What Credit Card Has Lowest APR: Top Options and How to Compare

Introduction

Finding the credit card with the lowest Annual Percentage Rate (APR) depends on whether someone needs a temporary 0% interest period or a long-term low interest rate. The APR represents the yearly cost of borrowing money, including interest and fees, expressed as a percentage. For a broader starting point, MoneyAtlas’s best credit cards comparison helps readers compare low rates, fees, and rewards side by side. This guide explores the current landscape of low interest cards, how credit scores influence the rates offered, and what to look for beyond the headline numbers.

Understanding the Two Types of Low APR

When searching for the lowest interest rates, it is helpful to distinguish between a promotional rate and a standard rate. Each serves a different purpose for the cardholder.

Introductory 0% APR Offers

Many major issuers offer a 0% intro APR on purchases, balance transfers, or both. These promotions typically last between 12 and 21 months. If you are focused on debt payoff, MoneyAtlas’s balance transfer card comparison is a useful place to start. However, once the promotional period ends, the APR will jump to the standard variable rate.

Low Ongoing Standard APR

For someone who occasionally carries a balance month to month, a low ongoing standard APR is often more valuable than a temporary 0% offer. While the average credit card APR in the US often exceeds 20%, some cards offer standard rates significantly lower. For a deeper look at how APR works in practice, read MoneyAtlas’s guide to what APR means on a credit card. MoneyAtlas tracks these variations to help users identify which institutions tend to offer lower ranges.

Top Options for Low Interest Credit Cards

The market for low APR cards is divided between large national issuers and member-based credit unions. The following categories represent the most common ways to secure a lower rate.

Credit Union Credit Cards

Credit unions are often the leaders in low ongoing interest rates. Because they are member-owned, they frequently pass savings back to members through lower loan rates and higher savings yields.

- Visa Platinum Cards: Many credit unions offer basic Platinum cards with no rewards but very low APRs.

- Membership Requirements: Most credit unions require a small deposit to a savings account to join.

National Bank 0% Intro Offers

For those prioritizing a 0% period, national banks offer some of the longest windows available.

- Long-Term Balance Transfers: Some cards offer 0% intro APR for up to 21 months on balance transfers. These are designed specifically for debt consolidation.

- Purchase and Reward Combinations: Many cash back cards offer 0% intro APR for 15 months while still allowing the cardholder to earn rewards.

For readers who want a rewards-focused option with no annual fee, MoneyAtlas’s cash back credit cards rankings can help narrow the choices. If low fees matter most, the no annual fee credit cards page is another smart comparison point.

Factors That Determine Your APR

The interest rate a person receives is not universal. It is usually presented as a range, and the specific rate assigned depends on several variables.

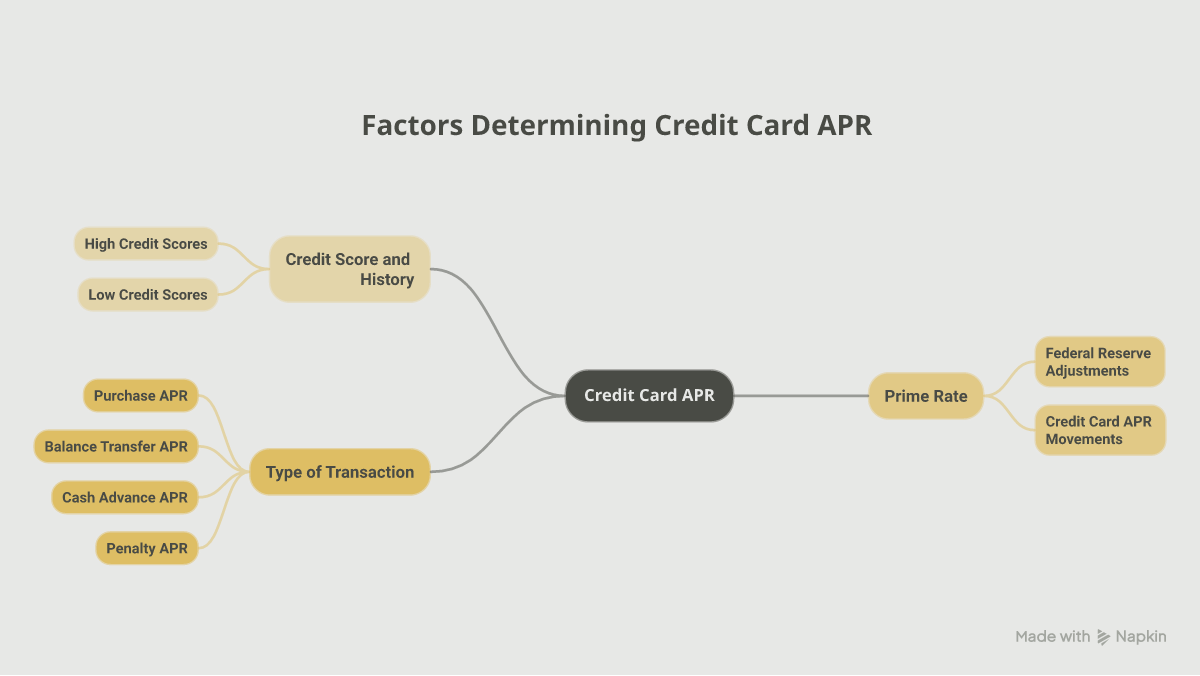

1. Credit Score and History

Issuers use credit scores to assess the risk of lending. Generally, the highest credit scores qualify for the lowest rates within a card's advertised range. For a closer look at how rates are priced, MoneyAtlas’s practical guide to APR calculation breaks down the math behind credit card interest.

2. The Prime Rate

Most credit cards have variable APRs. This means the rate is tied to an index, typically the US Prime Rate. When the Federal Reserve adjusts interest rates, the Prime Rate usually follows, causing credit card APRs to move up or down accordingly.

3. The Type of Transaction

A single credit card can have multiple APRs.

- Purchase APR: The rate applied to new items bought with the card.

- Balance Transfer APR: The rate for moving debt from another card.

- Cash Advance APR: A much higher rate, often 25% to 30%, applied when using the card to get cash. This interest usually starts accruing immediately.

- Penalty APR: A very high rate that may be triggered if a payment is late by 60 days or more.

How to Compare Low APR Cards

To find the right fit, it is necessary to look at the total cost of card ownership, not just the interest rate. MoneyAtlas’s credit card review index is a good next step when you want to compare specific cards in one place.

Evaluate the Annual Fee

A card with a 12% APR and a $95 annual fee might be more expensive than a card with a 15% APR and a $0 annual fee, depending on the average balance carried. For many shoppers, low-fee products are worth comparing alongside APR.

Check for Balance Transfer Fees

If the goal is to move existing debt to a 0% or low APR card, check for a balance transfer fee. This is usually 3% to 5% of the total amount transferred. On a $5,000 balance, a 5% fee adds $250 to the debt immediately. This must be weighed against the potential interest savings.

Review the Reward Trade-off

Often, the cards with the absolute lowest ongoing APRs do not offer rewards like cash back or travel points. It is important to decide if the interest savings outweigh the value of rewards. If you want an example of a no-fee rewards card, see the Blue Cash Everyday® Card from American Express review. For another everyday spending option, the Chase Freedom Unlimited® Credit Card review shows how a card can pair simple rewards with a 0% intro period.

Steps to Secure a Lower Interest Rate

Securing a low rate is a process of both selection and maintenance.

How to Secure a Lower Interest Rate

- 1

Check your credit score

Knowing your score helps narrow down which cards are likely to approve an application. Most low APR cards require good to excellent credit.

- 2

Research credit unions

Look for local or national credit unions with open membership. Compare their Platinum or non-rewards cards against national bank offers.

- 3

Calculate the break-even point

If a card has a 0% intro period but a high standard rate later, calculate if the balance can be paid off before the promo ends.

- 4

Use a comparison tool

MoneyAtlas allows users to filter by APR range and intro offer length to see how different cards stack up.

If you are still deciding between intro offers and ongoing rewards, the Capital One Venture Rewards Credit Card review is a helpful example of a travel card with a different value tradeoff. If you want a simpler entry-level option, the Capital One VentureOne Rewards Credit Card review shows how a no annual fee card can fit a lighter spending pattern.

FAQ

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

Do Credit Cards Charge Interest if You Pay in Full?

Do credit card charge interest if you pay in full? Learn how grace periods work and how to avoid interest by paying your statement balance by the due date.

Why Is Interest Charged on My Credit Card? Understanding the Mechanics

Wondering why is interest charged on my credit card? Learn how APR works, how interest is calculated daily, and tips to avoid fees. Take control of your debt today!

When Does Interest Charge on Credit Card?

Wondering when does interest charge on credit card accounts? Learn how billing cycles and grace periods work to avoid high APR costs and debt.