Is Credit Card APR the Same as Interest Rate?

Introduction

When you review a credit card agreement or look at your monthly statement, the term Annual Percentage Rate (APR) appears alongside the term interest rate. Many people wonder if these two figures represent different costs or if they are simply different names for the same thing. For credit cards, the interest rate and the APR are almost always the same. This differs from other financial products, such as mortgages or auto loans, where the APR is typically higher than the interest rate.

MoneyAtlas tracks these rates across hundreds of cards to help you understand the real cost of borrowing. If you want a broader starting point, begin with our best credit cards comparison to see how rates, fees, and rewards stack up. This article explains why these terms are used interchangeably for credit cards, how the math affects your monthly balance, and why the distinction matters when you compare other types of loans. Understanding these nuances helps you navigate the fine print and choose the right financial products for your needs.

The Core Difference Between APR and Interest Rate

To understand why these terms overlap, it helps to define what each one represents in the broader financial world. The interest rate is the base cost you pay to borrow the principal amount of a loan. It is expressed as a percentage. APR is a broader measure. It is designed to show the total annual cost of borrowing by including the interest rate plus any mandatory fees or closing costs.

For a plain-English breakdown of the mechanics, see MoneyAtlas’s guide on what APR means in credit card accounts. With a mortgage, for example, the APR includes the interest rate plus loan origination fees, mortgage insurance, and discount points. This is why a mortgage might have a 6% interest rate but a 6.2% APR. The higher APR gives you a more accurate picture of the total cost of the loan over time.

Credit cards are the exception to this rule. Under the Truth in Lending Act, credit card issuers must disclose their rates clearly, but they do not include most fees in the APR calculation. This is because fees like annual fees, late fees, or foreign transaction fees are not charged to everyone. Since an issuer cannot predict which cardholders will trigger these fees, they are kept separate from the APR.

Comparison: APR vs. Interest Rate by Product Type

Why Credit Card APR and Interest Rate Match

The primary reason credit card APRs and interest rates are identical is the nature of revolving credit. Unlike an installment loan with a set end date and a fixed amount of fees, a credit card is a flexible line of credit. You might use it every day, or you might not use it for months. You might pay an annual fee once a year, or you might have a card with no annual fee at all.

If you are comparing cards with and without yearly fees, our no annual fee credit cards comparison can help you size up the tradeoffs. Because these costs are situational, federal regulations do not require issuers to bake them into the APR. Instead, these details are listed in the Schumer Box. This is the standardized table required on all credit card applications. It breaks down the interest rate for purchases, the rate for cash advances, and the specific dollar amounts for various fees. MoneyAtlas makes it easier to compare these Schumer Box details side by side so you can see which cards have the lowest overall cost.

How Credit Card Interest Is Actually Charged

Even though the APR is expressed as an annual figure, credit card companies do not wait until the end of the year to charge you. They calculate interest much more frequently. Understanding this mechanic is vital for anyone who carries a balance month to month.

The Daily Periodic Rate

Most credit card issuers calculate interest daily. To do this, they take your APR and divide it by 365 days. The result is called the daily periodic rate. If you have a card with a 24% APR, your daily periodic rate is approximately 0.0657%.

Every day that you carry a balance, the issuer applies this daily rate to your average daily balance. This means you are not just paying interest on what you spent. You are also paying interest on the interest that was added to your account the day before. This process is called compounding.

Compounding Interest Mechanics

Compounding can make debt grow faster than many people expect. Because the interest is added to your balance daily, your balance increases slightly every 24 hours. The next day, the interest rate is applied to that new, higher balance. Over a 30 day billing cycle, this can add up to a significant amount.

For a deeper look at promotional offers, see how 0% APR works on credit cards. Even if two cards have the same 22% APR, the one that compounds daily will be slightly more expensive than one that compounds monthly. Almost all major US cards use daily compounding.

Step-by-Step: Calculating Your Monthly Interest

If you want to see exactly how much your balance is costing you, follow these steps.

How to Calculate Your Monthly Interest

- 1

Find your APR.

Look at your most recent statement for the purchase APR.

- 2

Calculate the daily rate.

Divide the APR by 365. For a 20% APR, the math is 0.20 / 365 = 0.000547.

- 3

Determine your average daily balance.

Add up your balance for each day of the billing cycle and divide by the number of days.

- 4

Multiply the daily rate by the balance.

Multiply 0.000547 by your average balance.

- 5

Multiply by the number of days.

Take that daily cost and multiply it by the number of days in your billing cycle (usually 28 to 31).

For someone carrying a $5,000 balance at a 20% APR, the monthly interest charge would be roughly $82. This is money that does not go toward paying down your actual debt.

Different Types of APR on a Single Card

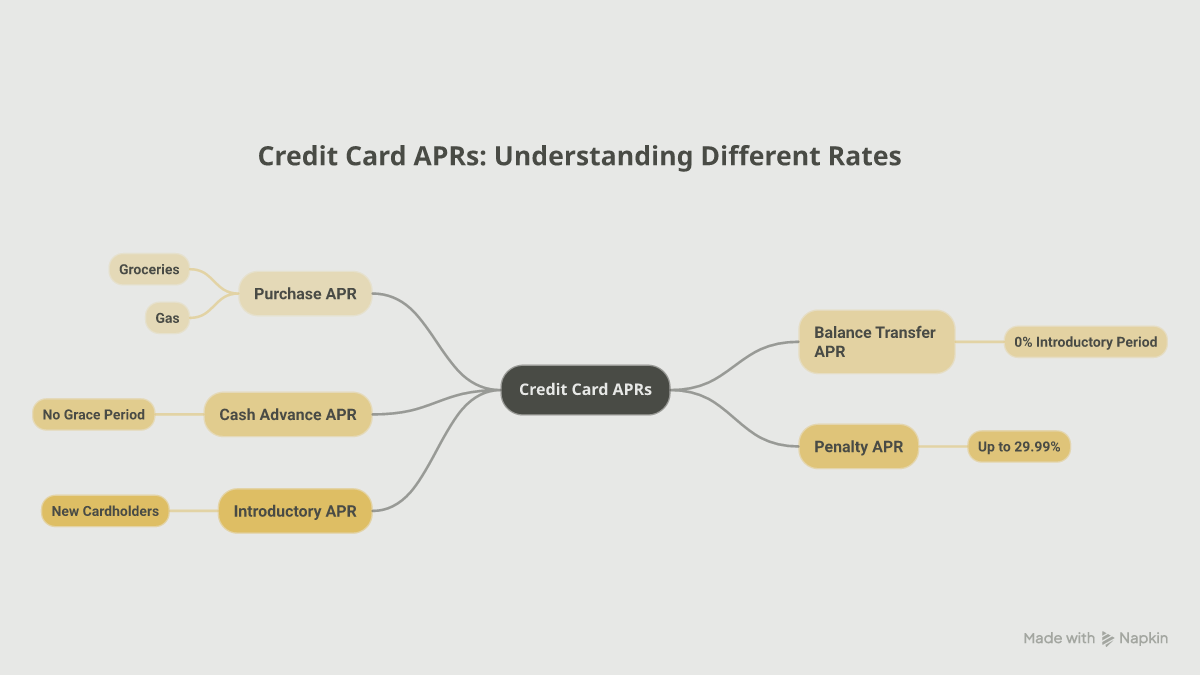

It is a common mistake to assume a card has only one interest rate. In reality, most credit cards have several different APRs that apply depending on how you use the card. These are all listed in your cardholder agreement.

Purchase APR

This is the standard rate applied to things you buy, like groceries, gas, or online shopping. This is the rate most people refer to when they talk about a card's interest rate.

Balance Transfer APR

When you move debt from one card to another, the new card might offer a special rate. If you are comparing options side by side, start with our balance transfer credit cards comparison. Many cards offer a 0% introductory APR on balance transfers for 12 to 21 months. After that period ends, the balance transfer APR usually reverts to the standard purchase APR.

Cash Advance APR

If you use your credit card at an ATM to get cash, you will likely be charged a cash advance APR. This rate is almost always significantly higher than the purchase APR. Furthermore, cash advances usually do not have a grace period. Interest starts accruing the moment the cash is in your hand.

Penalty APR

If you miss a payment or pay late, the issuer may raise your interest rate to a penalty APR. This rate can be as high as 29.99%. It can remain in effect indefinitely or until you make several consecutive on-time payments.

Introductory APR

Many cards offer a 0% rate for a limited time to attract new customers. This can apply to purchases, balance transfers, or both. It is an excellent way to avoid interest while paying down a large purchase, provided the balance is cleared before the promotional period ends.

The Role of the Grace Period

The best way to handle credit card interest is to avoid it entirely. Most credit cards offer a grace period of at least 21 days between the end of your billing cycle and your payment due date. If you pay your statement balance in full by the due date every month, the issuer will not charge you any interest on your purchases.

In this scenario, the APR effectively becomes 0% for you. This is why many people who pay their bills in full every month do not prioritize the interest rate when choosing a card. Instead, they focus on rewards or travel perks. However, if there is a chance you might carry a balance, comparing APRs becomes the most important part of the decision.

Factors That Determine Your APR

Not everyone gets the same interest rate, even for the same card. When you apply for a card, the issuer looks at several factors to determine your creditworthiness.

- Credit Score: Generally, people with higher credit scores (740+) qualify for the lowest available APRs. Those with lower scores are considered higher risk and are offered higher rates.

- Income and Debt: Issuers look at your debt-to-income ratio to ensure you can afford the monthly payments.

- The Prime Rate: Most credit cards have a variable APR. This means the rate is tied to an index called the Prime Rate. When the Federal Reserve raises or lowers interest rates, your credit card APR will likely change as well.

If you are rebuilding credit, you may want to compare products in the credit card reviews index and look for cards that match your profile. MoneyAtlas provides reviews of cards for every credit tier. Whether you have excellent credit and want the lowest possible rate or you are rebuilding your credit with a secured card, you can compare options to see what rates are typical for your situation.

Fixed vs. Variable APRs

Most credit cards issued today use a variable APR. This means your interest rate can change over time without the issuer needing to ask your permission. Variable rates are usually calculated by taking the Prime Rate and adding a certain percentage, known as the margin. For example, if the Prime Rate is 8.5% and your card's margin is 12%, your APR is 20.5%.

Fixed APRs are rare in the modern credit card market. Even with a fixed rate, an issuer can still change it, but they must give you 45 days of advance notice. Because the Prime Rate fluctuates based on the economy, variable rates are the industry standard.

Is a High APR Always a Bad Thing?

A high APR is only a problem if you carry a balance. Many of the best rewards cards, including those that offer high cash back percentages or premium travel points, come with higher than average APRs. The banks use the interest income from those who carry balances to fund the rewards for those who pay in full.

If you want to compare rewards-focused options, check our cash back credit cards comparison. For example, Chase Freedom Unlimited® and Capital One Quicksilver Cash Rewards Credit Card are common everyday-spend cards to review side by side. If you know you will pay your bill every month, a 25% APR does not cost you anything. In that case, you can ignore the APR and focus on the rewards. However, if you are planning a large purchase that you need to pay off over six months, a high APR card could cost you hundreds of dollars. For that situation, a low interest card or a 0% introductory offer is a much better choice.

How to Compare Credit Card Offers

When you are ready to find a new card, don't just look at the flashy bonus offer. Dig into the rates and terms to ensure the card fits your spending habits.

- Check the APR range. Most cards list a range, such as 19% to 29%. Assume you will get a rate in the middle or high end unless your credit score is exceptional.

- Look for 0% intro periods. If you have existing debt, a 0% balance transfer offer can save you a significant amount of money.

- Watch for annual fees. A card with a lower interest rate but a high annual fee might be more expensive than a card with a slightly higher rate and no fee.

- Verify the cash advance rate. If you think you might ever need to withdraw cash, check this rate first, as it is often much higher than the purchase rate.

If you prefer a travel-style starter card with no yearly fee, you can also review the Capital One VentureOne Rewards Credit Card. MoneyAtlas makes it easier to compare these factors side by side. By looking at the expert ratings and the detailed fee breakdowns, you can find a card that matches your financial goals without being surprised by the fine print later.

When APR Matters Most

While the distinction between APR and interest rate is negligible for credit cards, understanding the APR is critical when you move into other types of borrowing. If you are considering a personal loan to consolidate credit card debt, you must look at the APR. Many personal loans charge an origination fee, which is a percentage of the loan amount taken off the top.

A personal loan might advertise a 10% interest rate, but if it has a 5% origination fee, the APR will be significantly higher. When you use the comparison tools on MoneyAtlas, you can see these fees clearly. This allows you to compare a personal loan's APR against your credit card's APR to see if consolidation actually saves you money.

Strategies for Managing High APR Debt

If you currently have a credit card with a high interest rate and a large balance, you are likely losing a lot of money to compounding interest every month. You can take steps to mitigate these costs.

- Request a rate reduction. If your credit score has improved since you opened the card, call the issuer and ask for a lower APR. They may agree to lower it to keep you as a customer.

- Focus on the highest rate first. Use the avalanche method by making the minimum payments on all cards and putting every extra dollar toward the card with the highest APR.

- Use a balance transfer. Moving a 25% APR balance to a 0% intro APR card can stop interest charges for a year or more. This allows every dollar of your payment to go toward the principal balance.

- Consider a personal loan. If you cannot qualify for a 0% balance transfer card, a personal loan with a fixed term and a lower APR can provide a structured way to pay off the debt.

If the card you carry is tied to a simple rewards structure, you can review a spend-category fit like Capital One Savor Cash Rewards Credit Card to see whether the perks outweigh the cost.

Summary of Key Differences

While we have established that credit card interest rates and APRs are generally the same, the most important takeaway is that the APR is your most reliable tool for comparison. It is the standardized "price tag" for borrowing money. Whether you are looking at a credit card or a mortgage, the APR is designed to prevent lenders from hiding the true cost of a loan in the fine print.

For a closer look at what influences those rates, read is 13 or 18 APR for a credit card better. MoneyAtlas is built to bring this transparency to your financial decisions. By comparing over 1,500 products, we help you see past the marketing and focus on the numbers that affect your bank account.

FAQ

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

Do Credit Cards Charge Interest if You Pay in Full?

Do credit card charge interest if you pay in full? Learn how grace periods work and how to avoid interest by paying your statement balance by the due date.

Why Is Interest Charged on My Credit Card? Understanding the Mechanics

Wondering why is interest charged on my credit card? Learn how APR works, how interest is calculated daily, and tips to avoid fees. Take control of your debt today!

When Does Interest Charge on Credit Card?

Wondering when does interest charge on credit card accounts? Learn how billing cycles and grace periods work to avoid high APR costs and debt.