What Is Normal Credit Card APR? A Guide to Average Interest Rates

Introduction

Finding out if a credit card interest rate is fair requires looking at current market averages and individual credit profiles. The question of what is normal credit card APR is common for anyone opening a new account or managing existing debt. Most cardholders want to know if they are paying more than necessary or if they qualify for a better deal. Currently, the average interest rate for new credit card offers sits near 23.79%, though this figure varies significantly based on the type of card and the applicant's credit score.

MoneyAtlas tracks these shifts to help consumers evaluate their current financial products. If you are ready to compare current offers, start with our best credit cards comparison. This guide covers the current benchmarks for different card categories, how issuers determine individual rates, and the mechanics of interest charges. Understanding these averages allows for more effective comparisons when choosing a new financial product.

Current Benchmarks for Credit Card APR

To determine if a rate is normal, it is necessary to look at the broader economic environment. Credit card interest rates are largely influenced by the federal funds rate, which is the interest rate banks charge each other for overnight loans. When the Federal Reserve adjusts this rate, credit card APRs typically follow suit within one or two billing cycles.

Annual Percentage Rate, or APR, represents the yearly cost of borrowing money on a card balance. It includes the interest rate and certain fees expressed as a percentage. While many people use the terms interest rate and APR interchangeably in the credit card world, the APR is the standardized figure used for comparison.

Averages for New Credit Card Offers

Data from recent market analysis shows that the average APR for new credit card offers is 23.79%. For a deeper look at how that compares to today’s borrowing environment, see what qualifies as high APR on credit cards. This figure represents a baseline for someone with a solid credit profile applying for a standard card. However, this is an average of many different products. Some cards designed for low interest might offer rates significantly lower, while rewards cards often sit at the higher end of the spectrum.

Averages for Existing Accounts

There is often a difference between the rates offered to new customers and the rates currently being paid on existing accounts. If you want the broader definition of the rate on your statement, MoneyAtlas also explains what regular APR means for credit cards. According to Federal Reserve data, the average APR on all credit card accounts assessed interest is approximately 21.52%. This includes older accounts that may have been opened when the prime rate was lower. For cardholders who pay their balance in full every month, the APR is less impactful because interest does not accrue during the grace period.

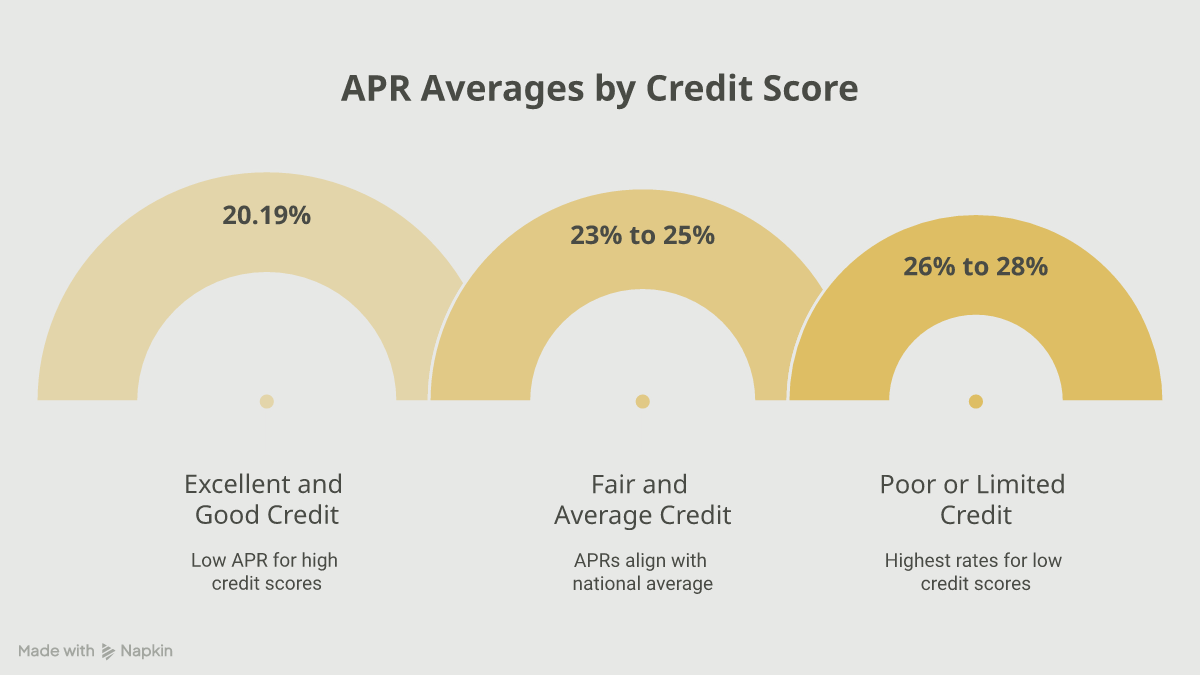

APR Averages by Credit Score

An individual's credit score is the most significant factor in determining the specific APR an issuer offers. Lenders use credit scores to assess the risk of nonpayment. Higher scores suggest lower risk, which typically results in a lower interest rate.

Excellent and Good Credit (700 to 850)

For applicants with credit scores in the 700s or 800s, a normal APR is usually at the lower end of the issuer's provided range. Recent data shows that borrowers with excellent credit receive average offers around 20.19%. These individuals are often eligible for the most competitive rewards cards and long 0% introductory periods.

Fair and Average Credit (640 to 699)

Cardholders in the fair credit range often see APRs that align closely with the national average of 23% to 25%. While they may still qualify for rewards cards, they are less likely to receive the lowest advertised rate in a given range.

Poor or Limited Credit (300 to 639)

Borrowers with lower credit scores or those who are new to credit altogether face the highest rates. For this group, a normal APR often falls between 26% and 28%. If you are rebuilding and want a simpler starting point, our no annual fee credit card comparison can help you compare lower-cost options. Secured credit cards, which require a cash deposit, also carry high APRs, frequently averaging 26.09% or more.

Normal APR by Credit Card Category

The purpose of a credit card often dictates its interest rate. A card designed for luxury travel perks will almost always have a higher APR than a card designed specifically for debt consolidation.

Rewards and Cash Back Cards

Cards that offer points, miles, or cash back generally have higher APRs. If travel rewards matter most, browse our travel credit cards comparison. The average for cash back cards is currently around 23.82%, while travel rewards cards average 23.71%. The cost of funding the rewards programs is often reflected in the higher interest rates charged to those who carry a balance.

Low Interest and Balance Transfer Cards

For someone looking to minimize interest costs, low interest cards are the standard choice. If you want to compare options built for debt payoff, start with our balance transfer card comparison. These products currently average about 17.31%. Balance transfer cards, which often feature a 0% introductory period, typically have a standard purchase APR of 22.19% after the promotion expires.

Student and Secured Cards

Student credit cards are designed for those with little credit history and currently average 22.29%. Secured cards, often used for credit rebuilding, have the highest averages at 26.09%. Because these cards are for higher risk borrowers, the high APR serves as a safeguard for the lender.

How Credit Card APR Is Determined

Understanding why a rate is considered normal requires a look at the formula used by banks. Most credit cards use variable APRs, which means the rate can change without notice when a specific benchmark moves.

The Prime Rate

The foundation of most credit card rates is the U.S. Prime Rate. This is the interest rate that commercial banks charge their most creditworthy corporate customers. It is typically 3% higher than the federal funds rate set by the Federal Reserve. If the Prime Rate is 8.5%, an issuer will use that as the starting point.

The Issuer Margin

On top of the Prime Rate, the credit card issuer adds a margin based on the cardholder's credit risk and the card's features. For example, a card might have a rate of Prime + 15%. If the Prime Rate is 8.5%, the total APR would be 23.5%. This margin covers the issuer's operating costs, the cost of rewards, and the risk that some borrowers might not pay their bills.

Fixed vs. Variable Rates

While most cards are variable, some rare cards offer fixed rates. A fixed rate APR does not automatically change when the Prime Rate moves. However, the issuer can still change a fixed rate by providing 45 days of notice to the cardholder. Variable rates are much more common because they allow lenders to maintain their profit margins automatically as economic conditions shift.

Different Types of APR on One Card

A single credit card account often has several different APRs depending on the transaction type. It is a mistake to assume that the purchase APR applies to everything.

Purchase APR

This is the most common rate. It applies to standard purchases of goods and services. If you pay your balance in full by the due date, you generally avoid paying this interest entirely due to the grace period.

Balance Transfer APR

When moving debt from one card to another, a specific balance transfer APR applies. While many cards offer 0% introductory periods for 12 to 21 months, the standard rate that kicks in afterward might be different from your purchase APR.

Cash Advance APR

Using a credit card to get cash from an ATM is one of the most expensive ways to use the card. Cash advance APRs are often 5% to 10% higher than purchase APRs. Additionally, cash advances usually have no grace period, meaning interest starts accruing immediately.

Penalty APR

If a cardholder misses a payment by 60 days or more, the issuer may apply a penalty APR. This rate can be as high as 29.99%. It can remain on the account indefinitely, though issuers are required to review the account after six months of on-time payments to see if the rate can be lowered.

How to Calculate Monthly Interest Charges

Knowing your APR is the first step in understanding the real cost of your debt. Credit card interest is usually compounded daily, which means the issuer calculates interest every day based on your average daily balance.

For a plain-English walkthrough of the math, MoneyAtlas has a practical guide to how APR is calculated for credit cards.

Step 1: Find the Daily Periodic Rate

To find the daily rate, divide your APR by 365. For a card with a 24% APR, the calculation is 24% / 365. This equals a daily periodic rate of approximately 0.0657%.

Step 2: Determine Your Average Daily Balance

The issuer looks at your balance every day of the billing cycle. If you started with $1,000 and made no payments or purchases, your average daily balance is $1,000. If your balance changed throughout the month, they add the daily totals and divide by the number of days in the cycle.

Step 3: Multiply the Figures

Multiply your average daily balance by the daily periodic rate. Then, multiply that result by the number of days in your billing cycle. For a $1,000 balance at 24% APR in a 30 day month:

$1,000 x 0.000657 x 30 = $19.71.

This $19.71 is the interest charge that would appear on your statement for that month. While it may seem small, these charges compound over time, making it harder to pay down the principal balance.

Strategies for Getting a Lower APR

If your current rate is significantly higher than the normal averages discussed, you have several options to reduce your interest costs. Comparing your current rate against the latest market data is the first step in this process.

If you want a broader next step, our guide to lowering credit card APR breaks down the main strategies.

Improve Your Credit Score

Since APR is tied to creditworthiness, raising your score is the most effective long-term strategy. This involves:

- Paying every bill on time, every month.

- Keeping credit utilization below 30% of your total limits.

- Limiting new credit applications to avoid hard inquiries.

Negotiate with Your Issuer

Cardholders with a history of on-time payments can sometimes successfully ask for a lower rate. Call the customer service number on the back of your card. Mention how long you have been a customer and note that you have seen lower rates offered elsewhere. While not guaranteed, issuers sometimes lower the APR to keep a loyal customer from switching to a competitor.

Use a Balance Transfer Card

For those carrying significant debt, moving the balance to a card with a 0% introductory APR can save hundreds of dollars. These promotions often last for 12 to 18 months. It is important to compare the balance transfer fee, which is usually 3% to 5% of the transferred amount, against the interest savings to ensure the move makes financial sense.

Look at Credit Unions

Federal credit unions are subject to a legal interest rate cap of 18% on most loans, including credit cards. This is significantly lower than the current national average for bank issued cards. For many consumers, a credit union card represents the most reliable way to secure a "normal" rate that stays below the 20% mark.

The Role of the Grace Period

One of the most important features of a credit card is the grace period. This is the window between the end of a billing cycle and your payment due date. Most cards offer a grace period of at least 21 days.

If you pay your statement balance in full by the due date, the issuer does not charge interest on your purchases. In this scenario, the APR is effectively 0%. However, if you carry even a small balance into the next month, the grace period disappears. This is known as "trailing interest" or "residual interest." Once the grace period is lost, interest begins accruing on new purchases the moment you make them.

To regain the grace period, most issuers require you to pay the balance in full for two consecutive billing cycles. This highlights why paying the full balance is the most effective way to manage a credit card, regardless of whether the APR is 15% or 25%.

Important Terms to Watch For

When comparing credit card offers, the fine print contains several terms that affect the total cost of credit. Being a "knowledgeable friend who reads the fine print" means paying attention to these details.

Annual Fee: Some cards charge a flat yearly fee. When calculating the true cost of a card, this fee should be factored in alongside the APR. A card with a 15% APR and a $95 annual fee might be more expensive than a card with a 20% APR and no fee, depending on your average balance.

Variable Rate Floor: Most variable rate cards have a minimum APR that they will not drop below, even if the Prime Rate falls significantly. This floor is often listed in the terms and conditions.

Introductory Period Terms: Always check if the 0% rate applies to both purchases and balance transfers. Some cards only offer the promotional rate on one or the other. Also, verify what the "go-to" APR will be once the promotion ends.

Late Fee and Penalty Trigger: Understand exactly when a late payment triggers a penalty APR. Under the CARD Act, issuers generally cannot raise your rate on existing balances unless you are 60 days late. However, they can raise the rate on new purchases with 45 days of notice.

When a High APR Is Worth It

There are specific situations where a cardholder might choose a card with a higher than normal APR. This is usually the case for people who never carry a balance.

For someone who pays in full every month, the APR is irrelevant. In this case, it makes sense to prioritize a card with the best rewards, travel insurance, or airport lounge access, even if the APR is 28%. These "premium" cards often have the highest interest rates because the issuers use that revenue to fund the high end perks.

Conversely, if there is any chance you will carry a balance, a high rewards card is usually a poor choice. The interest charges will quickly outweigh the value of any points or cash back earned. For those who carry debt, a "plain vanilla" card with a low APR is the better tool.

Next Steps for Comparing Rates

If your current credit card has an APR above 24% and you have a good credit score, you are likely paying more than the current market average. Taking action to lower this cost can significantly improve your monthly cash flow.

How to Compare Credit Card APRs

- 1

Check statement APR

Check your current statement to find your actual APR.

- 2

Get your score

Use a credit monitoring tool to get your current credit score.

- 3

Compare category averages

Compare your current rate against the category averages for rewards, low interest, or balance transfer cards.

- 4

Review tailored offers

Use a comparison platform to see specific offers tailored to your credit range.

MoneyAtlas provides side by side comparisons of over 1,500 products to make this process easier. If you are deciding between payoff strategies and long term rewards, compare credit cards by type to see which direction fits your goals. By looking at the expert ratings and honest fee breakdowns, you can determine if a different card would better serve your current financial situation.

FAQ

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

How Much Will My Credit Card Interest Charges Be?

Wondering how much will my credit card interest charges be? Learn how to calculate your daily rate and minimize monthly fees with our expert guide.

How Much Do Credit Cards Charge Interest? Understanding the Real Cost

Wondering how much do credit cards charge interest? Learn how APR is calculated, why rates vary, and how to avoid costly charges with our expert guide.

How Much Interest Will My Credit Card Charge Me?

Wondering how much interest will my credit card charge me? Learn to calculate your daily rate, use the grace period, and minimize interest costs today.