Is 24% APR High for a Credit Card? Costs and Comparisons

Introduction

Determining if a 24% Annual Percentage Rate (APR) is high for a credit card depends on your credit score, the type of card you use, and current market conditions. In the current lending environment, a 24% APR is roughly average for many rewards cards and retail accounts. However, it is significantly higher than the rates found on low-interest cards or those offered by credit unions, which often cap rates at 18%. MoneyAtlas monitors these trends to help you understand how your specific rate stacks up against the broader market. This post explores the mechanics of high-interest rates, how they impact your monthly balance, and the steps to take if you want to lower your borrowing costs. Understanding these factors is the first step toward comparing your credit card options and making a more informed financial decision.

Understanding the Credit Card APR Landscape

The APR on a credit card is the yearly interest rate you pay to borrow money. While it is expressed as an annual figure, credit card companies actually use it to calculate interest on a daily basis. To determine if 24% is high, you must first look at the national averages.

In recent years, the average credit card APR has climbed significantly. Many major banks now offer standard rates between 21% and 25% for cardholders with good credit. If you are using a card that offers travel points or cash back, a 24% APR is very common. These cards often have higher interest rates to help the issuer offset the cost of the rewards they provide.

However, if you look at the broader financial landscape, 24% is expensive compared to other forms of debt. For example, personal loans often carry rates in the 8% to 15% range for qualified borrowers. Mortgages and auto loans are even lower. In the world of credit cards specifically, a rate is usually considered high if it significantly exceeds the national average for your specific credit tier.

The Impact of the Prime Rate

Most credit cards have variable interest rates. This means your APR is not fixed. It is instead tied to an index called the Prime Rate. The Prime Rate is influenced by the Federal Reserve's decisions regarding the federal funds rate.

When the Federal Reserve increases rates to combat inflation, the Prime Rate goes up. Because most credit card agreements are structured as the Prime Rate plus a specific percentage margin, your 24% APR could easily climb to 25% or 26% without the issuer needing to provide much notice. This variable nature makes it difficult to predict exactly how much interest you will owe from one year to the next.

How 24% APR Affects Your Monthly Balance

A 24% APR can quickly turn a small balance into a large debt due to daily compounding. Credit card companies calculate your interest every single day. They do this by dividing your APR by 365 to find the daily periodic rate.

For a 24% APR, the daily rate is approximately 0.0657%. This may seem like a tiny number, but it is applied to your average daily balance every day of your billing cycle. If you carry a $5,000 balance, you are accruing about $3.29 in interest daily. Over a 30 day month, that adds up to nearly $100 in interest alone.

The real danger of a 24% APR is how it interacts with minimum payments. Most minimum payment requirements are set at roughly 1% to 2% of your balance plus the interest charged that month. If your interest is $100 and your minimum payment is $150, only $50 is actually going toward the principal balance. This can lead to a cycle where you are paying for years without making significant progress on the original debt.

Comparison of Interest Costs

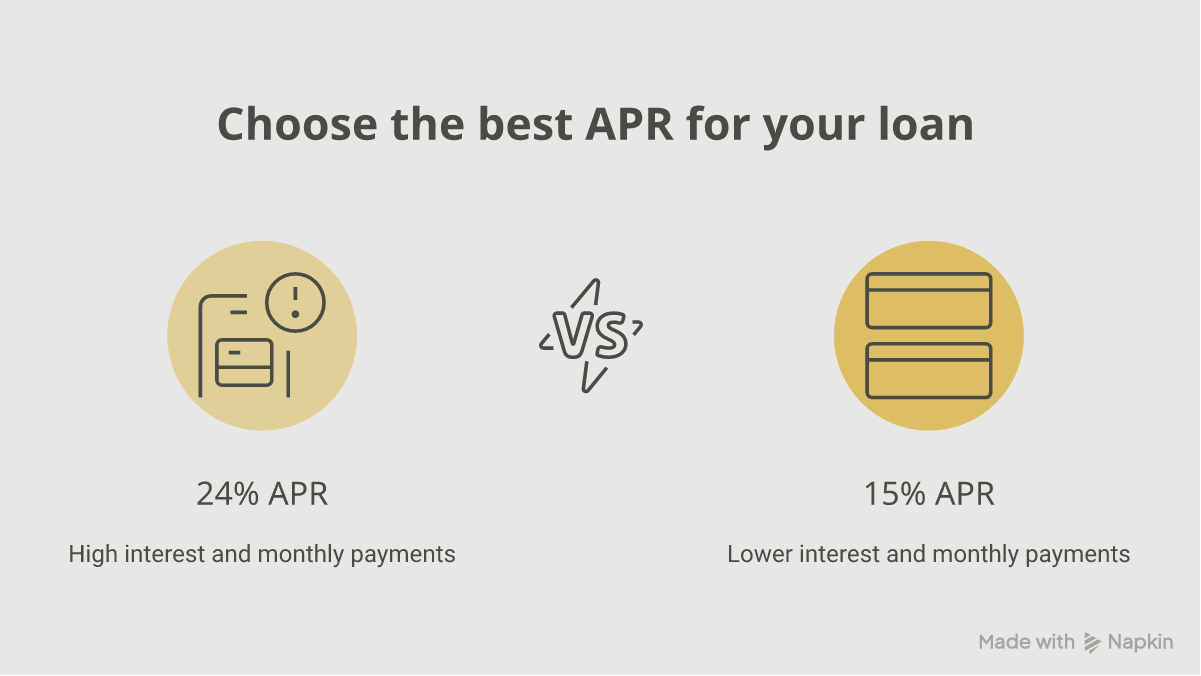

To see how a 24% APR compares to a lower rate, consider a $3,000 balance that you plan to pay off over 24 months.

- At 24% APR: You would pay approximately $172 per month. Your total interest paid over two years would be about $820.

- At 15% APR: You would pay approximately $159 per month. Your total interest paid over two years would be about $490.

- At 0% APR: You would pay $125 per month. Your total interest paid would be $0.

As this comparison shows, the difference between a high rate and a competitive rate can mean hundreds of dollars in extra costs for the same purchase.

Why Your Rate Might Be 24% or Higher

Lenders use risk-based pricing to determine your APR. This means they look at the likelihood that you will pay back the money you borrow. Several factors influence where you land on the APR spectrum.

Your Credit Score

Your credit score is the most significant factor in your assigned APR. Cardholders with excellent credit scores (740 or higher) are often offered the lowest possible rates in a card's advertised range. If a card advertises an APR between 19% and 29%, a high credit score helps you secure that 19% rate.

If your score is in the fair or poor range (below 670), you are viewed as a higher risk. Lenders charge higher interest rates to compensate for that risk. For someone with a lower score, a 24% APR might actually be the best offer available to them.

The Type of Credit Card

Not all credit cards serve the same purpose. The card's features often dictate the interest rate. If you want to browse a broader set of cash back credit cards, compare how rewards can affect the long-term value of the card.

- Rewards Cards: These cards offer cash back, miles, or points. They almost always have higher APRs, often starting at 20% or higher.

- Retail or Store Cards: Cards co-branded with specific retailers often have some of the highest rates in the industry. It is common to see store card APRs between 28% and 32%. In this context, 24% might actually look relatively low.

- Low-Interest Cards: These cards usually do not offer rewards. Instead, they provide a lower ongoing APR for people who know they might need to carry a balance occasionally. These rates can sometimes be as low as 12% to 15%.

- Secured Cards: These are for people building credit. Because they require a cash deposit, the risk to the lender is lower, but the APRs can still be high, often 24% to 26%, because the borrower's credit history is unproven.

Penalty APRs

If you miss a payment or pay more than 60 days late, your issuer might trigger a penalty APR. This rate is often the maximum allowed by the card agreement, frequently reaching 29.99%. If your rate was 24% and it jumps to nearly 30%, your interest costs increase by 25% almost overnight.

When a 24% APR Becomes a Problem

A 24% APR is only a problem if you carry a balance from month to month. If you pay your statement in full every single month, the APR is effectively 0%. This is because most credit cards offer a grace period.

The grace period is the time between the end of your billing cycle and your payment due date. If you pay the full balance during this window, the issuer does not charge interest on your purchases. For people who treat their credit card like a debit card and pay it off frequently, a 24% APR is an irrelevant number.

The 24% APR becomes a serious financial burden in several specific scenarios:

- Emergency Expenses: If you use your card for a $2,000 car repair and cannot pay it off for six months, that 24% rate will add significant cost to the repair.

- Income Instability: If you rely on credit for daily living expenses during a period of unemployment, the high interest rate will make it much harder to recover once you find a new job.

- Living Beyond Your Means: Charging more than you can afford to pay off results in interest charges that compound, making your future purchases even more expensive.

How to Lower Your Interest Rate

If you realize your 24% APR is costing you too much money, you have several ways to lower that cost. You do not always have to accept the rate you were originally given.

Negotiate with Your Issuer

Many cardholders do not realize they can simply call their credit card company and ask for a lower rate. This is especially effective if your credit score has improved since you first opened the account.

When you call, mention how long you have been a customer and point out your history of on-time payments. If you have received offers from other cards with lower rates, mention those as well. While the issuer is not required to lower your rate, they may offer a temporary reduction or a permanent move to a lower APR tier to keep you as a customer. For more context, see how to request a lower APR on a credit card.

Use a Balance Transfer Card

A balance transfer card allows you to move debt from a high-interest card to a new card with a 0% introductory APR. These introductory periods typically last between 12 and 21 months.

By moving a balance from a 24% card to a 0% card, every dollar of your payment goes toward the principal. This can save you hundreds or even thousands of dollars in interest. However, be aware that most cards charge a balance transfer fee, usually between 3% and 5% of the total amount moved. You must also ensure you pay off the balance before the introductory period ends, or the rate will jump to a standard APR, which could be 24% or higher. You can compare current offers with our balance transfer card comparison.

Explore Credit Unions

Federal credit unions are unique because they are member owned and subject to different regulations than national banks. The National Credit Union Administration currently caps interest rates on most loans and credit cards at federal credit unions at 18%.

If you have a 24% APR at a big bank, moving that balance to a credit union card could immediately drop your rate by 6%. Credit unions also often have fewer fees and more personalized customer service. MoneyAtlas makes it easier to compare credit union offerings alongside national bank cards to see where the best value lies.

Consolidation with a Personal Loan

If you have a large amount of credit card debt at 24% APR, a personal loan might be a better tool for repayment. Personal loans have fixed interest rates and fixed monthly payments.

For someone with good credit, a personal loan rate might be 10% to 15%. Using that loan to pay off your 24% credit cards simplifies your debt into a single payment and significantly reduces the total interest you pay. This is a common strategy for people who want a clear end date for their debt. You can also compare personal loans to see whether a fixed installment plan fits your payoff timeline.

Strategies for Managing High APR Debt

If you are currently managing a balance on a card with 24% APR, how you structure your payments matters. Using a systematic approach can help you minimize the damage.

The Debt Avalanche Method

The debt avalanche method involves listing all your debts and their interest rates. You then direct as much money as possible toward the debt with the highest APR while making minimum payments on the others.

Since 24% is likely one of your higher rates, focusing on this balance first will save you the most money over time. Once the 24% card is paid off, you move all that payment power to the next highest interest rate.

Avoid Cash Advances

Your 24% purchase APR is high, but the cash advance APR on the same card is likely much higher, often 29% or more. Furthermore, cash advances do not have a grace period. Interest starts accruing the moment the cash is in your hand. Always compare other options before using a credit card for a cash withdrawal.

Step-by-Step: Lowering Your Interest Costs

Lowering Your Interest Costs

- 1

Check your current rate

Look at your most recent statement or the Schumer Box in your card agreement to find your exact purchase APR.

- 2

Audit your credit score

If your score has gone up 50 points or more since you got the card, you have a strong case for a lower rate.

- 3

Call your issuer

Ask for a rate reduction based on your loyalty and improved credit.

- 4

Compare balance transfer offers

Look for cards with 0% intro periods that are long enough to cover your repayment timeline.

- 5

Stop new charging

If you are carrying a balance at 24%, every new purchase you make starts accruing interest immediately because you have lost your grace period. Switch to cash or a debit card until the balance is zero.

The Role of Credit Unions and Capped Rates

As mentioned, federal credit unions operate under a legal ceiling. This 18% cap is a significant protection for consumers. When national banks are raising rates to 25% or 27%, credit union members are shielded from those extremes.

This difference is due to the structure of the institutions. National banks are beholden to shareholders and aim to maximize profit. Credit unions are non-profit cooperatives. Their goal is to provide affordable credit to their members. If you find that 24% is the best rate you can get at a major bank, it is worth looking at local or national credit unions. Many people qualify for credit union membership through their employer, their location, or by joining a specific association.

Is 24% Ever a Good Rate?

In the context of the current market, 24% is not always "bad." If you are a young adult with a thin credit file or someone rebuilding after a bankruptcy, a 24% APR might be one of the most competitive offers you can find. In these cases, the 24% rate is a tool for building credit rather than a long-term borrowing strategy.

If you use the card responsibly, your credit score will improve over time. Once your score moves from the 600s into the 700s, you can then compare other cards with lower rates or more lucrative rewards. In this scenario, 24% is a stepping stone.

However, for a consumer with a score of 750 who is carrying a $10,000 balance, 24% is objectively high. That individual is likely overpaying for their debt by hundreds of dollars a month and should investigate consolidation or balance transfer options immediately.

Reading the Fine Print: The Schumer Box

Every credit card offer includes a standardized table known as the Schumer Box. This table is required by law and makes it easier to compare cards side by side. When looking at your 24% APR, you should also check these other rates in the box:

- Purchase APR: The rate for standard buys.

- Balance Transfer APR: The rate for moving debt.

- Cash Advance APR: Usually the highest rate on the card.

- Penalty APR: The rate triggered by late payments.

- Annual Fee: This fee is not part of the APR but adds to the overall cost of the card.

- Transaction Fees: Fees for balance transfers or foreign purchases.

By looking at the total cost of the card, you can determine if a slightly lower APR is worth a high annual fee. MoneyAtlas helps you break down these complex terms so you can see the real cost of ownership beyond the headline rate. If avoiding annual fees is a priority, you can also compare no annual fee credit cards.

Next Steps for Cardholders

Understanding that 24% APR is a significant expense is the first step toward better financial health. If you are currently paying this rate, your next move should be to determine how much it is costing you annually. Use a simple interest calculator to see your total yearly interest spend.

Once you have that number, use it as motivation to compare alternatives. Whether you choose to negotiate with your current issuer, move to a credit union, or consolidate with a personal loan, reducing a 24% interest rate can provide immediate relief to your monthly budget. MoneyAtlas provides the tools and reviews necessary to compare these paths effectively. You can start with our credit card reviews if you want to evaluate cards in one place.

Summary of Key Findings

- 24% is average for rewards cards. While it feels high, it is currently a standard rate for many cash back and travel cards.

- Credit scores dictate rates. If your score is excellent, 24% is high. If your score is fair, 24% might be the market rate.

- Daily compounding is the real cost. High APRs make debt grow faster than most people realize.

- Alternatives exist. Balance transfers, credit unions, and personal loans are all viable ways to escape a 24% interest cycle.

FAQ

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

Can Credit Cards Charge Interest on a Zero Balance

Can credit cards charge interest on a zero balance? Learn how residual interest and grace periods work to avoid unexpected fees and clear your debt.

Are Credit Card Interest Charges Tax Deductible for Business?

Are credit card interest charges tax deductible for business? Learn how to deduct interest and fees, manage mixed-use cards, and stay IRS-compliant.

Are Credit Card Interest Charges Tax Deductible? Key Tax Rules

Are credit card interest charges tax deductible? Learn when you can deduct interest for business use and the rules for personal expenses.