What Is a Penalty APR for Credit Cards and How Does It Work?

Introduction

A penalty APR is a significantly higher interest rate that a credit card issuer applies to an account after the cardholder violates specific terms of the credit agreement. Most people encounter this rate after missing a payment by 60 days or more, though other violations like returned payments can also trigger it. This rate is often the highest possible interest rate allowed on the card, frequently reaching near 30%.

MoneyAtlas compares thousands of financial products to help you understand how different terms impact your wallet. This post covers how penalty APRs are triggered, how long they last, and how you can avoid or resolve them. Understanding these rules is essential for anyone carrying a balance, as a penalty APR can drastically increase the cost of debt overnight. By learning the mechanics of these rates, you can better navigate the terms of your current cards or compare new options that do not include these punitive measures.

If you want a broader refresher on how card interest works, start with our guide to what APR means in credit card accounts. For readers comparing offers before applying, the best credit cards comparison is a helpful place to begin.

How a Penalty APR Works

A credit card agreement is a contract between you and the issuer. In exchange for the ability to borrow money, you agree to follow certain rules. If those rules are broken, the issuer has the right to adjust the cost of that borrowing. The penalty APR serves as a financial consequence for high-risk behavior, such as falling significantly behind on payments.

When a penalty APR is triggered, it typically replaces your standard purchase APR. If your card usually charges 19% interest, a jump to a penalty rate of 29.99% represents a 50% increase in your interest costs. This change does not happen instantly or without warning. Under the Credit CARD Act of 2009, issuers must follow specific protocols before they can hike your rate due to a violation.

One of the most important protections is the notice period. Issuers must provide a written notice at least 45 days before the higher rate takes effect. This notice must explain the reason for the increase and state the new rate. It is also important to note that while a penalty APR is a major financial hurdle, it is not a permanent label for your account if you take the right steps to correct it.

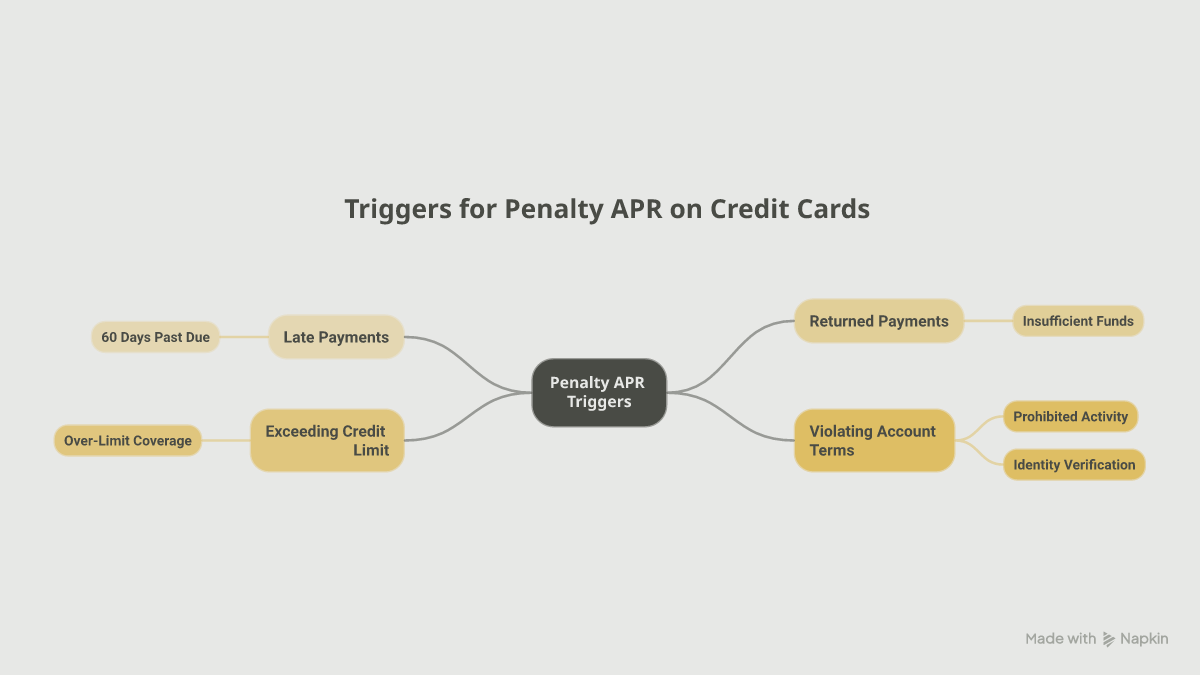

Common Triggers for a Penalty APR

Not every mistake leads to a penalty rate. Issuers generally reserve this measure for significant or repeated violations. While every bank has its own specific terms, there are four common reasons a penalty APR might appear on your statement.

Late Payments

This is the most frequent trigger. Most issuers do not apply a penalty APR the moment you are one day late. Instead, they typically wait until a payment is at least 60 days past due. A 60% delay in payment signals to the bank that the risk of default has increased. However, some cards may trigger the rate after only one or two missed payments, so checking the fine print in your agreement is vital.

Returned Payments

If you attempt to pay your bill and the payment is returned because of insufficient funds in your bank account, the issuer may view this as a violation. A returned payment can incur both a flat fee and a trigger for the penalty APR. This is especially common if you have multiple returned payments within a short timeframe.

Exceeding the Credit Limit

While less common today than it was in the past, some issuers still include "over the limit" violations as a trigger for a penalty APR. Most modern cards simply decline transactions that would exceed your limit unless you have specifically opted into over-the-limit coverage. If you have opted in, exceeding that limit can lead to a rate hike.

Violating Other Account Terms

Every credit card has a list of terms and conditions. Violating these, such as using the card for prohibited activities or failing to comply with identity verification requests, can sometimes result in the application of a penalty rate.

The Cost of a Penalty APR

The financial impact of a penalty APR is significant because of how interest compounds. Most credit cards calculate interest daily based on your average daily balance. When the APR jumps from a standard rate to a penalty rate, the daily interest charge grows proportionally.

Consider an example. If you have a $5,000 balance on a card with a 20% APR, you are paying roughly $82 in interest per month. If that rate jumps to a 29.99% penalty APR, your monthly interest cost increases to approximately $123. Over six months, this represents an extra $246 in interest charges alone.

These rates are often variable. They are calculated by taking a fixed margin set by the bank and adding it to a benchmark rate, which is usually the U.S. Prime Rate. For a broader look at current borrowing costs, MoneyAtlas’s current APR guide for credit cards is a useful companion read.

How Long Does a Penalty APR Last?

A penalty APR does not have to be a permanent fixture of your credit card account. Federal law provides a path for cardholders to earn back their original interest rate. However, the rules differ slightly depending on whether the rate applies to your existing balance or only to new purchases.

The Six-Month Rule

If an issuer applies a penalty APR to your existing balance because you are 60 days late, the law requires them to review your account after six months. If you make six consecutive on-time payments during that period, the issuer must restore your original purchase APR to that existing balance. This ensures that cardholders who demonstrate a return to responsible habits are not punished indefinitely.

Future Purchases

The rules for future purchases are less strict. While the issuer must revert the rate on your old balance after six months of on-time payments, they are sometimes permitted to keep the penalty APR in place for any new purchases you make. Some issuers choose to revert the entire account back to the standard rate as a gesture of goodwill or to encourage continued use of the card, but they are not always legally required to do so for new spending.

Indefinite Penalty Rates

If you continue to miss payments or violate terms during the six-month probationary period, the penalty APR can remain in effect indefinitely. In these cases, the bank is not required to lower the rate until you have successfully completed a full six-month cycle of on-time payments.

Impact on Credit Scores

A common misconception is that the penalty APR itself lowers your credit score. This is not technically true. Credit bureaus like Experian, Equifax, and TransUnion do not track the specific interest rates you are charged. Your credit report shows your balances, your limits, and your payment history, but not your APR.

However, the actions that trigger a penalty APR are incredibly damaging to your credit score. Payment history is the single most important factor in FICO and VantageScore models, accounting for roughly 35% of your total score. A payment that is 60 days late can cause a score to drop by 50 to 100 points, depending on your starting score.

Furthermore, a higher interest rate leads to faster balance growth if you only pay the minimum. This increases your credit utilization ratio, which is the amount of credit you are using compared to your total limits. High utilization is the second most important factor in credit scoring, meaning a penalty APR can indirectly lead to a lower score by making it harder to keep your balances down.

If you are trying to rebuild after a late payment, cards for fair credit can be a practical next step. Another helpful resource is MoneyAtlas’s guide on how to lower credit card APR.

Strategies to Avoid a Penalty APR

Prevention is the most effective way to deal with penalty interest. Since these rates are triggered by specific behaviors, you can implement systems to ensure those behaviors do not occur.

Enroll in Autopay

Setting up automatic payments for at least the minimum amount due is the best defense against a penalty APR. Even if you cannot pay the full balance, an automatic minimum payment ensures you are never technically "late" in the eyes of the issuer. Most banks allow you to schedule this for a few days before the actual due date to provide a buffer.

Monitor Account Balances

To avoid returned payments, you must ensure your checking account has enough funds to cover your credit card payments. Setting up low-balance alerts on your bank account can help you stay aware of your available cash before an automatic payment is processed.

Set Calendar Reminders

If you prefer to pay your bills manually, do not rely on your memory alone. Set recurring reminders on your phone or computer. Many people find success by aligning their credit card due dates with their paydays. Most issuers allow you to move your due date to a specific day of the month that works better for your cash flow.

Communicate Early

If you are facing a financial hardship that makes it impossible to pay the minimum, contact your issuer before you miss the due date. Many banks have hardship programs that can temporarily lower your interest rate or move your payment date without triggering a penalty APR. They are generally more willing to help a customer who reaches out before a violation occurs.

What to Do if You Are Already Charged a Penalty APR

If you have received a notice that a penalty APR is being applied, you still have options to mitigate the damage. The goal is to minimize the interest you pay while working toward restoring your standard rate.

What to Do if You Are Already Charged a Penalty APR

- 1

Prioritize On-Time Payments

Your first priority is to start the six-month clock for the rate review. You must make every single payment on time for the next half-year. Even one day of lateness will reset the clock, forcing you to start the six-month period over again.

- 2

Stop Using the Card for New Purchases

If the penalty APR applies to new purchases, every dollar you spend will immediately begin accruing interest at the higher rate. It is often a better decision to stop using that specific card and switch to a different card with a standard APR or use cash until your original rate is restored.

- 3

Increase Your Monthly Payments

Since interest is accruing at a much faster rate, paying only the minimum will result in very little of your money going toward the actual debt. If possible, increase your monthly payment. Every extra dollar you pay reduces the principal balance, which in turn reduces the amount of interest the bank can charge you the following month.

- 4

Explore a Balance Transfer

If your credit score is still high enough, you might consider a balance transfer to a different card. Some cards offer a 0% introductory APR on transfers for 12 to 21 months. Moving your high-interest debt to a 0% or low-interest card can save you hundreds of dollars in interest and give you a clear path to paying off the balance. You can use the balance transfer card comparison to look at current options side by side.

Credit Cards Without a Penalty APR

Some credit card issuers differentiate themselves by promising never to charge a penalty APR. These cards are worth comparing if you are concerned about the occasional late payment or if you are new to managing credit and want a safety net.

Cards with no penalty APR still charge interest, and they will still charge late fees in most cases. The primary benefit is that your interest rate will remain stable even if you miss a payment. If you want cards that keep costs simpler, the no annual fee credit card comparison can be a useful place to look, especially if you want to avoid extra annual charges too.

When choosing a card, do not assume that a "no late fee" card also means "no penalty APR." These are two different types of penalties. A late fee is a one-time charge, while a penalty APR is an ongoing increase in the cost of your debt.

MoneyAtlas makes it easier to compare these terms side by side. When looking at potential cards, you can check the "Rates and Fees" section to see if a penalty APR is listed. If the section says "None," the issuer cannot raise your rate as a punishment for late payments.

Navigating the Schumer Box

To find out if your current card has a penalty APR, you do not need to read a 40-page legal document. You only need to look at the Schumer Box. This is the standardized table required by law to appear in all credit card marketing and monthly statements.

In the Schumer Box, look for a row labeled "Penalty APR and When it Applies." This section will tell you exactly what the rate is and what triggers it. It will also specify how long the rate lasts. If you see a rate of 29.99% or similar, you know that the stakes for missing a payment are high.

If you are comparing new cards, the Schumer Box is the fastest way to see which cards are the most "forgiving" regarding mistakes. Some cards might have a penalty APR of 29.99%, while a competitor might have a penalty rate of only 24% or none at all.

If you want to compare cards that are generally easier to live with, MoneyAtlas’s cash back credit card rankings can help you see options that reward everyday spending without extra complexity. You can also read what APR is good for credit card purchases for a broader comparison framework.

Using MoneyAtlas to Compare Options

Choosing a credit card is more than just looking at the rewards or the sign-up bonus. The fine print, including penalty rates and fees, can have a much larger impact on your long-term financial health. We provide the tools to see these details clearly so you can make an informed decision.

If you are currently stuck with a penalty APR, use our comparison tools to search for balance transfer cards or cards for "fair credit" if your score has taken a hit. Comparing these options side by side allows you to see which cards offer the best chance of lowering your interest costs.

When you are ready to compare specific cards, the MoneyAtlas review of the Chase Freedom Unlimited® Credit Card is a good example of how we present product details, and the Discover it Cash Back review shows another popular no-annual-fee option.

Conclusion

A penalty APR is a powerful tool used by credit card issuers to manage risk, but it can be a devastating financial blow to an uninformed cardholder. By understanding that these rates are typically triggered by 60-day late payments and can reach nearly 30%, you can take the necessary steps to protect yourself. Autopay, budget tracking, and regular account monitoring are the most effective ways to keep your interest rates low.

If you find yourself facing a penalty rate, remember that it is not permanent. Six months of responsible behavior can restore your original rate and put you back on the path to financial stability.

Ready to find a card that fits your lifestyle without the hidden traps? Use the MoneyAtlas comparison tool to filter for cards with no penalty APRs and see how they stack up against your current wallet.

For readers who want a fresh start with simpler everyday rewards, browse the best cash back credit cards or look at our best credit cards comparison.

FAQ

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

Mastering Your Balance: How to Avoid Interest Charges on a Credit Card

Learn how to avoid interest charges on a credit card by mastering grace periods, paying your statement balance, and using 0% intro APR offers effectively.

Why 2 Interest Charges on Credit Card: Common Causes Explained

Wondering why 2 interest charges on credit card statements appear? Learn about residual interest and APR categories to manage your debt effectively.

Why Does a Credit Card Charge Interest?

Why does a credit card charge interest? Learn how banks calculate APR, how to use grace periods to avoid fees, and tips to minimize your daily interest costs.