How Does APR Affect Credit Cards and Interest Costs

Introduction

Understanding how APR affects credit cards is a critical step for anyone navigating the US financial system. The Annual Percentage Rate, or APR, represents the total yearly cost of borrowing money on a card, expressed as a percentage. It is the primary factor that determines how much interest accumulates if a balance is carried from one month to the next. MoneyAtlas provides tools to compare these rates across more than 1,500 products, helping consumers see how different offers impact their long-term costs. This guide explains the mechanics of interest calculation, the factors that cause rates to fluctuate, and the different types of APR that appear in a standard credit card agreement. By understanding these variables, a cardholder can more effectively compare options and choose the right financial path.

The Basic Mechanics of Credit Card APR

To understand how APR affects credit cards, it is necessary to define what the term actually encompasses. While many people use interest rate and APR interchangeably, they have distinct meanings in the broader lending world. In the context of credit cards, the interest rate and the APR are often the same because most card-related fees are charged separately rather than being folded into the rate.

The APR is a measure of the cost of credit over a year. However, credit card interest is not usually charged once a year. Instead, it is typically calculated daily based on the balance. This means that even a small difference in the percentage rate can lead to significant changes in the total amount paid over several months or years.

If you want a broader shopping starting point, you can also use our best credit cards comparison to see how rates, fees, and rewards stack up side by side.

The Daily Periodic Rate

The most direct way to see how APR affects credit cards is through the daily periodic rate. This is the interest rate the bank applies to a balance every single day. To find this number, the APR is divided by 365. For example, if a card has a 24% APR, the daily periodic rate is roughly 0.065%.

Each day, the card issuer applies this tiny percentage to the current balance. If that balance is $1,000, the daily interest charge would be about 65 cents. Over a 30 day billing cycle, this adds up. Because interest compounds daily, the bank adds the interest from Monday to the balance on Tuesday, and then calculates Tuesday’s interest based on that new, higher total.

The Role of the Grace Period

One of the unique features of credit cards is the grace period. This is the window of time between the end of a billing cycle and the date the payment is due. For most cards, if the statement balance is paid in full by the due date, the APR effectively becomes 0% for those purchases.

In this scenario, the APR does not affect the cost of the card at all. The impact of the APR only begins when a cardholder carries a balance past the due date. Once a balance is carried over, the grace period usually disappears for new purchases as well, meaning interest begins to accrue immediately on everything bought with the card.

Different Types of APR on a Single Card

When looking at a credit card agreement, it is common to see several different APRs listed. Each one applies to a different type of transaction. Knowing these differences is vital when comparing products on MoneyAtlas or reviewing a monthly statement.

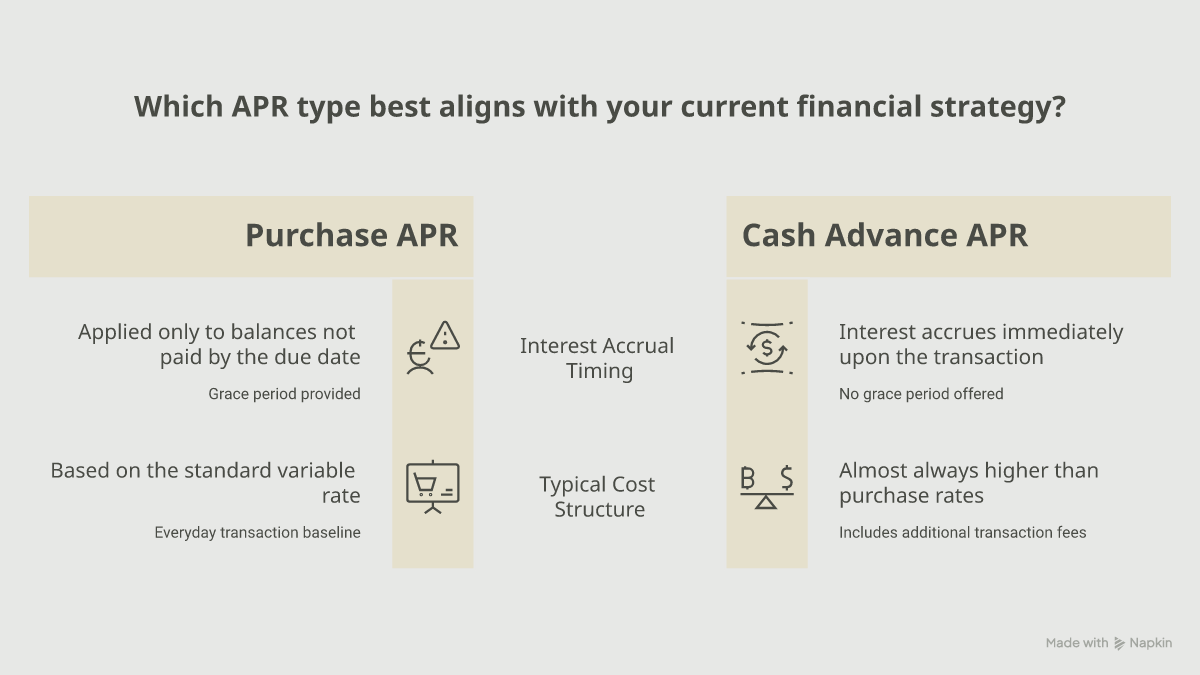

Purchase APR

The purchase APR is the standard rate applied to everyday transactions like buying groceries or paying for gas. This is the rate most people refer to when they talk about a card's interest rate. It applies to any remaining balance from purchases that is not paid off by the monthly due date.

Cash Advance APR

Many cards allow users to withdraw cash at an ATM or through a convenience check. This is known as a cash advance. The APR for cash advances is almost always significantly higher than the purchase APR. Furthermore, cash advances usually do not have a grace period. Interest begins to accrue the moment the cash is in hand. Most cards also charge a flat fee or a percentage of the advance in addition to the high interest rate.

For a deeper look at how cash advances differ from everyday spending, see how credit card APR works to affect monthly balances.

Balance Transfer APR

A balance transfer occurs when debt is moved from one credit card to another. Some cards offer a specific balance transfer APR, which may be lower than the purchase APR to encourage people to move their debt. Many promotional offers feature a 0% APR on balance transfers for a set period, such as 12 to 18 months. It is important to note that most cards charge a balance transfer fee, often 3% or 5% of the total amount moved.

If you are considering that strategy, our balance transfer credit card comparison is the most direct place to compare intro APR windows and transfer fees.

Penalty APR

If a cardholder misses a payment or pays late, the issuer may trigger a penalty APR. This rate is often much higher than the standard purchase rate, sometimes reaching near 30%. The penalty APR can stay in effect for several months, and it may apply to both existing balances and new purchases. Timely payments are the primary way to avoid this significant increase in borrowing costs.

Introductory or Promotional APR

Credit card companies often use introductory APRs to attract new customers. These rates are typically 0% and last for a specific timeframe. For someone planning a large purchase or looking to consolidate debt, these offers are worth comparing. However, once the promotional period ends, the remaining balance is subject to the standard variable APR, which is often much higher.

To understand how those offers work in practice, this APR explainer breaks down the math and the trade-offs.

How Your APR is Determined

Financial institutions do not assign the same APR to every customer. Several factors influence the rate an individual is offered when they apply for a new card. MoneyAtlas tracks these trends to help readers understand which tier of rates they might qualify for based on their financial profile.

Credit Score and Risk

The primary factor in determining a credit card APR is creditworthiness. Lenders view credit scores as a measure of risk. A higher credit score generally leads to a lower APR because the borrower is seen as more likely to repay the debt. Conversely, those with lower scores or limited credit history may only qualify for cards with higher APRs.

When a card lists a range of rates, such as 19% to 29%, the specific rate assigned to a borrower depends on their credit report. Improving a credit score over time is one of the most effective ways to qualify for more favorable rates in the future.

The Prime Rate and Market Conditions

Most modern credit cards have variable APRs. This means the rate can change over time based on the prime rate. The prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers. It is directly influenced by the federal funds rate set by the Federal Reserve.

When the Federal Reserve raises interest rates to combat inflation, the prime rate usually goes up as well. Because most credit cards are tied to the prime rate plus a certain margin, cardholders will see their APR increase shortly after a Fed rate hike. These changes do not require a hard credit check and often happen automatically.

Fixed vs. Variable Rates

While variable rates are the industry standard, some fixed-rate credit cards exist. A fixed rate does not fluctuate with the prime rate. However, the term "fixed" can be misleading. An issuer can still change the rate on a fixed-rate card, but they must generally provide 45 days of notice before doing so. Fixed-rate cards have become increasingly rare in the US market.

The Long-Term Impact of a High APR

The true impact of APR is felt most clearly when looking at how long it takes to pay off a debt. A high APR acts like a headwind, making it harder to reduce the principal balance because a large portion of every payment is consumed by interest charges.

The Minimum Payment Trap

Credit card companies only require a small minimum payment each month, often 1% to 3% of the total balance plus interest. When the APR is high, the interest charge can make up the majority of that minimum payment. This results in the principal balance barely moving, even though a payment was made.

For someone carrying a $5,000 balance at a 24% APR, the monthly interest charge alone is roughly $100. If the minimum payment is $125, only $25 is actually going toward the debt. At this rate, it could take decades to pay off the balance, and the total interest paid could be thousands of dollars more than the original amount borrowed.

Compound Interest in Reverse

Compounding is often called the eighth wonder of the world when it applies to savings, but it works against the consumer when it applies to debt. Because interest is added to the balance daily, the cardholder ends up paying interest on their interest. This accelerating effect is why credit card debt can feel so difficult to escape. Lowering the APR, even by a few percentage points, can significantly slow down this compounding process.

If you are carrying a balance, this guide to avoiding APR on a credit card is a useful next step.

Strategies to Manage and Lower APR Costs

While APR is determined by the lender and market conditions, there are ways to mitigate its impact. Managing interest costs requires a proactive approach to credit usage and a willingness to compare different financial products.

Paying More Than the Minimum

The most effective way to reduce the impact of a high APR is to pay as much as possible above the minimum requirement. Every extra dollar paid goes directly toward the principal balance. As the principal drops, the amount of interest charged each month also decreases, creating a positive cycle that leads to faster debt repayment.

Utilizing Balance Transfer Cards

For those currently carrying high-interest debt, moving that balance to a card with a 0% introductory APR is a strategy worth exploring. This pause in interest allows 100% of every payment to go toward the principal. MoneyAtlas helps users compare balance transfer offers to see which cards have the longest promotional periods and the lowest transfer fees.

It is important to have a plan to pay off the debt before the 0% period expires. Once the promotion ends, any remaining balance will be subject to the card's standard APR, which could be just as high as the original card.

Negotiating with the Issuer

In some cases, it is possible to negotiate a lower APR with a current credit card issuer. This is most successful for cardholders who have a long history of on-time payments and an improved credit score since they first opened the account. A simple phone call to the customer service department to request a rate reduction can sometimes lead to a lower APR, especially if the cardholder mentions they are considering moving their balance to a competitor.

Improving Your Credit Profile

Since the APR is a reflection of risk, improving a credit profile is a long-term solution for obtaining better rates.

- Payment History: Making every payment on time is the most significant factor in a credit score.

- Credit Utilization: Keeping balances low relative to credit limits shows lenders that a borrower is not overextended.

- Credit Mix: Having a variety of credit types, such as a car loan and a credit card, can help the score.

- Limiting Inquiries: Avoiding too many new credit applications in a short period prevents small, temporary dips in the score.

Comparing Cards Using the Schumer Box

To help consumers understand how APR affects credit cards before they apply, the federal government requires a standardized disclosure known as the Schumer Box. This table is included in every credit card agreement and marketing offer. It provides a clear, side-by-side look at the various rates and fees associated with the card.

When looking at a Schumer Box, focus on the following sections:

- Annual Percentage Rate for Purchases: The ongoing rate for standard buying.

- Other APRs: The rates for balance transfers, cash advances, and penalties.

- How to Avoid Paying Interest: Details on the grace period.

- Minimum Interest Charge: The smallest amount of interest the bank will charge if you owe anything.

Using these standardized figures makes it easier to use the comparison tools at MoneyAtlas. Instead of digging through pages of fine print, the Schumer Box puts the most important cost factors in one place.

How Market Trends Affect Your Wallet

The average credit card APR in the US has historically hovered around 15% to 16%, but in recent years, those averages have climbed above 20%. This shift is largely due to changes in the broader economy and the Federal Reserve's interest rate policies.

When market rates are high, even those with excellent credit may see APRs that seem surprisingly elevated. During these cycles, the importance of paying the full balance each month becomes even greater. When rates are low, borrowing becomes cheaper, but the mechanics of daily compounding and the loss of the grace period remain the same.

MoneyAtlas monitors these market shifts to provide context on whether a 21% APR is competitive for a certain credit tier or if there are better options available. Knowing the current "market rate" for a specific credit score helps a consumer know when they are getting a fair deal.

Checklist for Evaluating a Card's APR

When comparing new credit cards or reviewing your current accounts, use this checklist to gauge the impact of the APR on your finances.

- Check the Purchase APR: Is the rate fixed or variable? If it is a range, what is the highest potential rate you might receive?

- Identify the Grace Period: Does the card offer a grace period of at least 21 days? Does it apply to both purchases and transfers?

- Verify Promotional Terms: If there is a 0% introductory rate, how long does it last? What is the "go-to" rate after the promotion ends?

- Look for Fees: Does the card have an annual fee? Are there balance transfer or cash advance fees that change the total cost of the APR?

- Understand the Penalty APR: What triggers it and how long does it stay in place? Knowing this helps avoid the most expensive tier of credit.

Choosing the Right Card for Your Habits

The way APR affects credit cards depends entirely on how the card is used.

For a "transactor", someone who pays their bill in full every month, the APR is virtually irrelevant. This person might prioritize a card with high rewards or travel perks, even if the APR is 29%. Since they never carry a balance, they never pay the interest.

For a "revolver", someone who occasionally or regularly carries a balance, the APR is the most important feature of the card. A person in this situation would likely benefit from a card with the lowest possible ongoing APR, even if it offers no cash back or rewards. The savings on interest will almost always outweigh the value of any rewards earned.

If you are comparing low-fee options, our no annual fee credit cards page can help you narrow the field quickly. For rewards-focused spenders, our cash back credit cards comparison is another useful next step.

MoneyAtlas makes it easier to filter cards based on these specific needs. By identifying whether rewards or a low rate is the priority, a consumer can narrow down the 1,500+ products we track to the few that best fit their spending and repayment habits.

Summary of the APR Impact

The Annual Percentage Rate is more than just a number on a statement. It is a dynamic force that determines the velocity of debt growth. It fluctuates with the economy, reflects an individual's financial reputation, and dictates how much of a person's hard-earned money goes to a bank rather than toward their own goals.

By paying attention to the daily periodic rate, understanding the various types of APR, and using comparison tools to find the most competitive offers, a cardholder can take control of their interest costs. While we cannot control the Federal Reserve or the prime rate, we can control which cards we choose to carry and how we manage our monthly payments.

If you want to keep comparing options, our travel credit cards comparison is useful for rewards-first readers, and the Chase Freedom Unlimited review is a strong example of a card that blends everyday earning with a lower-fee structure.

MoneyAtlas Staff

Articles and reviews from the MoneyAtlas editorial team — independent research on credit cards, banking, loans, insurance, and investing.

Related Articles

Can My Credit Card Interest Rate Increase? What to Know and Do

Can my credit card interest rate increase? Learn why APRs rise, your legal protections under the CARD Act, and how to lower your rate or switch cards.

Can I Request a Lower Interest Rate on a Credit Card?

Can I request a lower interest rate on credit card? Yes. Use our guide to negotiate your APR, save on interest, and explore alternatives if denied.

Did Credit Card Interest Rates Drop to 10%? The Reality of Current Proposals

Did credit card interest rates drop to 10? Learn the truth about the proposed 10% rate cap, the Sanders-Hawley bill, and how to manage your debt today.