Pay Off Your Credit Card Faster: How a Credit Card Payoff Calculator Can Help

Struggling with credit card debt? See how a credit card payoff calculator can help you create a repayment plan and save on interest.

Credit card debt can strain your finances and be a huge source of stress. Because credit cards often have high interest rates, paying off your debt is often a struggle. Your balance can quickly grow with interest charges if you’re not careful.

A credit card payoff calculator is a useful tool to help you figure out how long it will take to eliminate your credit card debt based on your monthly payment.

Types of Credit Card Payoff Calculators

The type of financial calculator you should use depends on what you’re trying to figure out. Consider these options if you’re looking for a credit card payoff calculator.

General Payoff Calculators

General payoff calculators will help you determine how long it will take to pay off one of your credit card balances. These calculators are ideal if you only have one credit card balance or want to pay off one of your cards before closing it out. It’s easier to determine how long to pay off your credit card with a calculator.

Debt Repayment Calculators

Debt repayment calculators are useful when you want to know how long it will take to repay all of your debt, including your combined credit card balances. The average U.S. household with credit card debt owes about $6,065 in total. That debt is often spread across multiple credit cards.

If you’re interested in how to pay off credit card debt, this calculator can help you determine how much you would need to pay each month to eliminate your debt by a set date. Or you can calculate how long it would take to repay all your debt just by making your current monthly payments.

For example, if you have bad business credit cards, the debt repayment calculators can help you figure out a repayment plan and how long it would take to eliminate that debt. Even credit card points for niche professionals won’t outweigh high interest rates, so focus on repayment.

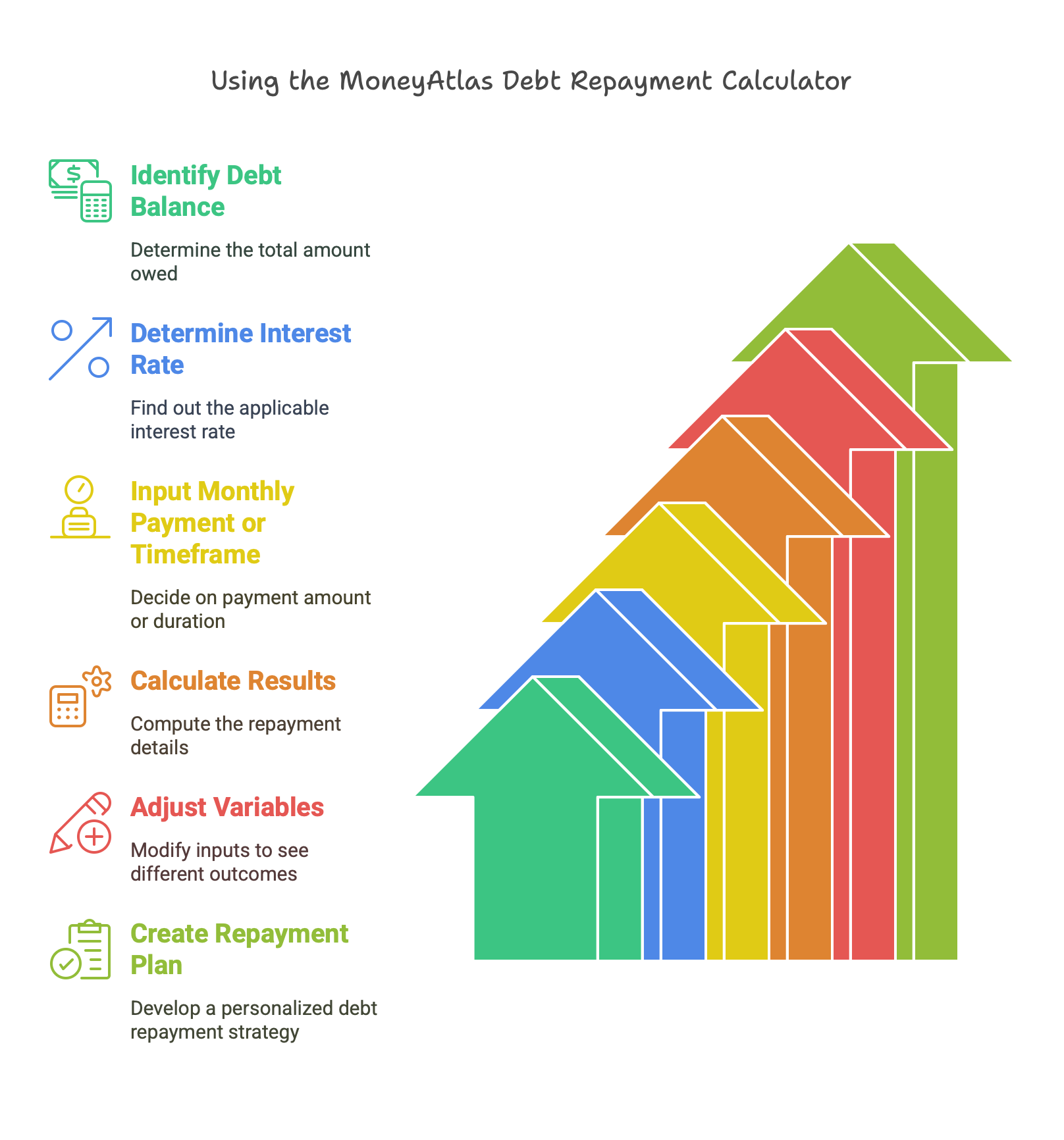

How To Use the MoneyAtlas Debt Repayment Calculator

You only need to know a few key variables to use a debt repayment calculator:

- The balance you owe (in dollars)

- The interest rate

- Your expected monthly payment OR how quickly you want to pay off your debt (in months)

Once you put these details into the calculator, it will tell you either the estimated monthly payment necessary to eliminate your debt in the specified time or how long it would take to pay off your debt. You can tweak the variables to see how they change the final results and create your personalized repayment plan.

Repayment Strategies

When you’re repaying your credit card debt, don’t just randomly make extra payments on your balances. That’s not the most efficient use of your money or time. Instead, try one of these repayment strategies: the snowball or the avalanche method.

Snowball Method Explained

In the snowball method, you list all of your debts from the smallest to the largest balance. For example, your list might be a $2,000 balance on Credit Card A, a $4,000 balance on Credit Card B, and a $12,000 balance on Credit Card C.

Then you put as much money as possible toward paying off the first credit card on the list while making the minimum monthly payments on the other credit card balances. Once you eliminate the first balance, you move on to the next-smallest balance, and so on, until all your debt is gone.

The snowball method works with any type of credit card or debit account. With business credit cards, for instance, you can make the business credit card minimum payment on all your balances except the largest.

Avalanche Method Explained

Instead of credit card balances, the avalanche method focuses on your interest rates. Start by listing all your debt accounts from largest to smallest interest rate. For example, you might have a 26% interest rate on Card A, an 18% interest rate on Card B, and a 15% interest rate on Card C.

Focus on paying off Card A, the card with the highest interest rate, while making minimum payments on the other cards. When you pay off Card A, move on to the next one on the list until all your cards are paid off.

For either method, you can decide which credit card to pay off first with a calculator to help find the optimal order to tackle your credit card balances.

Utilizing Balance Transfer Cards

If the interest rates on your credit card debt are very high, you may benefit from a balance transfer card. With a balance transfer, you move all your existing debt to a new card that typically has better terms, such as a lower interest rate. Some cards may even offer 0% interest for an introductory period.

You can take advantage of the balance transfer to pay less interest on your debt and consolidate your payments. Instead of having to pay all your different credit card companies, you’d just have to make one monthly payment on the balance transfer card.

There are some cons, though. You will probably have to pay a balance transfer fee to move your credit card balances to the new card. Additionally, when the introductory interest rate expires, you may face a high interest rate — possibly even higher than your original rates.

The best way to take advantage of a balance transfer card is to try to pay off as much of your debt as possible during the introductory period. That way, you save money by minimizing your interest payments and hopefully make your debt much more manageable.

Learn How To Manage Multiple Credit Cards With MoneyAtlas

Managing multiple cards and eliminating your credit card debt isn’t easy. But with the right knowledge and strategies, you can do it.

With MoneyAtlas’s thorough card comparisons and financial guides, you can learn what you need to get a handle on your credit card debt. Explore personal finance articles to get more out of your cards.