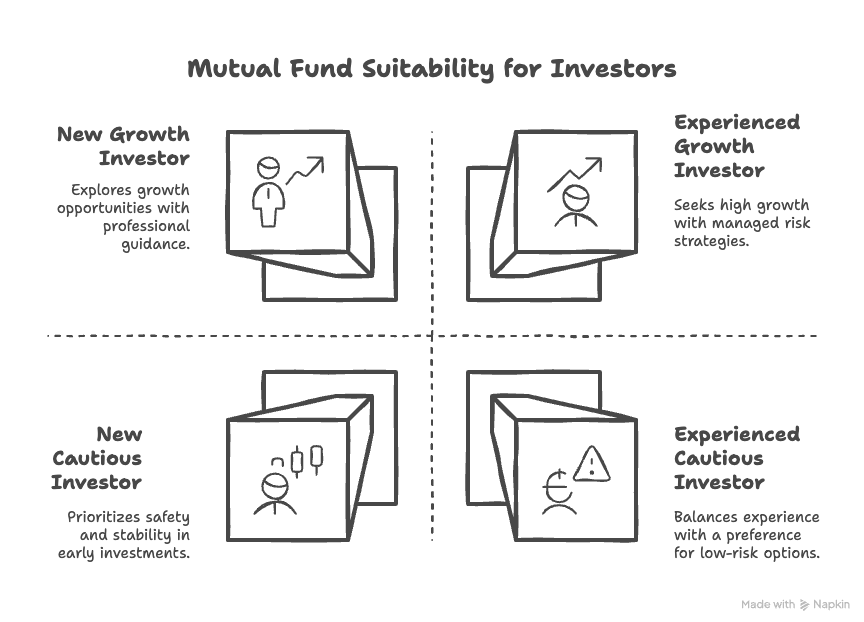

- Lower risk for new investors: Investing in a diversified portfolio of securities is generally less risky than investing in a single stock. While a holding within the fund may suffer from poor performance, other holdings' performance may lessen the overall loss.

Cons of Mutual Funds

Mutual funds are great if you want an actively managed portfolio. But if you’re a new investor or don’t have time to investigate specific mutual funds, you might want to consider ETFs as an alternative. ETFs often track a specific index, like the S&P 500, or sector, like technology. They provide similar diversity to a mutual fund with greater visibility into holdings and a lower cost.

Here are a few drawbacks of investing in mutual funds:

- Higher ongoing fees: Because they're actively managed, mutual funds tend to have higher expense ratios than ETFs.

- Structural constraints: Due to the fund's mandate, which you can learn more about in the prospectus, there may be limitations on the fund manager's ability to respond to volatile market conditions or make other changes.

- Limited control: With mutual funds and ETFs, you typically don't have much say in how your money is invested.

Best Uses for Brokerage Accounts

The key to getting the most out of your brokerage account is understanding when and how to use it to pursue your financial goals.

Brokerage accounts are especially effective if you’re saving up for a big purchase, trying to grow generational wealth, or supplementing your retirement savings and hoping to avoid early withdrawal fees in an IRA or 401(k).

Best Uses for Mutual Funds

Mutual fund shares can play a key role in your portfolio, whether you purchase them from a brokerage firm or directly. You can target specific areas of the market, like large-cap growth companies or corporate bonds, in a relatively affordable way.

They’re a good option for new investors who can benefit from professional management services, as well as for cautious investors and those close to retirement, as they tend to be less volatile than individual stocks.

Key Differences Between Brokerage Accounts and Mutual Funds and How to Choose the Best Option

When comparing a brokerage account vs. a mutual fund, remember that a mutual fund is an investment in and of itself. With a brokerage account, you haven’t actually invested in anything until you purchase securities.

Mutual funds are a type of security. When you buy into a mutual fund, you’re investing in the hope that your money will grow over time or generate capital gain distributions.

For most investors, a brokerage account is a great vehicle for consolidating a variety of investments. The best brokerage accounts for mutual funds include household names like Vanguard, SoFi, Robinhood, Fidelity, and Schwab.

Can You Hold a Mutual Fund Inside a Brokerage Account?

Yes — and that is the most common setup. The Securities and Exchange Commission defines a brokerage account as an account you open with a broker-dealer to buy and sell investments. Once the account is open, you can use it to purchase mutual funds, ETFs, individual stocks, and bonds — the fund is held inside the account.

If you buy a fund directly from a mutual fund company instead, you skip the brokerage account — but you also limit yourself to that one company's funds. Most investors open a brokerage account first so they can mix and match across providers, then add a mutual fund (or several) inside it.

Tax Treatment: A Worked Example

Both accounts trigger taxes in a taxable (non-retirement) context, but the timing is different. Say you invest $10,000 and earn a 7% annual return for 5 years — roughly $4,026 in gains.

In a brokerage account, you decide when to sell. If you hold the position the entire 5 years and then sell, you owe long-term capital gains tax on the ~$4,026 gain — typically 0%, 15%, or 20% depending on income. You also owe annual tax on any dividends paid out along the way.

Inside an actively managed mutual fund, the fund manager buys and sells securities throughout the year. Those internal trades generate capital-gains distributions that are passed to you — and you owe tax on them in the year they are declared, even if you never sold a single share of the fund yourself. Two investors with identical holdings can end up with very different tax bills depending on the wrapper.

Index mutual funds and ETFs typically distribute far less than actively managed funds, which is why many tax-sensitive investors prefer them. The takeaway: the account is just a container, but the kind of fund you put inside it changes when the IRS gets paid.

How to Choose Between a Brokerage Account and a Mutual Fund

Choose based on what is actually missing from your plan. If you do not yet have an investment account, the question is settled — you need a brokerage account first. The mutual fund question only matters once an account is open and you are picking what to hold.

Open a brokerage account if you want flexibility, no contribution caps on the account itself, and the option to mix asset types in one place. Add an actively managed mutual fund if you want a professional team handling allocation decisions and you are comfortable paying a higher expense ratio for it. Add an index mutual fund or ETF instead if you want diversification at the lowest possible cost. For most everyday investors, that last combination — a brokerage account holding low-cost index funds — does the work of both.

Choosing Between Brokerage Accounts and Mutual Funds With Money Atlas

Brokerage accounts and mutual funds can be used separately and together as part of an overall financial strategy. Brokerage accounts offer excellent flexibility and customizability, while mutual funds give you professional management at a relatively low cost. Regardless of whether you use one or both, incorporating these investment vehicles into your approach can play a role in helping you build wealth.

Ready to make your next investment? Check out Money Atlas' list of the best online brokerages.

FAQ

Emily Pitkin

Education

- Bachelor of Science Degree in Economics, Portland State University

- Master of Arts in Professional Writing, New England College

Expertise

- Long-term Investing and Retirement Planning

- Budgeting and Saving

- Debt Management Strategies

- Small Business Development

Related Articles

Roth IRA vs. Brokerage Account: Which One Is Right for Your Investment Goals?

Not sure whether to invest in a Roth IRA or a brokerage account? Compare tax benefits, risks, and long-term growth potential to make the right choice.

The Safest Crypto Exchanges: How to Choose a Secure Platform for Trading

Looking for a safe crypto exchange? Discover the most secure platforms for trading, key security features, and tips to protect your investments.

Brokerage Account vs. High-Yield Savings: Where to Keep Each Dollar in 2026

HYSA pays guaranteed interest with FDIC insurance; a brokerage account targets higher long-term returns with risk. Compare both side-by-side and see which one fits each saving goal.